Indian professionals who are moving back from Canada often lack clarity about how they can manage their overseas holdings like stocks, ETFs, RRSPs, and TFSAs after moving back.

This article explains how you can manage your overseas holdings after moving back to India and navigate complex rules like the CRA's departure tax and deemed disposition.

We also cover your new Indian tax and reporting requirements, your changing tax residency status, how you can avoid double taxation, and RNOR rules and opportunities.

Table of contents

- What happens to my stocks when I move back to India?

- What happens to my RRSP, TFSA, and CPP when I move back to India?

- What happens to my RSUs and stock options when I move back?

- What happens to my Canadian property when I move back?

- Tax and reporting implications of moving back to India

- What is RNOR status and how does it affect me?

- Common Questions Canadian NRIs Have About Moving Back

- About Paasa

What happens to my stocks when I move back to India?

When you move back to India, the first major hurdle you face is Canada's departure tax.

Canada's departure tax triggers a deemed disposition on most non-registered capital property at fair market value (FMV) the day before you cease your Canadian tax residency. The Canada Revenue Agency (CRA) treats your assets as if you sold them, taxing 50% (66.67% as of January 1, 2026 for gains over $250,000) of the capital gains at your marginal rate (up to roughly 53% combined federal and provincial).

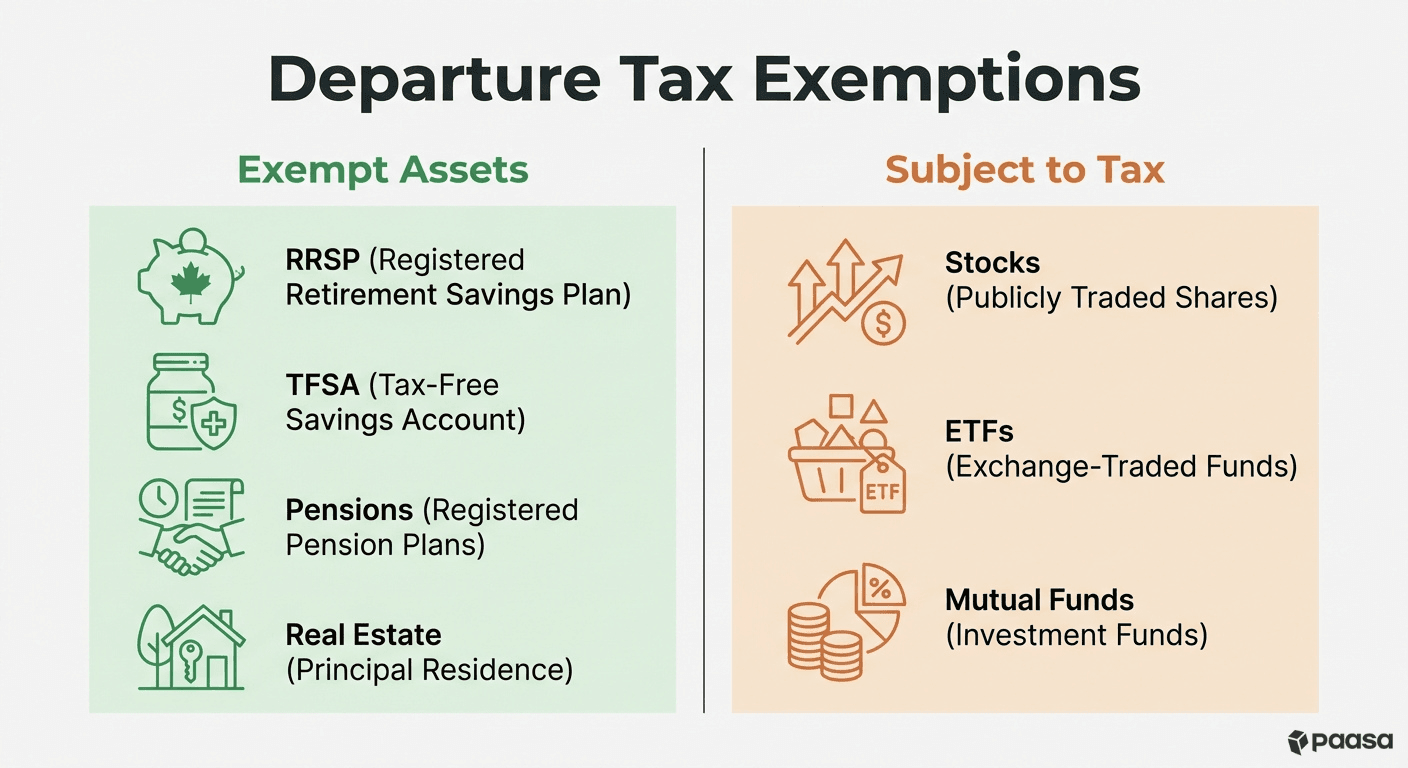

This applies to public stocks, mutual funds, ETFs (both domestic and foreign), and private company shares held in standard, non-registered investment accounts.

Which assets are exempt from the departure tax?

Your registered plans, including your RRSP, RRIF, TFSA, employer pensions, and Canadian real estate, are exempt from the deemed disposition exit tax.

What if I bought the stocks before moving to Canada?

Stocks or ETFs bought before your Canadian residency are subject to deemed disposition, but you are only taxed on the gains accrued during your residency. Your pre-arrival Adjusted Cost Base (ACB) carries over. The CRA only taxes the difference between the FMV on the day you leave and the FMV on the day you arrived.

Can I defer this tax?

