Indian investors don’t just need US exposure, they need the right way to access it.

Home to the S&P 500 and Nasdaq-100, the US market concentrates innovation (Apple, Microsoft, Nvidia), depth (thousands of liquid stocks and ETFs), and disclosure standards that are hard to match. For Indian investors, the challenge is not deciding whether to invest in the US, but figuring out how.

LRS paperwork, TCS deductions, dividend withholding, US estate tax, and the requirement to disclose foreign holdings all add layers of complexity. On top of that, there is confusion around fractional shares, UCITS, and feeder funds, which makes many investors hesitate.

This guide breaks down everything, helping you cut through the noise and make informed, compliant decisions about investing in the US stock market from India.

Table of Content

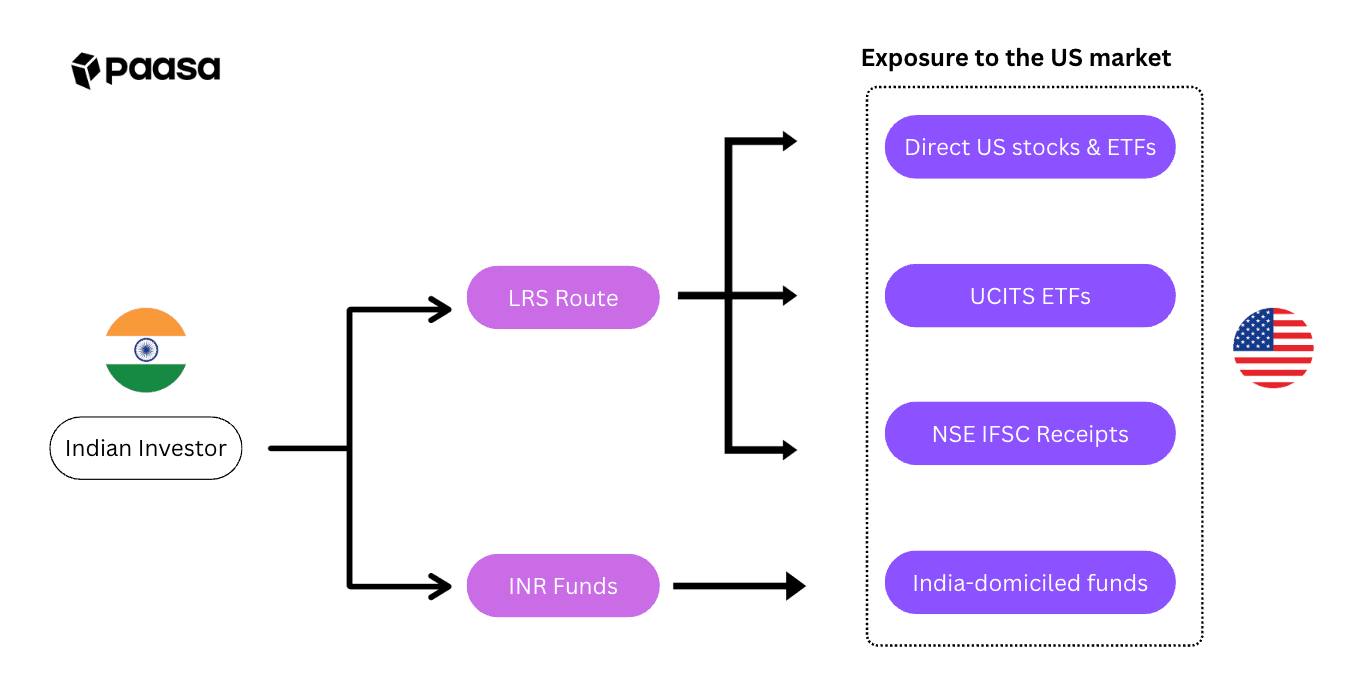

- Way 1: Buy US-listed Stocks and ETFs Directly

- Way 2: UCITS ETFs for US Exposure

- Way 3: NSE IFSC Receipts (GIFT City) for US Stocks

- Way 4: India-domiciled Funds with US Exposure

- Taxation: How Your Returns Are Treated in India

- Platforms that helps Indians invest in the US

- FAQs

- Conclusion

Buy US-listed Stocks and ETFs Directly

For Indian investors, the most common way to access the US market is to buy stocks and ETFs directly on US exchanges (NYSE/NASDAQ) through a global brokerage platform like Paasa. This is done under the RBI’s Liberalised Remittance Scheme (LRS), which allows each individual to remit up to USD 250,000 per financial year for investments abroad.

With this route, you can own US companies such as Apple, Microsoft, Amazon, Tesla, and Alphabet, as well as popular ETFs like SPDR S&P 500 ETF (SPY), Invesco QQQ Trust (QQQ), or iShares Core S&P 500 ETF (IVV).

And if you want to go beyond the US, Paasa also enables you to access other global markets. Explore our detailed guides:

- Invest in China from India

- Invest in Japan from India

- Invest in Ireland from India

- Invest in Switzerland from India

Key Points

- You own the real US-listed securities in your brokerage account.

- Requires INR to USD conversion and remittance under LRS (USD 250,000 annual cap).

- Banks deduct TCS on remittances above ₹10 lakh per FY; can be claimed back in your ITR.

- US dividends face 25% withholding tax for Indian residents after filing Form W-8BEN.

- No US capital gains tax for non-residents; gains are taxed in India at 12.5% LTCG (>24 months) or slab rate (STCG ≤24 months).

