For Indian investors, Switzerland represents stability, quality, and global brand power. Companies like Nestlé, Roche, Novartis, and UBS are not just Swiss champions, they are household names across the world.

The Swiss Market Index (SMI) offers exposure to a concentrated basket of these blue-chip giants, making Switzerland an attractive allocation within a globally diversified portfolio.

This guide brings everything together - how Indians can invest in Switzerland, the different routes available, the taxes and costs involved, and the platforms through which access is possible.

Table of Content

- Can Indians invest in Swiss stocks directly?

- Way 1: Direct Swiss Shares on Swiss Exchange

- Way 2: UCITS ETFs with Swiss Exposure

- Way 3: US-domiciled Swiss ETFs

- Way 4: ADRs of Swiss Companies

- Taxation and Costs for Indians Investors

- Platforms that helps access

- FAQs

- Conclusion

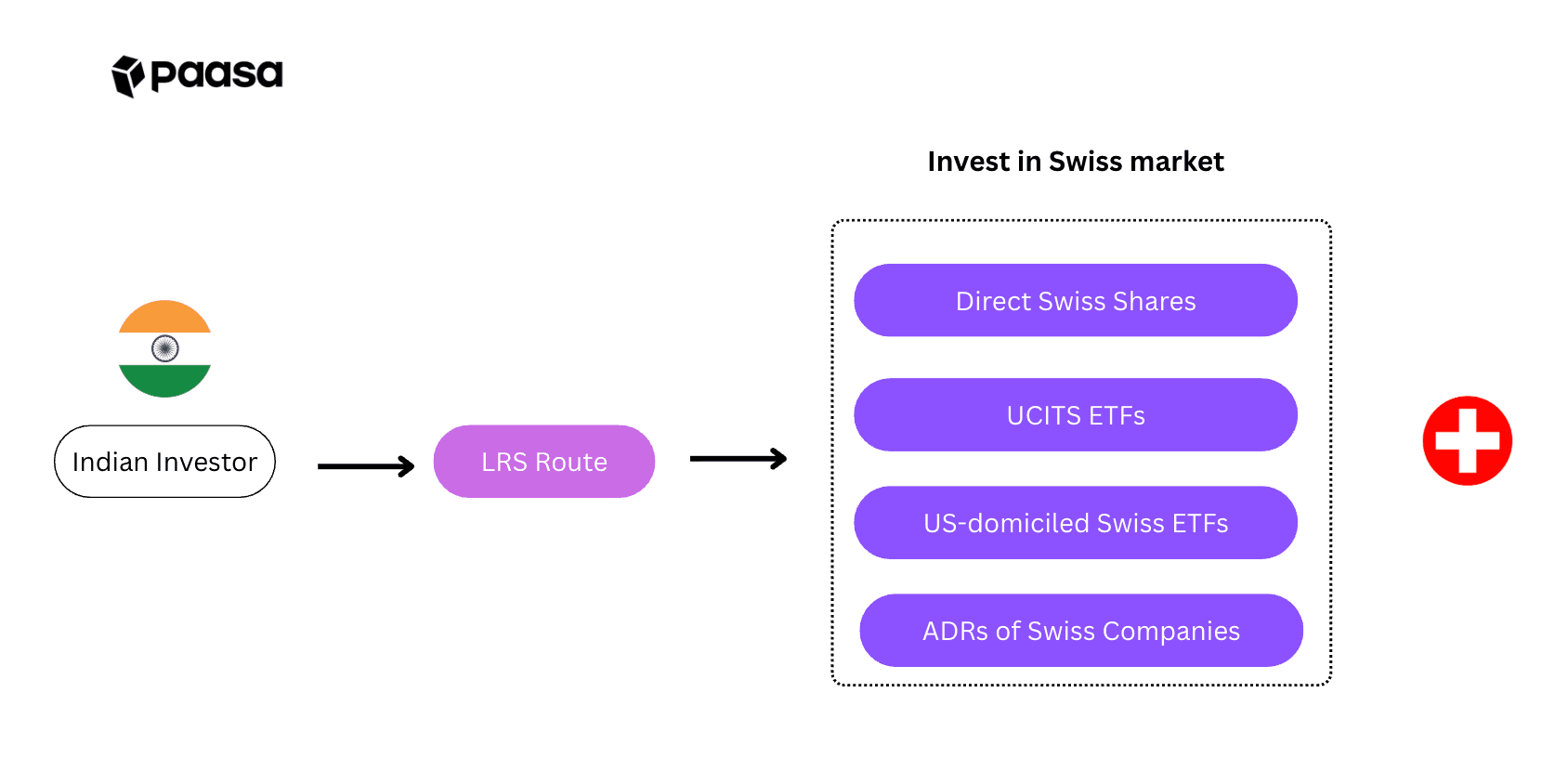

Can Indians invest in Swiss stocks directly?