If you have a liquidity crunch or plan to return to Canada, you can elect to defer the payment of this departure tax by filing a Section 220(4.5) election using Form T1244. You must post "adequate security" (like a bank letter of credit) with the CRA. Furthermore, short-term residents who lived in Canada for less than 60 months in the past 10 years are exempt from deemed disposition on property they owned before moving to Canada.

What happens to the assets I choose to keep?

Under Indian FEMA regulations, you are legally allowed to indefinitely hold any foreign stocks or ETFs you acquired while living in Canada.

However, while Indian law allows you to keep them, Canadian platforms might not:

- Retail Fintechs (Wealthsimple): These platforms generally cater strictly to Canadian residents. If you update your tax residency to India, they may restrict your account to "liquidate-only" mode.

- Traditional Bank Brokers (Questrade, TD Direct Investing, RBC Direct): These are sometimes more flexible and may allow you to maintain a non-resident account. However, you will likely face high platform fees, trading restrictions, and you will have to manage your complex Indian tax reporting manually.

What's the best way to stay invested globally after moving back to India?

The best way to stay invested globally is to transfer your investments into a platform specifically built for global investing from India.

You do not need to sell your non-registered stocks just because your Canadian broker is restricting your account. Instead, use an in-kind transfer (like AON/ACATS). This allows you to move your entire eligible portfolio "as is" to an India-friendly platform like Paasa.

These platforms allow you to maintain your positions and trade normally, while providing India-specific compliance support and tax documents tailored for your mandatory Schedule FA reporting.

What happens to my RRSP, TFSA, and CPP when I move back to India?

You can keep all major Canadian retirement accounts after returning to India. They remain open with your provider and continue to grow. However, the tax treatment changes significantly.

1. RRSP (Registered Retirement Savings Plan) and RRIF

You can keep your RRSP indefinitely. There is no forced closure, though your contribution room freezes since you no longer have Canadian earned income. You can also convert it to a RRIF at age 71 as usual.

- Canadian Tax: Canada imposes a 25% non-resident withholding tax on lump-sum withdrawals. However, for periodic pension payments, this can be reduced to 15% under the India-Canada Double Taxation Avoidance Agreement (DTAA) by filing form NR301.