- US-situs assets face estate tax if total holdings exceed USD 60,000.

- Paasa allows fractional share investing (e.g., buy $100 of Apple instead of 1 full share).

- All foreign assets must be disclosed in Schedule FA of your Indian ITR.

Pros

- Direct exposure to the world’s biggest companies and most liquid ETFs

- Wide choice of sectors, themes, and index funds

- Fractional share investing lowers ticket size

- Transparent pricing and high liquidity on US exchanges

- Fully legal under LRS with RBI approval process

Cons

- Dividend withholding tax at 25% with no reclaim option for Indian residents

- US estate tax applies if assets exceed USD 60,000

- Requires paperwork for LRS remittance, Form W-8BEN, and Schedule FA in ITR (requires expert CA or global brokerage platform like Paasa to help with filings)

UCITS ETFs for US Exposure (LSE/Xetra)

Another practical way for Indians to gain exposure to US markets is through UCITS ETFs domiciled in Ireland or Luxembourg. These are Europe-based funds designed specifically for international investors. They track US indices like the S&P 500 or Nasdaq-100 but are listed on European exchanges such as the London Stock Exchange (LSE) or Xetra (Germany).

For Indian investors, UCITS ETFs are often more tax-efficient and estate-safe than buying US-domiciled ETFs directly. They avoid US estate tax, simplify dividend withholding (handled at the fund level), and still provide exposure to the same US companies like Apple, Microsoft, Amazon, Tesla, and Alphabet.

How Dividends Are Taxed in UCITS vs US ETFs?

One common area of confusion when comparing UCITS and US ETFs is how dividends are taxed. Let’s break it down.

US ETFs: These always distribute dividends. By default, the US applies a 30% withholding tax. But because India has a tax treaty (DTAA) with the US, this isn’t an extra tax. You simply report the dividend in India, pay tax at your income-slab rate, and the US withholding gets adjusted as credit.

Net outcome: your dividends are taxed at your Indian rate, no more, no less.

UCITS ETFs: Here’s where the distinction matters. At the fund level, Ireland already has a treaty with the US, so only 15% withholding happens when US companies pay dividends into the ETF. Now, for you as an Indian investor:

- If you pick an accumulating UCITS ETF, those dividends never get distributed to you - they’re automatically reinvested. Which means no Indian dividend tax, and your money compounds quietly inside the fund.

