If you are an Indian tech professional and you have just returned to India (or planning to return) after working abroad, the transitional tax residency status of Resident but Not Ordinarily Resident (RNOR) gives you an opportunity to restructure your equity and RSUs for much higher long term returns.

This guide covers everything you need to know about restructuring equity while you are an RNOR, including who can do it, how you can do it, and advantages it provides.

Table of contents

- Who is considered RNOR?

- What are the tax advantages?

- How to restructure equity while RNOR?

- RNOR in India but a US tax resident?

Who is considered RNOR?

To qualify as Resident but Not Ordinarily Resident, you must first be considered a "Resident" of India for the current year.

Once you are a Resident, you fall into the special RNOR category if you meet ANY ONE of the following criteria:

- You were a Non-Resident (NRI) in at least 9 out of the 10 financial years immediately preceding the current year.

- You were physically present in India for 729 days or less in total during the 7 financial years immediately preceding the current year.

- If you are an Indian Citizen or Person of Indian Origin (PIO) with Indian income exceeding ₹15 Lakhs, you become an RNOR if you stay in India for 120 to 181 days (instead of the usual 182).

- If you are an Indian Citizen with Indian income exceeding ₹15 Lakhs and you are not liable to tax in any other country, you are automatically treated as a "Deemed Resident" in India. Deemed Residents are always classified as RNORs.

How long does it last?

The RNOR status can last from 1 to 3 years.

Most returning NRIs enjoy this status for 2 full financial years after the year they return. In some cases (depending on your arrival date), it can stretch to 3 years.

Once this period ends, you become an Ordinary Resident (ROR), and your global income becomes fully taxable in India.

What are the tax advantages of restructuring equity while I am an RNOR?

While you are an RNOR, India does not tax your foreign income, including capital gains from selling foreign stocks (like US-listed stocks and ETFs), provided the proceeds are received directly in a foreign brokerage or bank account.

If you have also ceased to be a tax resident of your previous country (e.g., the US), you enter a unique period where neither India nor your previous country taxes your capital gains.

The biggest advantage of this tax-free period created by the RNOR status is the ability to perform a "Cost Basis Reset" on your foreign assets.

Resetting Your Cost Basis

Most early employees or long-term tech workers hold RSUs with a very low "Cost Basis" (the price at vesting).

If you hold these stocks until you become an Ordinary Resident (ROR), you will eventually pay Indian capital gains tax on the entire appreciation from the day they vest to the day you sell.

However, if you sell and repurchase them while you are an RNOR, you can legally eliminate the tax on all past growth.

- Sell the Stock: You sell your RSUs/equity while you are RNOR.

- Tax-Free Gain: The profit you make (Capital Gain) is tax-free in India (because you are RNOR) and likely tax-free abroad (if you are a non-resident there).

- Buy Back Immediately: You immediately use the proceeds to buy the same stock back.

- The Benefit: Your new "Cost Basis" is now the current market price. When you eventually sell these stocks years later as a full Indian resident, you will only be taxed on the growth from this new, higher price, not the original low price.

Example

Suppose you are a software professional who is currently an RNOR in India and not a US tax resident.

You hold equity worth $1 million, which includes your vested RSUs. Your original cost of acquisition was $200,000.

You plan to hold this equity for another 5 years, by which time the value appreciates to $2 million.

Scenario 1: You did not sell (Old Cost Basis)

You held your original positions and became a Resident.

5 years later, your portfolio has grown to $2,000,000.

Since you are now a full Resident, the entire gain from your original purchase price ($200k) is taxable in India.

| Amount | Note | |

|---|---|---|

| Sale Value (A) | $2,000,000 | Future value of the portfolio. |

| Original Cost Basis (B) | $200,000 | The price you originally paid (or vest price). |

| Total Capital Gain (A-B) | $1,800,000 | Profit liable for tax in India. |

| LTCG Tax @ 12.5% | $225,000 | Base tax on the gain. |

| Surcharge @ 15% | $33,750 | Calculated on the base tax amount. |

| Health & Cess @ 4% | $10,350 | Calculated on (Tax + Surcharge). |

| Total Tax Payable | $269,100 | Effective Rate: ~14.95% |

Scenario 2: You sold while RNOR (New Cost Basis)

You executed a "Tax Reset" by selling your holdings while you were an RNOR and immediately repurchasing them.

This resets your cost of acquisition to $1,000,000 (the current market value) from the original $200,000.