- Indian Tax: Once you are a full Indian tax resident (post-RNOR), withdrawals are taxed at your applicable slab rates. You can claim a full DTAA credit in India for the 15% or 25% tax already withheld by Canada to avoid double taxation.

2. TFSA (Tax-Free Savings Account)

You can fully retain your TFSA. You cannot make new contributions as a non-resident, but the investments inside continue to grow tax-free worldwide from the CRA's perspective.

- Canadian Tax: There is zero Canadian tax on TFSA withdrawals. It remains a non-taxable event in Canada.

- Indian Tax: India does not recognise the TFSA as a tax-exempt vehicle. Once you become a full Resident (ROR), income and gains accruing inside your TFSA, including interest, dividends, and capital gains, are taxable in India in the year they arise, regardless of whether you have withdrawn them. The TFSA balance must also be declared in Schedule FA each year. During your RNOR window, this income is sheltered and not taxable in India, provided it remains in your Canadian account.

Note: The RNOR window is the most efficient time to draw down a large TFSA if needed. Neither Canada nor India taxes the withdrawal during that period.

3. CPP (Canada Pension Plan)

The CPP is a portable lifetime benefit based on your mandatory contributions during employment. You can start drawing it at age 60 or 65, even from India.

- Canadian Tax: Canada applies a 25% withholding tax on CPP payouts sent abroad. (You may apply for an NR5 waiver if your overall global income is very low).

- Indian Tax: Once you are a full resident, this is taxed at your standard slab rates as pension income, and you can claim a foreign tax credit for the Canadian withholding.

When is the best time to make RRSP withdrawals?

The RNOR window changes the tax cost of RRSP withdrawals significantly. Here is a direct comparison between withdrawing during RNOR and withdrawing after becoming a full Resident (ROR).

Example

You withdraw CAD 50,000 from your RRSP. You have filed Form NR301 to claim the reduced DTAA withholding rate. You are in the 30% Indian tax slab with income above ₹2 crore.

Scenario A: You withdraw during RNOR

| Component | Amount | Note |

|---|---|---|

| RRSP withdrawal (A) | CAD 50,000 | Gross amount |

| Canadian withholding at 15% DTAA rate (B) | CAD 7,500 | Reduced rate via NR301 |

| Net received in Canadian account (A minus B) | CAD 42,500 | |

| Indian tax liability | Nil | Foreign income exempt during RNOR |

| Total tax paid | CAD 7,500 | Effective rate: 15% |

Scenario B: You withdraw after becoming ROR

| Component | Amount | Note |

|---|---|---|

| RRSP withdrawal (A) | CAD 50,000 | Gross amount |

| Canadian withholding at 25% (B) | CAD 12,500 | Standard non-resident rate without DTAA election |

| Indian base tax at 30% (C) | CAD 15,000 | On full withdrawal amount |

| Surcharge at 25% of (C) (D) | CAD 3,750 | Applicable for income above ₹2 crore |

| Cess at 4% of (C+D) (E) | CAD 750 | |

| Gross Indian tax (C+D+E) (F) | CAD 19,500 | |

| Foreign tax credit for (B) (G) | CAD 12,500 | Credit for Canadian withholding |

| Net Indian tax payable (F minus G) | CAD 7,000 | |

| Total tax paid (B plus net Indian tax) | CAD 19,500 | Effective rate: 39% |

Withdrawing during RNOR saves CAD 12,000 in this example and cuts the effective rate from 39% to 15%.

Note: You must file Form NR301 with your Canadian financial institution before the first withdrawal to claim the reduced 15% DTAA rate. Without it, Canada defaults to 25% withholding on all amounts.

What happens to my RSUs and stock options when I move back?

If you held RSUs or stock options as part of your Canadian compensation, the situation at departure depends on which of three scenarios applies to you.

Scenario 1: You are leaving your Canadian employer

In most cases, returning to India means leaving the Canadian company you worked for. Unvested RSUs are forfeited at termination. There is no departure tax on them because you no longer hold the right to receive the shares.