- If you pick a distributing UCITS ETF, then those payouts land in your account and get taxed in India at your slab rate. Since India doesn’t have a tax treaty with Ireland, there’s no credit mechanism for the 15% fund-level deduction.

What this means in practice: For most Indian investors, accumulating UCITS ETFs are the more tax-efficient choice. They avoid the friction of dividend taxation altogether, letting your returns build inside the fund without leakage.

Popular Examples

- iShares Core S&P 500 UCITS ETF (CSPX) – Ireland domiciled, tracks the S&P 500

- Vanguard S&P 500 UCITS ETF (VUSA) – Ireland domiciled, low cost

- Invesco Nasdaq-100 UCITS ETF (EQQQ) – Luxembourg domiciled, focuses on Nasdaq-100

- iShares MSCI USA UCITS ETF (CSUS) – broad US equity exposure

Key Points

- Domicile: Ireland or Luxembourg, outside the US, regulated under UCITS.

- Dividend Withholding Tax: US dividends face ~15% WHT at the fund level (US–Ireland treaty benefit), compared to ~30% if you buy US ETFs directly.

- No US estate tax exposure, unlike US-domiciled ETFs (which face estate tax above USD 60,000).

- Indian Taxation: <24 months holding = STCG taxed at slab rate; ≥24 months holding = LTCG at 20% with indexation

- Dividends are taxed at slab in India; foreign tax credit (FTC) generally not available since WHT is applied at the fund level.

- Requires a global broker like Paasa or IBKR. Most India-focused apps (INDmoney, Vested) don’t provide UCITS access.

Pros

- No US estate tax exposure

- Diversified access to US equities via a single instrument

- Lower dividend withholding (15% for UCITS vs 30% for US Stocks and ETFs)

- Strong liquidity on LSE/Xetra in USD, GBP, EUR

Cons

- Requires routing via LRS (USD 250,000 annual cap, TCS above ₹10 lakh)

- Expense ratios slightly higher than US ETFs (0.07–0.25% vs 0.03–0.10% for US-domiciled)

- Limited awareness among Indian retail investors; often overlooked in favor of US-domiciled ETFs

NSE IFSC Receipts (GIFT City) for US Stocks

In addition to remitting funds abroad under RBI’s Liberalised Remittance Scheme (LRS), Indian investors can also buy unsponsored depository receipts of US companies listed on NSE IFSC (GIFT City, Gujarat International Finance Tec-City). These are structured as INR-accessible USD securities and provide fractional exposure to US companies without needing a foreign broker account.

How It Works

- Each receipt represents a fraction of one US share (e.g., 25 or 50 receipts = 1 share).

- The receipts are backed by underlying shares held by a custodian overseas.

- Available companies include some of the world’s largest names like Apple, Amazon, Tesla, Microsoft, and Meta.

- Currently, the universe is limited to around 50 US large-cap stocks.

Key Points

- Fractional Investing: Makes high-priced US stocks accessible in smaller tickets.

- Trading Currency: Listed in USD, so funding still needs to go through RBI’s LRS framework (USD 250,000 annual cap, TCS above ₹10 lakh).

- Capital gains: Taxed in India as foreign securities (20% with indexation if held >24 months, slab for shorter periods).

- Dividends: Subject to US withholding tax (~25% after W-8BEN) and taxed again in India at slab, with foreign tax credit available.

- Trading volumes are still low compared to US markets; spreads can be wider.

Pros

- Provides a way to own marquee US stocks without a foreign brokerage account

- Fractional access makes otherwise expensive shares more affordable

- Regulated under Indian IFSC and SEBI framework

Cons

- Very limited stock universe (only top ~50 US companies available)

- Liquidity is shallow; order execution may not be smooth

- Still requires USD remittance under LRS, so it’s not “outside FEMA”

- No access to ETFs, UCITS, or the full breadth of US-listed securities

Our View: While NSE IFSC receipts are a step forward for retail investors, they’re restrictive in scope. If you want to build a serious global portfolio, it’s better to use a platform like Paasa or Interactive Brokers which provides direct access to the full US market (thousands of stocks, ETFs, and UCITS) and other global markets like China, Europe, UK along with FEMA compliance, tax-ready reporting, and INR-based analytics.