Yes. Indian residents are permitted to invest in overseas equities, including Swiss stocks, under the Liberalised Remittance Scheme (LRS) of the Reserve Bank of India (RBI).

Under LRS, each individual can remit up to USD 250,000 per financial year for permitted capital account transactions, which include investing in foreign shares and ETFs.

In practice, this means an Indian investor can open an account with a global broker platform such as Paasa, remit funds abroad using the correct purpose code for equity investment, and legally purchase Swiss equities or ETFs.

The four practical routes to gain exposure to Switzerland are:

- Direct Swiss shares on SIX

- UCITS ETFs with Swiss exposure

- US-domiciled Swiss ETFs

- Swiss ADRs on US exchanges

Important to know:

- The annual LRS limit is USD 250,000 per individual.

- Remittances above ₹10 lakh attract TCS (Tax Collected at Source) at the bank level.

- All foreign assets must be disclosed in your Indian Income Tax Return (ITR).

Direct Swiss Shares on SIX (Swiss Exchange)

The SIX Swiss Exchange is the primary stock exchange in Switzerland, home to global blue chips such as Nestlé (NESN), Roche (ROG), and Novartis (NOVN). Through global brokers like Paasa and Interactive Brokers (IBKR), Indian investors can remit funds abroad under the RBI’s Liberalised Remittance Scheme (LRS) and purchase these shares directly in Swiss francs (CHF).

For Indians, this is the cleanest way to hold Swiss equities in their original market.

Key points:

- Dividends: Switzerland levies a 35% withholding tax (WHT) on dividends by default. Under the India–Switzerland DTAA, this can be reduced to 10% from Jan 2025, but only if investors file a refund claim with the Swiss Federal Tax Administration. Otherwise, the 35% is withheld and not fully creditable.

- Capital gains: Non-resident investors do not pay Swiss capital gains tax. Gains are only taxable in India as per slab rates.

- Currency: Shares are priced in Swiss francs (CHF). Investors face FX exposure (INR/CHF) in addition to equity risk.

- Estate tax: Switzerland does not impose estate tax on non-residents, unlike the US.

- Compliance: Remittances must be made under LRS (USD 250,000 annual cap per person). Correct purpose code for “equity investment abroad” is required.

Pros:

- Direct ownership of Swiss blue chips (Nestlé, Roche, Novartis).

- Voting rights and corporate action entitlements.

- No US estate tax risk (unlike US ETFs/ADRs).

- Recognised and fully legal under FEMA LRS.

Cons:

- High dividend WHT (35%), with refund paperwork required to reduce to 10%.

- Trading fees on SIX are usually higher than US or European exchanges.

UCITS ETFs with Swiss Exposure

Another practical way for Indians to gain exposure to Swiss equities is through UCITS ETFs domiciled in Ireland or Luxembourg.

UCITS ETFs are Europe-domiciled funds that give investors exposure to Swiss equities while being regulated under the UCITS framework. They trade on exchanges such as the London Stock Exchange (LSE), Xetra (Germany), and SIX (Switzerland), and are built for international investors.

For Indians, UCITS ETFs are often the most practical and tax efficient way to invest in Switzerland. They sidestep US estate tax, handle Swiss withholding at the fund level, and provide access to a diversified basket of Swiss companies including Nestlé, Roche, and Novartis.

Popular examples include:

- iShares MSCI Switzerland UCITS ETF (Ireland domiciled)

- Amundi MSCI Switzerland UCITS ETF (Luxembourg domiciled)

If you want a deeper dive on why UCITS are often better suited for Indian investors, see our detailed blog here: Why Indian Investors Should Choose UCITS.

Key points:

- Ireland or Luxembourg domiciled ETFs, regulated under UCITS. Listed on LSE, Xetra, or SIX in USD, GBP, EUR, or CHF.