What does fall within the departure tax net is any vested RSU shares you are still holding in your brokerage account at the time of departure. These are treated like any other non-registered stock. The CRA deems them sold at fair market value on your departure date, and you pay capital gains tax on 50% of the gain at your marginal rate.

When an RSU vests, the fair market value on the vesting date is taxed as ordinary employment income. That same value then becomes your Adjusted Cost Base (ACB), which is the Canadian term for cost of acquisition, used to calculate any future capital gain. You are not taxed on the same amount twice.

Example

You received RSU grants over a few years. By the time you leave Canada, 1,000 shares have vested and are trading at CAD 45. You are still holding them. The shares were worth CAD 20 each when they vested, and you paid employment tax on that amount at vesting.

| Component | Amount | Note |

|---|---|---|

| FMV at departure (A) | CAD 45,000 | 1,000 shares at CAD 45 |

| ACB at vesting (B) | CAD 20,000 | 1,000 shares at CAD 20, already taxed as employment income |

| Capital gain (A minus B) | CAD 25,000 | |

| Taxable gain, 50% inclusion (C) | CAD 12,500 | Canada taxes 50% of capital gains |

| Estimated federal tax at 33% (D) | ~CAD 4,125 | Approximate top federal rate |

| Provincial tax (varies by province) | ~CAD 2,500 | Depends on province of residence |

| Estimated total Canadian tax | ~CAD 6,625 |

Note: To understand how India taxes any future gains when you eventually sell these shares after returning, read our guide on how foreign capital gains are taxed for Indian investors.

Scenario 2: Intra-company transfer to an Indian entity

If you continue working for the same company through its Indian entity and your RSUs keep vesting after departure, the employment income at each vesting event is apportioned between Canada and India. The CRA calculates the Canadian-source portion based on the ratio of Canadian workdays during the full vesting period to total workdays during that period.

Canada withholds 25% non-resident withholding tax on the Canadian-source portion. During your RNOR window in India, this foreign-source income is not taxable in India. Once you become a full Resident (ROR), both portions are taxable in India, with a foreign tax credit available for the Canadian withholding already paid.

Note: Keep a workday log from the grant date of every RSU through to the vesting date. The apportionment calculation covers the entire vesting period and requires documentation of where you physically worked on each day.

What happens to my Canadian property when I move back?

Canadian real estate is exempt from deemed disposition at departure, so you do not pay a departure tax even if the property has appreciated significantly. You can continue to hold it. However, two obligations apply once you become a non-resident, and both are frequently overlooked.

Rental income as a non-resident

If you rent out your Canadian property after leaving, Canada applies Part XIII withholding tax of 25% on the gross rental income. Your property manager is required to withhold this and remit it to the CRA monthly.

To pay tax on net income instead, you can file an NR6 election with the CRA before the first rental payment of the year. This lets you deduct expenses like mortgage interest, maintenance, and property management fees before calculating tax owing.

How does India treat this rental income?

This depends on your Indian residency status:

- During RNOR: Rental income from your Canadian property is tax-free in India, provided your tenant deposits the rent into your Canadian bank account first. If it is wired directly to your Indian account, it becomes taxable in India immediately. To learn more, read our guide on foreign rental income for RNORs.

- After becoming ROR: The income becomes taxable in India at your slab rate. Under Article 6 of the India-Canada DTAA, Canada retains primary taxing rights on rental income from Canadian property. India also taxes it but gives you a foreign tax credit for the Canadian tax already withheld, so you do not pay tax on the full amount twice.