India-domiciled Funds with US Exposure

For Indians who want exposure to US markets without the paperwork of RBI’s Liberalised Remittance Scheme (LRS), the simplest option is to invest through India-domiciled mutual funds and ETFs. These are SEBI-regulated products, denominated in INR, and available on all major Indian brokerages and MF platforms.

How It Works

These funds are usually structured as feeder funds:

- The Indian AMC (like Motilal Oswal, Mirae, or Franklin) collects money in INR.

- The fund then invests into an offshore master fund or directly into US stocks/indices.

For the investor, it feels like any other mutual fund or ETF purchase in India.

Popular Examples

- Motilal Oswal Nasdaq 100 ETF / FoF – tracks the Nasdaq 100 index.

- Mirae Asset NYSE FANG+ ETF / FoF – focuses on top US tech names like Apple, Amazon, Tesla, and Meta.

- Franklin US Opportunities Fund – invests in a diversified basket of US growth companies.

- Edelweiss US Technology Equity FoF – invests in JP Morgan US Technology Fund.

(Availability may vary depending on SEBI’s overseas investment cap)

Key Points

- All investments are in INR, no USD conversion required.

- No LRS: You don’t need to use your USD 250,000 LRS limit or deal with bank remittances.

- Accessibility: Available via Zerodha, Groww, Paytm Money, or any MF distributor.

- Taxation in India: Treated as non-equity mutual funds (since underlying assets are foreign). >24 months: LTCG @ 12.5% (no indexation). ≤24 months: STCG at slab.

- SEBI Overseas Cap: AMCs face a USD 7 billion industry-wide limit for overseas MF investments. Once the cap is hit, some funds pause new inflows.

Pros

- Easiest way for Indians to access US stocks (INR-based, SEBI-regulated).

- No LRS paperwork, no TCS deduction.

- Simple to buy and redeem like any other MF/ETF.

- No estate tax or foreign tax credit filing required.

Cons

- Dependent on SEBI’s overseas cap - inflows can be restricted at times.

- Limited product shelf compared to what’s available via global brokers.

- Taxation is less favorable than Indian equity (no 10% LTCG regime).

- Indirect exposure: performance depends on the offshore master fund.

Taxation: How are your returns treated in India?

When you invest in the US from India, two layers apply:

- Foreign-side taxes: dividend withholding tax (WHT), any capital-gains tax at source, and potential estate/inheritance tax in the asset’s domicile.

- Indian taxation: how those dividends and capital gains are taxed when you file in India.

For how the double tax treaty taxes dividends, interest, and gains, read India–US DTAA.

Foreign-side taxes

Route | Asset domicile | Dividend WHT at source | Capital gains tax at source | Estate tax exposure |

Direct US stocks & ETFs | US | 25% after filing W-8BEN under the India–US treaty (otherwise 30%). No reclaim for individuals. | None | Yes, US estate tax above USD 60K |

UCITS ETFs | Ireland or Luxembourg | ~15% US WHT at the fund level (US–Ireland treaty). No Irish/Lux WHT to most non-resident investors with declaration. | None | None |

NSE IFSC Receipts | India | 25% US WHT flows through to the receipt | None | None |

India-domiciled funds | India | No foreign WHT passed on; distributions taxed directly in India | None | None |

Indian taxation

Assuming you are a resident individual in India (FY 2025–26 rules):

Route | Dividend income (India) | Capital gains (sale) |

Direct US stocks & ETFs | Taxed at your slab rate. Foreign Tax Credit (FTC) available for the 25% US WHT via Form 67. | >24 months: LTCG @ 12.5% (no indexation). ≤24 months: STCG at slab. |