- Requires a global platform like Paasa, since most India focused apps do not provide UCITS access.

- Underlying Swiss company dividends (Nestlé, Roche, Novartis) face 35% WHT, but this is handled at the fund level. Investors simply receive net distributions.

- In India, dividends are taxed at slab and capital gains at 10% (LTCG if >12 months for listed units, STCG at slab).

- UCITS ETFs avoid US estate tax risk, making them safer for HNIs and family offices with larger allocations.

Pros:

- No US estate tax exposure.

- Diversified access to the Swiss equity market through a single instrument.

- Lower administrative burden compared to holding Swiss shares directly.

- Traded on major European exchanges with good liquidity.

Cons:

- Must route via LRS (USD 250,000 annual cap, TCS, paperwork).

- Expense ratios are slightly higher than US ETFs (typically 0.25–0.5 percent).

Use our UCITS Screener to discover and compare UCITS-compliant investment instruments.

US-domiciled Swiss ETFs

For Indian investors who already have exposure to US markets, one of the most convenient ways to invest in Switzerland is by buying US-domiciled ETFs that hold Swiss equities. These ETFs are listed on American exchanges, priced in USD, and can be purchased legally under RBI’s LRS through Paasa.

Many Swiss companies or indices are packaged into US-listed ETFs to make them accessible to global investors. This gives Indians the ability to tap into Switzerland’s equity market without directly trading in Europe or Switzerland.

Popular options include:

- iShares MSCI Switzerland ETF (EWL) – the flagship fund tracking around 40 Swiss large and mid-cap companies such as Nestlé, Roche, Novartis, and UBS.

- Franklin FTSE Switzerland ETF (FLSW) – a lower-cost alternative to EWL with similar exposure.

- iShares Currency Hedged MSCI Switzerland ETF (HEWL) – holds the same basket as EWL but hedges CHF/USD currency risk.

Key points:

- Domicile: US-domiciled ETFs, regulated under US law, traded in USD on NYSE/NASDAQ.

- Holdings: Provide diversified access to Swiss equities. EWL and FLSW cover the MSCI Switzerland Index, HEWL adds currency hedging.

- Dividends: Dividends face 25% US withholding tax for Indian investors after filing W-8BEN. Unlike UCITS, there is no reclaim option.

- Capital gains: No US capital gains tax for non-residents. Gains are taxed in India at 10% LTCG (>12 months) or slab (STCG).

- Estate tax: US-situs assets are exposed to US estate tax if holdings exceed USD 60,000.

- Compliance: Fully legal under RBI’s LRS with an annual cap of USD 250,000 per individual.

Pros:

- Easy to access if you already invest in US stocks (Paasa, INDmoney or Vested)

- High liquidity on US exchanges.

- Multiple ETF choices beyond EWL, including cost-efficient and hedged products.

- Clean execution in USD, with familiar settlement and reporting.

Cons:

- 25% US dividend withholding with no treaty reclaim for Indian Investors.

- US estate tax exposure above USD 60,000.

- Less tax-efficient than Ireland or Luxembourg domiciled UCITS ETFs.

ADRs of Swiss Companies

Several large Swiss companies are also available in the US as American Depositary Receipts (ADRs). ADRs are certificates issued by US banks that represent shares in foreign companies, making it easier for global investors to trade them on US exchanges in USD.

For Indian investors, ADRs of Swiss companies like Nestlé (NSRGY), Novartis (NVS), and Roche (RHHBY) offer a way to own some of Switzerland’s best-known names through US markets. These can be purchased under RBI’s LRS through Paasa.

Key points:

- Structure: ADRs are issued by US banks and represent one or more shares of a foreign company. They trade on US exchanges in USD.

- Holdings: Popular Swiss ADRs include Nestlé, Novartis, Roche, UBS, and Zurich Insurance.

- Dividends: ADR dividends typically pass through the Swiss withholding tax of 35 percent. Under the India–Switzerland tax treaty, this can be reduced to 10 percent if a refund is filed with the Swiss tax authority, but ADR holders still need to navigate reclaim paperwork.

- Capital gains: No US capital gains tax for non-residents. Gains are taxed in India.

- Estate tax: As US-situs assets, ADRs are exposed to US estate tax if holdings exceed USD 60,000.

