When Indians look beyond the US for global exposure, Ireland almost always appears on the shortlist. That’s because Ireland is the home of UCITS ETFs, funds designed for international investors, with cleaner dividend treatment and no US estate tax. Add to that globally known companies like CRH, Kerry, and Ryanair, and Ireland becomes a natural destination for global allocations.

The problem is, most Indians only get bits and pieces. Some hear “just buy the ADR in New York,” others say “look at the London listings,” and some push UCITS without really explaining the tax side.

This blog puts everything together, the actual ways Indians can invest in Ireland, what taxes and costs apply, and which route might fit your portfolio best.

Table of Content

- Can Indians invest in Irish stocks directly?

- Way 1: US-listed Irish companies and ADRs

- Way 2: LSE-listed Irish stocks

- Way 3: UCITS ETFs (Ireland-domiciled)

- Taxation and Costs for Indian Investors

- Platforms that help access

- FAQs

- Conclusion

Can Indians invest in Irish stocks directly?

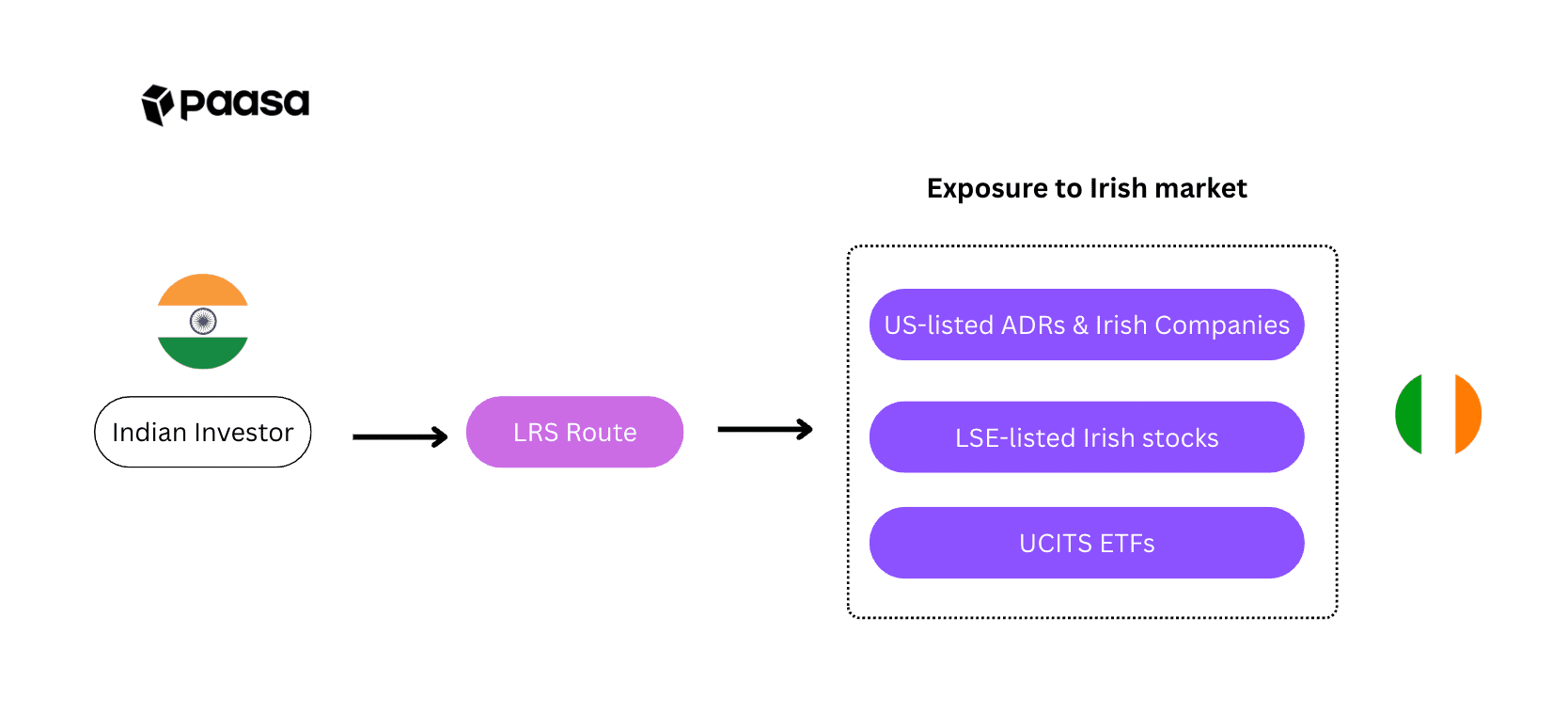

The short answer is ‘No’, Indian residents cannot open a direct trading account with an Irish broker to buy shares on Euronext Dublin (Ireland’s stock market).

Instead, access happens through international routes:

- US-listed Irish companies or ADRs (e.g., CRH, Flutter, Ryanair ADR).

- London Stock Exchange (LSE) listings of Irish companies (e.g., Kerry, Kingspan).

- Ireland-domiciled UCITS ETFs that trade on European exchanges like LSE or Xetra (e.g., CSPX, VWCE, IWDA).

For Indian investors, all three routes are fully legal, practical, and accessible through global platforms like Paasa.

Important to know:

- All overseas investments by resident Indians, whether in US stocks, UK shares, or Irish UCITS ETFs must be made under the RBI’s Liberalised Remittance Scheme (LRS).

- The limit is USD 250,000 per person per financial year.

- Above ₹10 lakh, banks deduct TCS (Tax Collected at Source) on remittances.

- All foreign assets must be reported in your Indian Income Tax Return (ITR).

US-listed Irish companies and ADRs