UCITS ETFs | If distributing, taxed at slab in India. FTC is generally not available to the end-investor because the 15% WHT is suffered within the fund. (Accumulating share classes don’t distribute; nothing to declare until sale.) | >24 months: LTCG @ 12.5% (no indexation). ≤24 months: STCG at slab. |

NSE IFSC Receipts | Taxed at slab; FTC for US WHT via Form 67 | >24 months: LTCG @ 12.5% (no indexation). ≤24 months: STCG at slab. |

India-domiciled funds | Any distribution taxed at slab. | >24 months: LTCG @ 12.5% (no indexation). ≤24 months: STCG at slab. |

If you are already investing in the US, or are considering it and need clarity on how taxation applies to your situation, you can reach out to us at support@paasa.com

Our team works closely with HNIs, family offices, and institutional investors, and we have developed deep expertise in navigating the nuances of cross-border taxation, compliance, and reporting. We can help you understand the implications in detail and ensure your global investments are managed with the right structures in place.

Platforms that help Indians invest in the US

While the investment routes are clear, the ease of access depends on the platform you use. Below is a comparison of commonly used platforms by Indian investors, showing which US routes they enable and what additional services they provide.

Paasa | IBKR | INDmoney | Vested | Kristal | Zerodha | Groww | |

Direct US stocks & ETFs | ✅ | ✅ | ✅ | ✅ | ✅ | ❌ | ❌ |

UCITS ETFs | ✅ | ✅ | ❌ | ❌ | ✅ | ❌ | ❌ |

NSE IFSC Receipts | ❌ | ❌ | ✅ | ❌ | ❌ | ✅ | ✅ |

India-domiciled funds | ✅ | ❌ | ✅ | ❌ | ❌ | ❌ | ❌ |

FEMA compliance support | ✅ | ❌ | ❌ | ❌ | ❌ | ❌ | ❌ |

Tax reporting support | ✅ | ❌ | ❌ | ❌ | ❌ | ❌ | ❌ |

INR-based analytics | ✅ | ❌ | ❌ | ❌ | ❌ | ❌ | ❌ |

Want a deeper breakdown?

If you’re comparing platforms, we’ve written detailed guides:

They cover infrastructure, features, FEMA compliance, tax handling, and investor fit in detail, so you can choose the platform that best matches your needs.

Conclusion

For Indian investors, the US remains the world’s most important market to allocate to. The challenge isn’t access anymore, it’s choosing the route that balances costs, taxation, estate rules, and convenience.

- If you want breadth and flexibility, direct US stocks and ETFs are the natural choice.

- If you care about tax efficiency and estate safety, UCITS ETFs are often superior.

- If you prefer simplicity in INR, India-domiciled funds work, but with trade-offs in tax and product range.

- If you’re curious about GIFT City receipts, know that they’re still limited in scope.

The right route depends on your ticket size, your tax situation, and how much complexity you’re willing to manage.

About Paasa

Paasa is built as a global-first investing platform for Indian investors. We help HNIs, family offices, and institutions move beyond domestic assets and build portfolios that include the US, Europe, Japan, China, Switzerland, and other key markets.

Our platform is powered by global brokerage infrastructure, giving you direct access to thousands of stocks, ETFs, UCITS funds, and other instruments.

Relevant Reads

Compare routes, costs, and taxes across markets with these quick reads.

- Invest in Ireland from India

- Invest in Switzerland from India

- Invest in China from India

- Invest in Japan from India

- Invest in Singapore from India

- Invest in UK from India

- Invest in Poland from India

- Invest in Germany from India

Disclaimer

This blog is for informational purposes only and does not constitute investment, tax, or legal advice. The content is based on publicly available sources and our interpretation of current regulations, which are subject to change. Investing in international markets, including the US, carries risks such as currency fluctuations, regulatory changes, tax implications, and market volatility. Past performance should not be taken as a guarantee of future returns. Investors are advised to consult their financial, tax, and legal advisors before making any investment decisions.