5 years later, when the portfolio reaches $2,000,000, your taxable gain starts from the higher "reset" price.

| Amount | Note | |

|---|---|---|

| Sale Value (A) | $2,000,000 | Future value of the portfolio. |

| New Cost Basis (B) | $1,000,000 | Reset value during your RNOR window. |

| Taxable Capital Gain (A-B) | $1,000,000 | Gain calculated only from the reset point. |

| LTCG Tax @ 12.5% | $125,000 | Base tax on the reduced gain. |

| Surcharge @ 15% | $18,750 | Calculated on the base tax amount. |

| Health & Cess @ 4% | $5,750 | Calculated on (Tax + Surcharge). |

| Total Tax Payable | $149,500 | Effective Rate: ~14.95% |

By resetting your cost basis during the RNOR period, you pay $119,600 less in taxes when you eventually exit your positions.

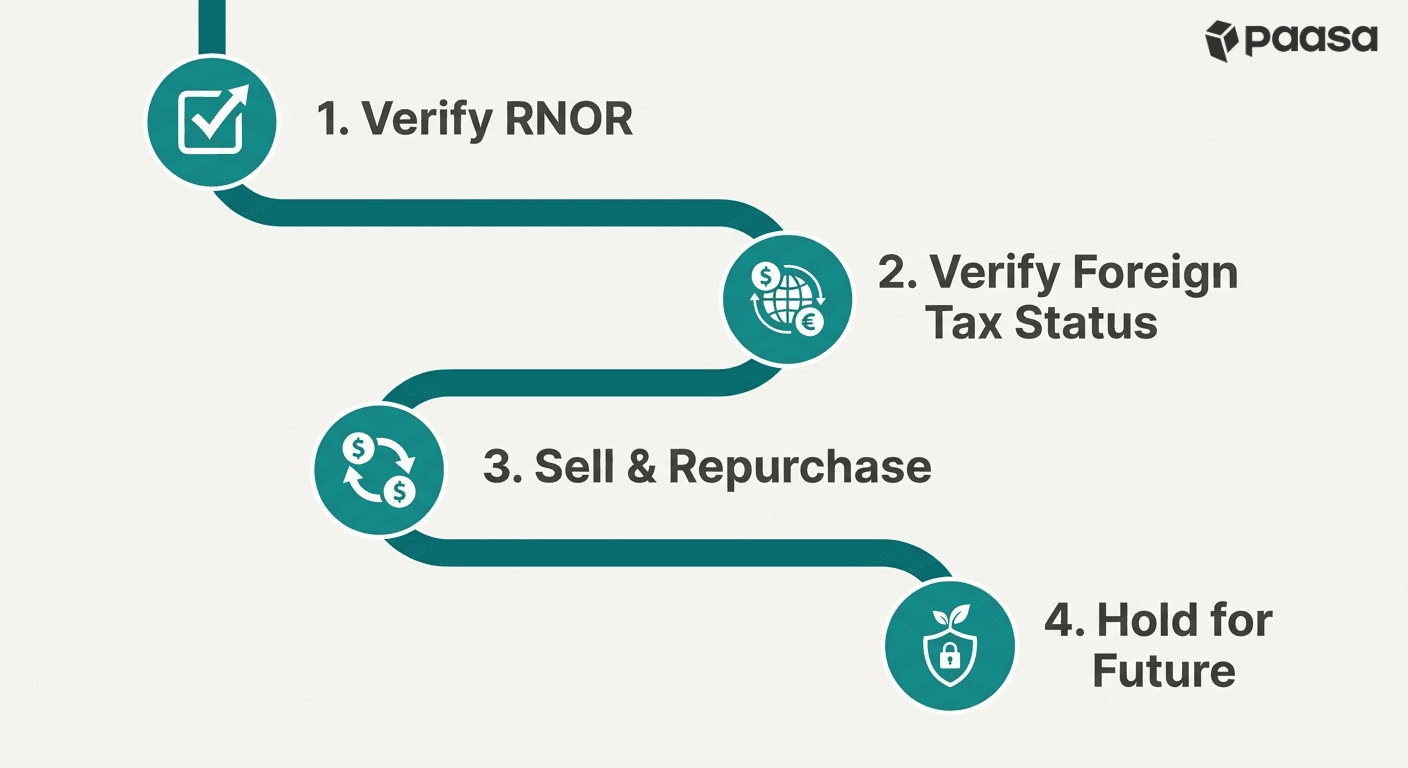

Step-by-Step guide to restructuring your equity while RNOR

To execute this "Cost Basis Reset" correctly, follow this 4-step checklist.

1. Check if you are an RNOR

You cannot use this strategy if you are already an Ordinary Resident (ROR).

