If you are a Spotify leader or early employee who has seen the company become synonymous with music streaming and get listed, the majority of your net worth is likely in Spotify stocks.

While these RSUs have created wealth, it now creates a risk: your income, your savings, and your financial future are all tied to the performance of a single stock.

This blog talks about how you can protect your Spotify RSU wealth and grow it, and what other Spotify senior folks with significant RSU holdings are doing.

Table of contents

- Risks with Spotify RSUs

- Protect your Spotify RSU wealth

- How to diversify vested Spotify stocks?

- What are the tax implications?

- How to minimize tax burden?

- How Paasa can help

- FAQs

Risks of having a large part of your net worth tied to Spotify stocks

For many Spotify employees, their compensation structure creates a situation where a large part of their wealth ends up being locked in employer stocks.

Here are the risks of having a large part of your wealth in Spotify stocks:

1. Growth Risk

Markets are unpredictable in the short term and growth at the level of individual stocks remains uncertain over any given period.

Even a fundamentally strong stock like Spotify can grow slower than the broader market and even go through extended periods of slow growth.

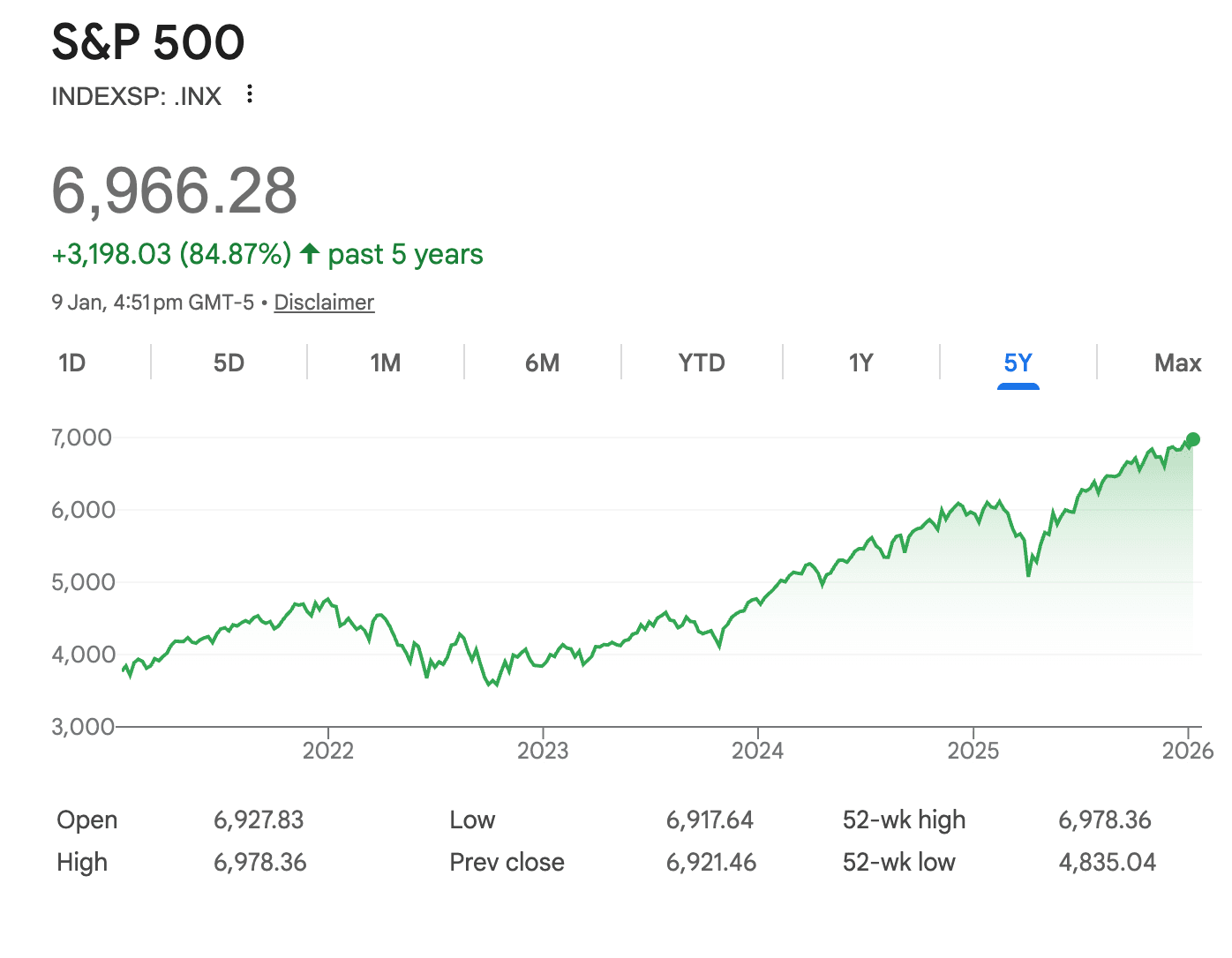

Despite being the market leader, the stock price of Spotify has not caught up to broader market growth for the last few years.

While Spotify grew 67.17% over the past 5 years (as of Jan 2026), the S&P 500 provided returns of 84.87% over the same time period.