American Depositary Receipts (ADRs) are certificates issued by US banks that represent shares of foreign companies. Instead of buying the stock in its home market, investors can trade the ADR on US exchanges in USD, with the ADR price designed to mirror the underlying share.

Irish multinationals have tapped US markets in two ways:

- Direct US primary listings: companies like CRH plc (NYSE: CRH) and Flutter Entertainment (NYSE: FLUT) have shifted their main trading line to the US. Investors buying these stocks in New York are holding the company’s actual shares, not receipts.

- ADRs: companies like Ryanair Holdings (NASDAQ: RYAAY) issue ADRs backed by their Irish shares. Here, a US depositary bank holds the underlying Dublin-listed stock and issues receipts to trade in the US.

For Indian investors, both routes count as US-situs securities under RBI’s LRS.

Key points:

- Dividends: Whether it’s a primary listing or ADR, dividends from Irish companies face Irish Dividend Withholding Tax (DWT) — 25% by default. Under the India–Ireland DTAA this can be reduced to 10%, but only if you file the correct forms (Revenue V2A/V2B) with the registrar/depositary before the record date. Otherwise, 25% is withheld and you must reclaim it later.

- Stamp duty: Buying ADRs in the US doesn’t usually trigger Irish stamp duty, though creating/cancelling ADRs behind the scenes can involve 1% Irish stamp duty. Direct US listings are not subject to this.

- Estate tax: Both ADRs and US primary listings are considered US-situs assets, exposing Indian investors to US estate tax — up to 40% on holdings above USD 60,000.

- Indian taxation: Dividends are taxed at your income-slab rate in India.

Pros:

- Access to Irish blue chips with deep liquidity.

- Traded in USD during US market hours (fits easily into existing US portfolios).

- Available via most US-focused investment apps in India.

Cons:

- Must route via LRS (USD 250,000 annual cap, paperwork, TCS above ₹10 lakh).

- Irish DWT applies to dividends unless exemption paperwork is in place.

- US estate tax risk on holdings above USD 60,000.

LSE-listed Irish stocks

Many Irish multinationals are also listed on the London Stock Exchange (LSE), giving investors another route to gain exposure. These are the same Irish-incorporated companies, but their shares trade in London alongside other global equities.