- Were you an NRI in 9 out of the last 10 financial years? Or was your stay in India ≤ 729 days in the last 7 years?

- Confirm your status for the current financial year.

2. Check if you are not a tax resident of any other country

You need to ensure you are not taxed in India (due to RNOR) and not taxed in your previous country (e.g., the US).

- If you are still considered a tax resident of the US (e.g., because you hold a Green Card or pass the Substantial Presence Test for the current year), the US will tax the capital gains you trigger. This defeats the purpose of the reset.

3. Sell your equity and repurchase while RNOR

Once you have confirmed your status, execute the trade.

- Sell your foreign stocks (RSUs, ESPPs, or direct holdings) through your foreign broker.

- Ensure the proceeds are credited to your foreign brokerage account. Income received directly in India is taxable, regardless of your RNOR status.

- Immediately use the funds to repurchase the assets. You can buy back the same stocks (e.g., sell Amazon, buy Amazon) or use this opportunity to diversify into broader ETFs (e.g., S&P 500 or Ireland-domiciled UCITS ETFs).

- Your "Cost Basis" is now reset to the current market price.

4. Hold or sell as planned

When you eventually decide to sell these assets 5, 10, or 20 years later, your capital gains tax will be calculated based on this new, higher purchase price irrespective of where you are residing when you sell.

You have effectively legally erased the tax liability on all the growth that happened before you returned to India.

Can there be a situation where I am RNOR in India but a US tax resident?

Yes. It is possible to be a tax resident of both India and the US at the same time.

This happens because the two countries use completely different metrics and rules to determine if you are a tax resident.

- India determines residency based on your physical presence during the Financial Year (April 1 to March 31). You are a Resident if you meet either of these conditions:

- You are in India for 182 days or more during the year.

- You are in India for 60 days or more during the year AND have spent 365 days or more in India over the preceding 4 years.

- The US uses the Substantial Presence Test, which looks at your presence during the Calendar Year (January 1 to December 31) and includes a look-back period of the previous 2 years. Alternatively, if you hold a Green Card, you are a tax resident regardless of where you live.

Because these rules function independently, you can trigger the residency criteria for both countries simultaneously. If this happens, the "Cost Basis Reset" strategy will not work.

Example

Suppose you lived in the US for 10 years and moved back to India permanently on August 1, 2025.

1. Your Status in the US (Calendar Year 2025)

- The US Substantial Presence Test counts days in the current calendar year.

- You were in the US from Jan 1 to July 31, 2025 (~212 days). Since you exceed the 183-day threshold for the Substantial Presence Test, the US considers you a US Tax Resident for the entire year of 2025.

2. Your Status in India (Financial Year 2025-26)

- India looks at the Financial Year (April 1 to March 31).

- You are in India from Aug 1, 2025 to March 31, 2026 (~243 days). Since you exceed 182 days, you are an Indian Resident.

- Why you are RNOR: Since you were a Non-Resident for the entire 10 years prior to this return, you meet the "9 out of 10" test (having been an NRI in 10 of the last 10 years). This classifies you as RNOR.

If you try to execute the "Cost Basis Reset" by selling your stocks in November 2025, here’s what happens:

From India's perspective, you are an RNOR, so the capital gains are technically tax-free.

However, from the US perspective, you are still a tax resident for the 2025 calendar year because you spent more than 183 days there before moving.

Consequently, the US will tax these capital gains.

What's the solution?

In this scenario, you should simply wait until January 1, 2026.

- From Jan 1, 2026, you will no longer meet the US Substantial Presence Test for that new year (assuming you do not travel back to the US).

- You will still be an RNOR in India (until March 31, 2026).

- Selling in January 2026 ensures you are non-resident in the US and RNOR in India, allowing for a tax-free reset.

About Paasa

Paasa is a global investing platform built specifically for Indian residents and returning NRIs. We provide direct access to over 10 global exchanges, including the United States, United Kingdom, Switzerland, Hong Kong, Germany, France, Canada, Netherlands, Japan, and Singapore and support 9 global currencies.

- Seamless "In-Kind" Transfers (ACATS): You can move your entire US stock portfolio (from brokers like Robinhood, Schwab, Fidelity, E*TRADE, and more) directly to Paasa. This allows you to consolidate your assets in one place without triggering a tax event.

- Compliance Support: Paasa provides the exact reports you need for your Indian tax returns and foreign asset disclosures, eliminating the need for manual calculations.

- Estate Tax Protection: Paasa offers access to Ireland-domiciled (UCITS) ETFs, allowing you to legally shield your long-term investments from the 40% US Estate Tax that applies to non-residents.