- Compliance: Eligible under RBI’s LRS limit of USD 250,000 per year.

Pros:

- Provides exposure to global Swiss brands through familiar US markets.

- Traded in USD with decent liquidity

- Easier to buy than direct Swiss shares on SIX.

- Fully legal under LRS and supported by Paasa.

Cons:

- Dividends still subject to 35 percent Swiss WHT, with reclaim paperwork needed to bring it down to 10 percent.

- US estate tax exposure above USD 60,000.

- Fewer ADRs compared to the number of Swiss companies listed on SIX, so exposure is limited to the biggest names.

Taxation: How are your returns treated in India?

When investing in Switzerland through offshore routes, Indian investors face two layers of taxation:

- Foreign-side taxes: withholding tax (WHT) on dividends, capital gains tax (if any), and estate tax exposure in the country of domicile.

- Indian taxation: how those dividends and capital gains are taxed when you file your return in India.

For how the double tax treaty taxes dividends, interest, and gains, read India–Swiss DTAA.

The interaction of these two layers determines your net outcome. Below is a structured comparison across the four practical routes.

Foreign-side taxes

Indian taxation

Assuming you are a resident individual in India (FY 2025–26 rules):

Platforms that enable access

Indian investors cannot open an account directly with the Swiss exchange (SIX). Instead, access happens through global brokerage platforms that support overseas equities and ETFs.

Paasa is the most practical route for Indians, since it not only provides global market access but also adds the India-facing layer you need: FEMA compliance, INR-based tracking, and tax-ready reporting. Through Paasa, you can access:

- Direct Swiss shares on SIX (Nestlé, Novartis, Roche, UBS)

- UCITS ETFs domiciled in Ireland or Luxembourg that trade on LSE, Xetra, or SIX

- US-domiciled Swiss ETFs like EWL and FLSW

- Swiss ADRs trading on US exchanges

Other “US-only” apps in India (like INDmoney, Vested, or Groww) limit access to US-listed stocks and ETFs only. They do not support UCITS ETFs or direct Swiss equities, which makes them unsuitable for Swiss market exposure.

Want a deeper breakdown?

If you’re comparing platforms, we’ve written detailed guides:

They cover infrastructure, features, FEMA compliance, tax handling, and investor fit in detail, so you can choose the platform that best matches your needs.

Conclusion

For Indian HNIs and family offices looking at Switzerland, the pattern is becoming clear. UCITS ETFs are emerging as the default vehicle for long-term allocations, offering efficiency, tax clarity, and estate-safety. US-domiciled ETFs and Swiss ADRs add liquidity and convenience for investors already active in US markets, while direct Swiss shares on SIX remain valuable for those who want pure exposure to blue-chip names like Nestlé, Roche, or Novartis.

At Paasa, we believe the most resilient portfolios don’t rely on a single route. They combine UCITS ETFs as the core, with direct Swiss equities or US-listed instruments for targeted bets, all managed cleanly under LRS with FEMA compliance and tax-ready reporting in India.

About Paasa

Paasa is built as a global-first investing platform for Indian investors. For HNIs, family offices, and institutions, we provide structured access not only to US markets but also to Europe (UCITS), Switzerland, London, China, and beyond.

Whether your allocation is into UCITS ETFs listed on LSE or Xetra, US-listed ADRs of Swiss companies, US-domiciled ETFs like EWL, or direct Swiss shares on SIX, Paasa enables all the practical routes available today. More importantly, we handle the India-facing side of global investing from LRS flows and FEMA compliance to tax reporting and INR-based analytics.

This way, you can focus on building a globally diversified portfolio that includes Switzerland and other key markets, while we simplify the cross-border complexity behind the scenes.

Relevant Reads

Compare routes, costs, and taxes across markets with these quick reads.

- Invest in US from India

- Invest in Ireland from India

- Invest in China from India

- Invest in Japan from India

- Invest in Singapore from India

- Invest in UK from India

- Invest in Poland from India

- Invest in Germany from India

Disclaimer

This blog is for informational purposes only and should not be considered investment, tax, or legal advice. The information presented is based on publicly available data and our understanding of current regulations, which may change over time. Investing in international markets, including China, involves risks, including currency risk, political risk, and market volatility. Past performance is not indicative of future results. Investors should consult their financial, tax, and legal advisors before making any investment decisions.