Example

You rent your Toronto property for CAD 4,000 per month (CAD 48,000 per year). Your annual expenses are CAD 18,000. You have filed an NR6 election. You are in the 30% Indian tax slab with income above ₹2 crore.

| Component | RNOR year | ROR year |

|---|---|---|

| Gross rental income | CAD 48,000 | CAD 48,000 |

| Canadian expenses deducted via NR6 | CAD 18,000 | CAD 18,000 |

| Canadian net income | CAD 30,000 | CAD 30,000 |

| Canadian tax at 25% on net (A) | CAD 7,500 | CAD 7,500 |

| Indian base tax at 30% on gross (B) | Nil | CAD 14,400 |

| Surcharge at 25% of (B) (C) | Nil | CAD 3,600 |

| Cess at 4% of (B+C) (D) | Nil | CAD 720 |

| Gross Indian tax (B+C+D) | Nil | CAD 18,720 |

| Foreign tax credit for (A) | N/A | CAD 7,500 |

| Net Indian tax payable | Nil | CAD 11,220 |

| Total tax paid | CAD 7,500 | CAD 18,720 |

Filing the NR6 election is worth doing as a ROR as well. Without it, Canada withholds 25% on the full gross rent (CAD 12,000 in this example). Your foreign tax credit rises accordingly, but so does the total outflow before the credit is claimed in India.

Selling Canadian property as a non-resident

When you sell Canadian property as a non-resident, two tax systems are involved: Canada and India. How much you pay to each depends on when you sell relative to your Indian residency status.

Canada always taxes the gain. Under Article 13 of the India-Canada DTAA, Canada retains the right to tax gains from immovable property situated in Canada regardless of where you live. This does not change when you become an Indian resident.

India's right to tax depends on when you sell.

- During RNOR: India does not tax the gain. Only Canada taxes the sale.

- After becoming ROR: India also taxes the gain. For property held for more than 24 months, this is treated as long-term capital gains and taxed at 12.5% without indexation under the post-2024 budget rules. In this case, India gives you a foreign tax credit for the Canadian tax already paid, so you only have to pay the difference if the tax paid in Canada is lower than the tax you owe in India. If the tax paid in Canada is higher, you do not need to pay anything in India, but neither do you get a refund for the extra tax paid in Canada.

Note: For most of our readers selling Canadian property, the Canadian tax paid will exceed the Indian LTCG liability of 12.5%, meaning no additional Indian tax is owed.

Do note that under India's "Ordinary Credit Method" (Rule 128), the Foreign Tax Credit (FTC) is adjusted only against the tax liability on that specific foreign income, not your total tax bill.

The credit you can claim is restricted to the lower of:

- Actual tax paid abroad

- Indian tax payable on that specific income

That said, confirm your specific position with a CA before the sale, as the exact outcome depends on provincial rates and the size of the gain.

Tax and reporting implications of moving back to India

When you permanently return to India, your tax status eventually shifts from being a Non-Resident Indian (NRI) to a Resident.

This brings two major changes: your global income becomes taxable in India, and your reporting requirements increase significantly.

To learn more about how your global income is taxed in India and the reporting requirements, read:

- How Global Stocks and ETFs Are Taxed for Indian Investors

- Tax on Repatriation of Foreign Income to India

- Foreign Asset Disclosure (Schedule FA) Requirements for Indians

When do you become an Indian Tax Resident?