Spotify is now a market leader. While this offers stability, mature giants rarely offer the explosive hyper-growth of the broader, diversified mid-cap market.

2. Concentration Risk

Having a large part of your wealth tied up in one stock means that the overall returns of your portfolio will be strongly correlated to that particular company’s performance.

This increases volatility as any growth slowdowns or sectoral changes affecting the company’s stock will also affect your net worth and other financial plans.

For tech professionals with $100k+ in salary compensation, concentration in employer stocks also creates a situation where your income and wealth is tied to the performance of the same company.

3. Wealth erosion due to the 40% US Estate Tax

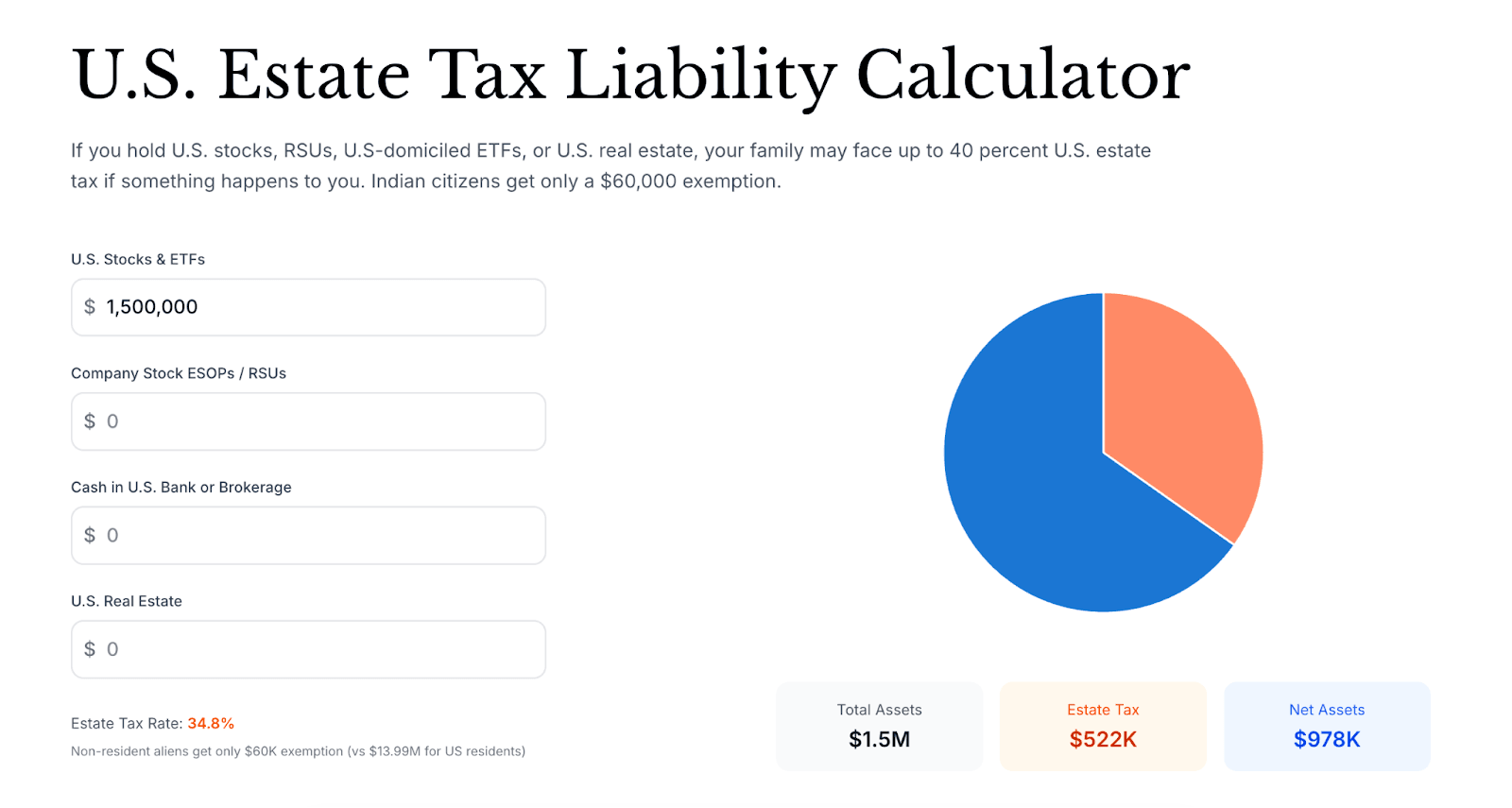

In the event of your death, all your US assets (like stocks, ETFs, any property in the US, etc) over the $60,000 exemption limit are subject to the US Estate Tax of up to 40%

Since Spotify stocks are US-situs assets, they are subject to the US estate tax.

The US estate tax is an up to 40% tax that needs to be paid on the total value of your US assets upon your death.

US domiciled persons have a $15 million exemption limit, and only assets above this exemption limit are subject to this tax.

However, if you are not US domiciled, the exemption limit for you is only $60,000, and any US-situs asset above this threshold is subject to the US estate tax.