Examples include:

- Kerry Group (KYGA, LSE) – a global leader in food ingredients.

- Kingspan Group (KGP, LSE) – an insulation and building materials giant.

Instead of buying Kingspan shares in Dublin (ticker: KRX ID), an Indian investor can buy Kingspan’s London-listed shares (ticker: KGP) on the LSE. The London line represents the same underlying Irish company, but trades in GBP during UK market hours.

Key points:

- You directly own the London-listed shares of Irish-incorporated companies, traded in GBP.

- Dividends declared by these companies remain subject to Irish Dividend Withholding Tax (DWT) at 25% by default. For Indian residents, this can be reduced to 10% under the India–Ireland DTAA, and DWT on Irish company dividends can be reduced to 0% if the exemption paperwork (Form V2) is filed.

- Purchases of Irish-incorporated company shares generally attract 1% Irish stamp duty, even when traded in London.

- As with all offshore investing, Indian residents must route transactions under the Liberalised Remittance Scheme (LRS).

Pros:

- Access to Irish blue-chip companies through one of the world’s deepest and most liquid exchanges.

GBP-denominated trading may suit investors diversifying beyond USD. - London market hours (overlapping with India’s day) are convenient for tracking and trading.

- Brokers with LSE access are common among global platforms like IBKR and Paasa.

Cons:

- Must route via LRS (paperwork, TCS, USD 250,000 annual cap).

- Irish DWT still applies to dividends, with relief only if proper forms are filed.

- 1% Irish stamp duty applies to transfers of Irish-incorporated shares, regardless of trading venue.

- FX costs for INR–GBP conversion add another layer of expense.

UCITS ETFs (Ireland-domiciled)

UCITS ETFs are funds domiciled in Ireland or Luxembourg and regulated under the European UCITS framework. Ireland is the global hub for UCITS, making it the default structure for international ETFs that are designed to be more tax-efficient for non-US investors.

If you’d like a detailed comparison, see our UCITS vs US ETFs guide for Indian Investors.

Instead of buying a US-listed ETF like SPY (which exposes you to US estate tax and 25% dividend withholding), an Indian investor can buy an Ireland-domiciled S&P 500 UCITS ETF (for example, CSPX on the London Stock Exchange). The fund structure allows you to hold the same index exposure but with cleaner tax outcomes and without US estate tax risk.

Key points:

- Fund domicile: Ireland or Luxembourg, regulated under UCITS.

- Ireland does not levy withholding tax on distributions to non-residents. Underlying US dividends inside a UCITS (e.g., in S&P 500 ETFs) suffer ~15% WHT at fund level, but that’s still more efficient than the 25% WHT you’d face holding a US ETF directly.

- UCITS avoid US estate tax risk, unlike US ETFs.

- Currencies and exchanges: Listed in USD, GBP, or EUR on LSE, Xetra, and other European markets.

- Product breadth: Global equity ETFs (VWCE, IWDA), regional allocations, bond ETFs, and thematic funds like China UCITS.

Pros:

- Tax efficiency: Lower dividend tax drag vs US ETFs.

- Estate tax protection: No US estate tax exposure.

- Broad selection: Thousands of ETFs across asset classes and regions.

- Global standard: Used by HNIs, family offices, and institutions worldwide.

- Available across exchanges: LSE, Xetra, SIX, Borsa Italiana.

Cons:

- Must route via LRS (paperwork, TCS, USD 250,000 cap).

- Requires a global broker (Paasa or IBKR); not available on US-only apps like INDmoney or Vested.

- FX conversion costs (INR → USD/EUR/GBP).

- Liquidity can be thinner compared to US ETFs (though still adequate for most allocations).

Use our UCITS Screener to discover and compare UCITS-compliant investment instruments.

Taxation and Costs for Indians Investors

When you buy Irish exposure from India, two layers matter:

- Foreign side (what Ireland, the US or the UK may take at source), and

- India side (your final tax when you file ITR).