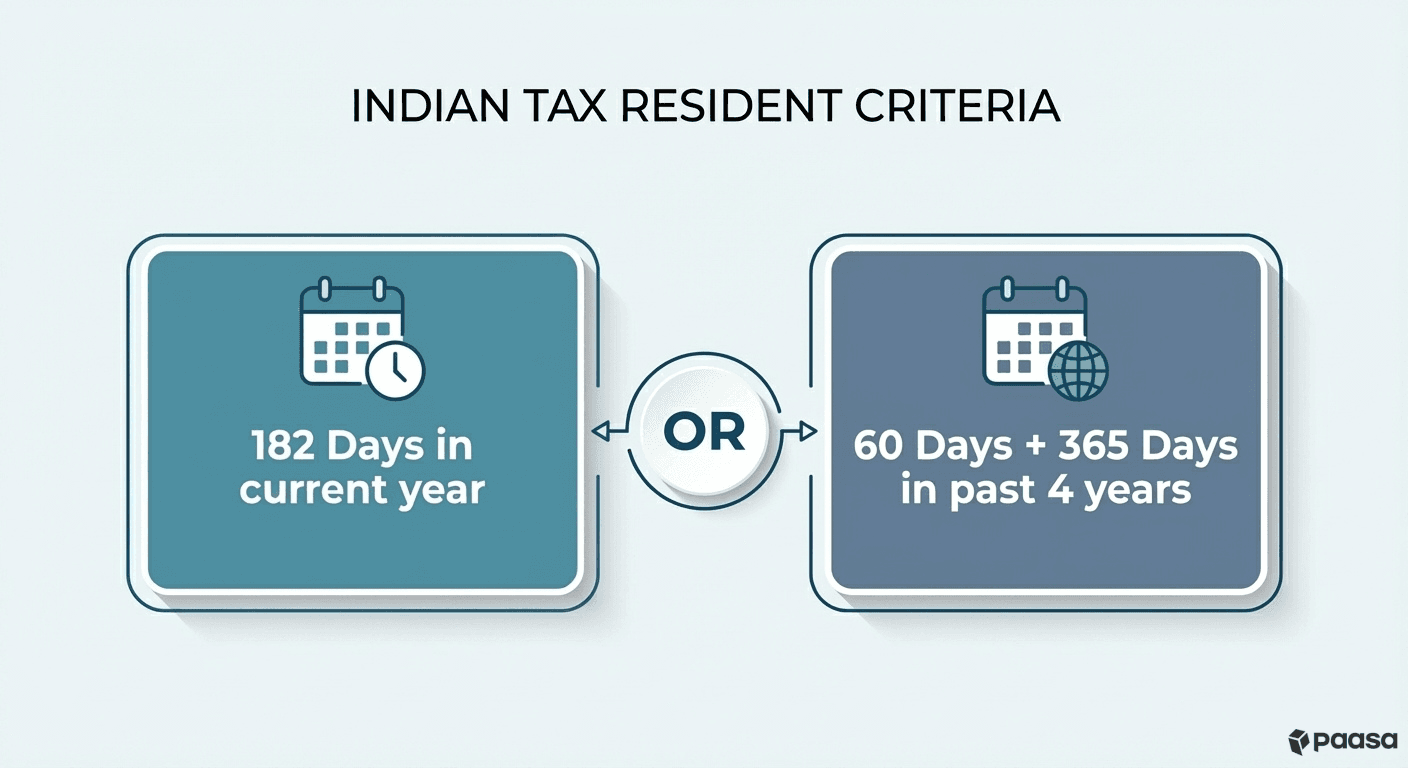

Under the Income Tax Act, you are considered a tax resident of India if:

- You are physically present in India for a period of 182 days or more in the tax year (182-day rule), or

- You are physically present in India for a period of 60 days or more during the relevant tax year and 365 days or more in aggregate in the four preceding tax years (60-day rule).

Once you meet this criterion, you are legally required to pay tax in India on income earned anywhere in the world, including Canadian interest, dividends, and capital gains.

What do I need to file in Canada before leaving?

Moving back to India does not automatically close your Canadian tax file. There are two specific filings to action in the year of departure.

Departure tax return (T1)

You must file a Canadian T1 departure return for the year you leave, with your departure date declared on the return. This return reports your income up to the departure date as a resident and declares the deemed disposition gains on your non-registered assets. The return is due by April 30 of the following year, or June 15 if you or your spouse had self-employment income. Filing late attracts interest and penalties on any tax owing.

Formal residency determination

If you want the CRA to formally confirm that your residency has ended, you can submit Form NR73. This is not mandatory but provides written confirmation of your non-resident status from a specific date, which is useful if you have ongoing Canadian income or if your residency status could be questioned later.