Example

If you have Spotify stocks worth $1.5 million, your family will have to pay a 34.8% tax ($522,000) on this asset upon your death, wiping off more than a third of your RSU wealth instantly. The liability increases if you also have other US assets.

Use our Estate Tax Calculator to find out your exact tax liability.

To learn more about how you can protect your RSUs from the US estate tax, visit our guide on How Indian professionals can protect RSUs from estate tax.

How to protect your Spotify RSU wealth?

Many Spotify employees are mitigating this by selling a portion of their RSUs and diversifying into other stocks and US estate-tax friendly instruments (like UCITS ETFs).

Here’s how diversification protects against the risks we discussed:

1. Spread out the growth risk

Diversification ensures that your portfolio tracks the performance of the broader market rather than relying on a single stock.

Depending on your risk appetite, you can choose funds like S&P 500, target specific sectors like AI or commodities, or go for a combination.

This ensures your wealth follows market-wide growth and isn't limited by the performance of just one company.

2. Eliminate concentration risk

Concentration risk exposes you to volatility, meaning that any abrupt movement in Spotify stock will also have a large effect on your overall portfolio. Diversification reduces this volatility by spreading out the risk over several companies and sectors.

For example, if a large part of your net worth is tied to the Spotify stock, your portfolio will show large swings when the Spotify stock goes up or down significantly.

A diversified portfolio will be less prone to such swings as your risk is spread across several assets, and when some of them are going down, others are going up.

“A portfolio can also hold several stocks and ETFs and still be exposed to the same market risks.

Proper diversification involves investing in assets that behave differently across market environments. “

3. Use UCITS ETFs to avoid the US Estate Tax

Many Indian tech professionals are now using UCITS ETFs to avoid the US Estate Tax while staying invested in the US market.

UCITS ETFs are funds that invest in US markets but are domiciled in Europe, most commonly in Ireland or Luxembourg.

As they are legally situated in the European Union, they are not subject to the US Estate Tax even when they hold US stocks such as Apple, Microsoft, or Google.

Rather than holding the S&P 500, you can hold an equivalent UCITS ETFs and avoid the risk of 40% US Estate Tax.

UCITS ETFs are functionally similar to US ETFs, and only the legal domicile is different.

Use our UCITS Screener to find UCITS compliant investment instruments.

Tax implications of diversifying your Spotify RSUs

When you sell your vested RSUs, you have to pay capital gains tax on the profit you are making.

The rate of capital gains tax is decided by your holding period:

To learn more about the tax liabilities arising from the sale of foreign stocks and ETFs, visit our guide on Capital Gains Tax on Foreign Stocks and ETFs

How to minimize your lifetime tax burden while diversifying your Spotify RSUs

The capital gains tax is unavoidable since you have to sell your vested RSUs to diversify.

But your total tax liability can be optimized by implementing a structured selling plan.

We suggest you sell your RSUs in the following order for minimizing your tax liability:

- Vested RSUs with the highest cost basis. These are units currently trading at a loss or closest to their original vesting price (where you have little to no taxable gain).

- Vested RSUs that fall under LTCG (long term capital gains), starting with the units where you have made the minimum capital gains.

- Vested RSUs that fall under STCG (short term capital gains), starting with the units where you have made the minimum capital gains.

How to diversify your vested Spotify RSUs with Paasa

At Paasa, we make the process of moving from concentrated RSUs to globally diversified portfolios seamless. Here’s how it works:

Step 1: Transfer RSUs via ACATS

Your RSUs are transferred from your broker (like Morgan Stanley, E*TRADE, Charles Schwab, Fidelity) into your Paasa account through the Automated Customer Account Transfer Service (ACATS). This is the standard industry process used by global brokerages.

Step 2: Strategic liquidation

Once your RSUs are in Paasa, you can liquidate them, either partially or fully, depending on your goals.

Step 3: Reinvestment into UCITS ETFs or direct stocks

You can then reinvest into direct global stocks, UCITS ETFs, commodities, or Paasa’s curated managed strategies. This gives you global diversification, estate tax protection, and better tax efficiency.

All your assets in Paasa are held directly with Interactive Brokers, offering unmatched security and peace of mind.

If you want to discuss this with our team and understand it in detail, you can schedule a call with us or write to us at support@paasa.com.

Why many Spotify employees are moving to Paasa

Spotify employees are moving to Paasa for unmatched access to global markets (like Switzerland, China, Japan, Singapore, and more), and for the safety and stability offered by Interactive Brokers.

Whether you want to buy BYD stocks or invest in UCITS ETFs to avoid the US Estate Tax, Paasa has it all.

Paasa works with Indian HNIs, family offices, and institutional investors, bringing the same global access and compliance depth to professionals managing RSU wealth. It offers one of the widest UCITS ETF portfolios available to Indian investors, enabling diversification across equities, bonds, and thematic exposures in multiple markets.

Disclaimer

This material is provided for general information only and does not constitute investment, tax, or legal advice. Paasa does not guarantee any returns or outcomes from the strategies described. All investments and remittances should be made in accordance with applicable RBI, FEMA, and income-tax regulations. Investors are advised to seek independent professional advice before acting on any information contained herein.