Below is a structured comparison across the three practical routes available to Indian investors.

Foreign-side taxes

Foreign-side taxes:

Indian taxation:

Assuming you are a resident individual in India (FY 2025–26 rules)

UCITS vs US ETFs: Dividend Advantage

One of the biggest reasons global investors including more and more Indians prefer Ireland-domiciled UCITS ETFs over US ETFs comes down to how dividends are taxed.

- US ETFs: If an Indian investor holds a US-listed ETF (like SPY), dividends from US companies face a 25% withholding tax at source. These dividends then get taxed again at your income slab in India, though you can claim credit for the US tax deducted.

- UCITS ETFs: If you buy an Ireland-domiciled UCITS ETF holding US stocks (like CSPX), the fund itself benefits from the US–Ireland tax treaty, which caps withholding at 15% instead of 25%. That deduction happens at the fund level, so it never shows up on your statement. If you choose an accumulating UCITS ETF, no dividends are paid out to you at all - they’re reinvested within the fund, which means no Indian dividend tax either.

The result: UCITS ETFs don’t just avoid US estate tax, they also deliver lower dividend leakage compared to US ETFs. For Indian investors focused on long-term compounding, this tax efficiency is a major reason UCITS are increasingly the smarter default.

If you’d like a full breakdown of how UCITS ETFs work and why they are usually better than US ETFs for Indian investors, check out our detailed guide here.

Platforms that enable access

The good news is that Indian investors today have multiple global platforms that make investing in Irish companies and UCITS ETFs straightforward.

Some platforms go a step further by simplifying FEMA compliance, LRS remittances, and Indian tax reporting, so you don’t have to worry about the paperwork.

The table below highlights which platforms cover which routes, and what additional support they provide.

For serious allocations and cross-border compliance, Paasa is often the smoother choice since it manages FEMA, LRS flows, and tax reporting end-to-end, letting you focus on the investments themselves.

Want a deeper breakdown?

If you’re comparing platforms, we’ve written detailed guides:

They cover infrastructure, features, FEMA compliance, tax handling, and investor fit in detail, so you can choose the platform that best matches your needs.

Conclusion

We’re seeing a strong shift among Indian HNIs and family offices, UCITS ETFs are becoming the default for long-term allocations, while US and London lines are used for stock-specific exposure.

UCITS provides efficiency and compliance comfort; US ADRs and LSE shares add liquidity and flexibility.

At Paasa, we believe the smartest portfolios don’t choose one over the other, they combine UCITS for core holdings and direct Irish equities for precision bets, all managed under LRS with clean reporting in India.

About Paasa

Paasa is designed as a global-first investing platform for Indian investors. For HNIs, family offices, and institutions, we provide structured access not just to US markets, but also to London, Europe (UCITS), China, and beyond.

Whether your allocation is into UCITS ETFs listed on LSE/Xetra, US-listed ADRs of Irish companies, or direct LSE shares, Paasa enables all the practical routes available today. More importantly, we handle the India-facing side of global investing from LRS flows and FEMA compliance to tax reporting and INR-based analytics.

This way, you can focus on building a globally diversified portfolio that includes Ireland and other key markets, while we simplify the cross-border complexity behind the scenes.

Relevant Reads

Compare routes, costs, and taxes across markets with these quick reads.

- Invest in US from India

- Invest in Switzerland from India

- Invest in China from India

- Invest in Japan from India

- Invest in Singapore from India

- Invest in UK from India

- Invest in Poland from India

- Invest in Germany from India

Disclaimer

This blog is for informational purposes only and should not be considered investment, tax, or legal advice. The information presented is based on publicly available data and our understanding of current regulations, which may change over time. Investing in international markets, including China, involves risks, including currency risk, political risk, and market volatility. Past performance is not indicative of future results. Investors should consult their financial, tax, and legal advisors before making any investment decisions.