Note: Simply moving to India does not automatically sever Canadian tax residency. The CRA looks at residential ties including property owned or rented in Canada, a spouse or dependants remaining in Canada, Canadian bank accounts, a Canadian driver's licence, and provincial health coverage to determine when residency actually ended. Severing these ties formally at the time of departure is an important step to avoid being treated as a deemed resident with ongoing worldwide tax obligations.

Note: If you lived in Quebec, your provincial tax obligations do not automatically end when you move. Revenu Quebec operates independently from the CRA and administers its own provincial income tax at rates up to approximately 25.75%. If you have Quebec-source income after returning to India, such as rental income from a Quebec property or deferred compensation attributed to Quebec employment, you may have ongoing Quebec provincial filing obligations separate from your federal Canadian return. A Quebec-based tax advisor is worth consulting if you have any continuing Quebec-source income or unsettled ties to the province.

What is RNOR status and how does it affect me?

RNOR (Resident but Not Ordinarily Resident) is a transitional tax residency status for returning NRIs. It functions as a bridge between being a Non-Resident and becoming a full Ordinary Resident.

You typically qualify for this status if you meet one of the following criteria:

- You have been an NRI for 9 out of the last 10 financial years.

- You have lived in India for 729 days or less in the preceding 7 financial years.

This status grants you a 1 to 3-year window where your global income is treated differently from that of a standard Indian resident.

What benefits can I get from this status?

As long as you hold RNOR status, your foreign income is NOT taxable in India, provided it is received outside India first. This allows you to manage your Canadian assets without immediate tax liability in India.

- Global Stocks & ETFs: If you sell them while you are RNOR, the capital gains are tax-free in India. (Note: You still need to account for your Canadian tax obligations based on the departure tax).

- Canadian Bank Interest: The interest earned in your Canadian accounts is tax-free in India.

- RRSP/TFSA Protection: Any withdrawals or income generated within your Canadian registered accounts are not taxed by India during your RNOR window.

To utilize these exemptions, you must receive the funds in your Canadian bank account first. If you wire sale proceeds or dividends directly to an Indian bank account, the income is considered "received in India" and becomes fully taxable immediately.

Common Questions Canadian NRIs Have About Moving Back

Can I send money from India and buy more overseas stocks?

Yes. You can remit up to $250,000 USD equivalent per financial year under the Liberalised Remittance Scheme (LRS) to invest in foreign stocks. However, be aware that transfers exceeding ₹10 Lakhs in a year attract a 20% TCS (Tax Collected at Source), which you can claim back as a refund or tax adjustment when filing your income tax return in India.

When do I become subject to FEMA upon moving back?

You become a resident under FEMA immediately upon landing in India if your intention is to stay for an uncertain period or for employment and business. Unlike income tax residency (which counts days), FEMA residency applies the moment you return to settle.

Can I continue operating my Canadian bank account?

Yes. Section 6(4) of FEMA allows you to continue holding and operating foreign bank accounts, stocks, and properties if they were acquired when you were a resident outside India. You are not legally required to close them.

Can I keep my NRO account?

No. Once your status changes to Resident, you are legally required to inform your bank and convert your NRO account to a standard Resident Savings Account. Continuing to hold an NRO account as a resident is a violation of FEMA regulations.

About Paasa

Paasa is a global investing platform built specifically for Indian residents and returning NRIs. We provide direct access to over 10 global exchanges and support 9 global currencies, allowing you to build a truly international portfolio.

- Seamless "In-Kind" Transfers: You can move your entire global stock portfolio directly to Paasa. This allows you to consolidate your assets in one place without triggering a tax event.

- The Compliance Advantage: Paasa provides the exact reports you need for your Indian tax returns and foreign asset disclosures, eliminating the need for manual calculations.

- Estate Tax Protection: Paasa offers access to Ireland-domiciled (UCITS) ETFs, allowing you to legally shield your investments from the US Estate Tax if your portfolio includes US equities.