RSUs are one of the most valuable parts of your compensation, but they are also one of the most confusing when it comes to taxes.

This guide explains how RSUs are taxed from the day they are granted to the day you eventually sell them.

By understanding what happens at each stage, you'll know why tax is withheld, when capital gains tax applies, and how to avoid common mistakes.

Table of contents

- What are RSUs?

- What happens at Grant?

- What Happens at Vesting?

- What Happens After Vesting?

- What Happens When You Sell?

- Cost Basis & Capital Gains

- How Paasa Helps

What Are RSUs?

Restricted Stock Units (RSUs) are a form of equity compensation that employers grant to employees. Instead of receiving shares immediately, you're promised company shares that will be delivered once certain conditions, usually continued employment over a specified period, are met.

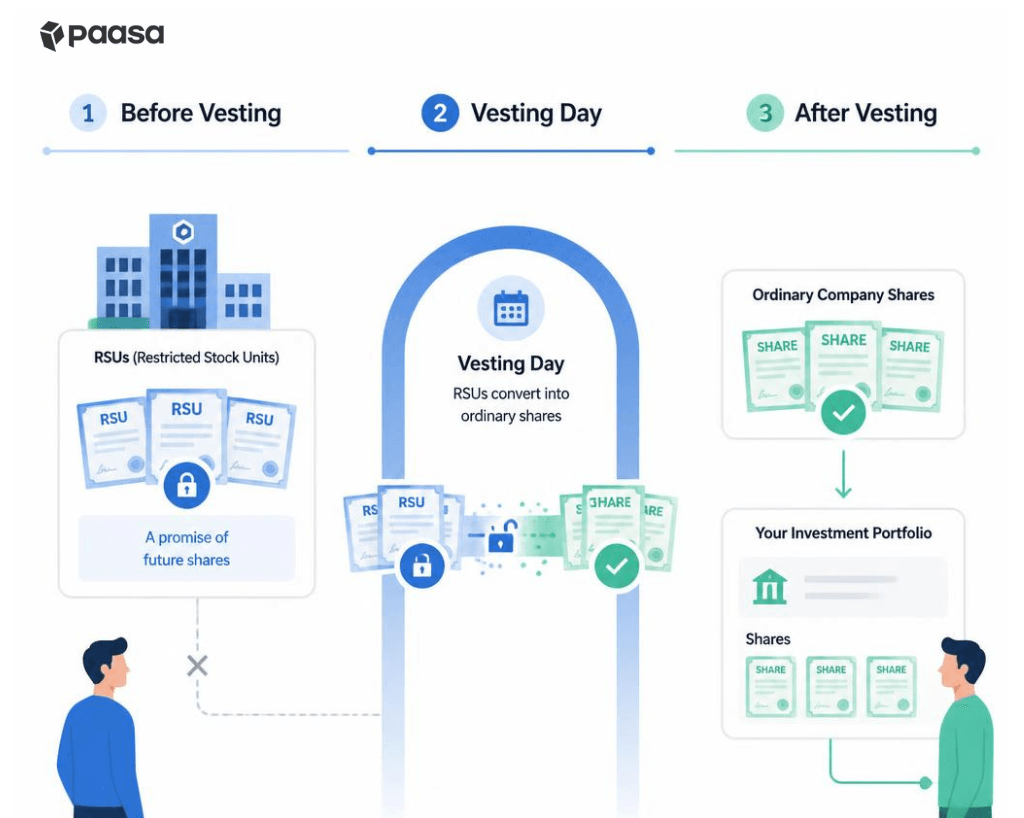

There are four key stages in an RSU's lifecycle:

- Grant: Your employer promises to award you RSUs in the future.

- Vesting: The RSUs convert into company shares and become yours.

- Holding: You can choose to keep the vested shares.

- Sale: You sell the shares, which may result in a capital gain or loss.

What Happens at Grant?

The grant date is when your employer promises to award you a certain number of RSUs. At this stage, you do not own the shares, and they have not yet been transferred to you.

Since you haven't received any shares or economic benefit yet, the grant itself is not a taxable event. There is no income tax to pay, and you don't need to report anything in your tax return simply because your RSUs were granted.

What Happens at Vesting?

Vesting is when your RSUs convert into shares and become yours.

This is the first taxable event. The fair market value (FMV) of the shares on the vesting date is treated as employment income and taxed like salary.

You owe tax even if you don't sell the shares. The tax is based on their value at vesting.

To cover this, employers apply tax withholding by selling some shares or withholding their value.

How Tax Withholding Works

Since tax is due when your RSUs vest, your employer must withhold tax on your behalf. Most employers do this automatically at vesting rather than asking you to pay separately.

The most common method is sell-to-cover, where enough shares are sold to cover the estimated tax. Some employers may instead withhold shares or collect the tax in cash.

Example:

You are an Indian software professional at Microsoft in the 30% income-tax slab (income between 1cr - 2cr). On a vesting date, RSUs worth approximately ₹42,50,000 become taxable as perquisites.

| Amount | Note | |

|---|---|---|

| RSU market value at vesting (A) | 42,50,000 | |

| Employer withholding rate | 30% | |

| Tax withheld (sell-to-cover) (B) | 12,75,000 | 0.30 × 42,50,000 |

| Net value of shares delivered (after tax sale) (A-B) (C) | 29,75,000 | 42,50,000 − 12,75,000 |

The value of your vested RSUs and the tax withheld by your employer are reflected in your Form 16.

To understand where these amounts appear and how to verify them, read our article: How to Read Your Form 16 When You Have RSUs.

Keep in mind that withholding is only an estimate. Your actual tax depends on your total income and tax bracket, so you may still owe additional tax or receive a refund when you file your return.

Tax withholding at vesting doesn't always cover your entire tax liability. Read our Guide to Advance Tax for RSU Holders.

What Happens After Vesting?

Once your RSUs vest, they become regular company shares. From this point on, you can choose to hold them for as long as you like or sell them whenever you're eligible to trade.

Simply holding the shares does not create any additional tax liability. The next taxable event occurs only when you sell the shares.

Any change in the share price after vesting is no longer treated as salary income. Instead, it is considered when calculating your capital gain or loss at the time of sale.

What Happens If You Receive Dividends?

After vesting, if you continue holding the shares, you may receive dividends on those shares. Dividend payouts are a separate taxable event, different from the tax you paid at vesting and the capital gains tax you may pay when you sell.

These dividends are taxed in the year they are received.

For a detailed breakdown of how dividend income is taxed for Indian investors, read our guide on How Foreign Dividend Income is Taxed for Indian Investors.

What Happens When You Sell?

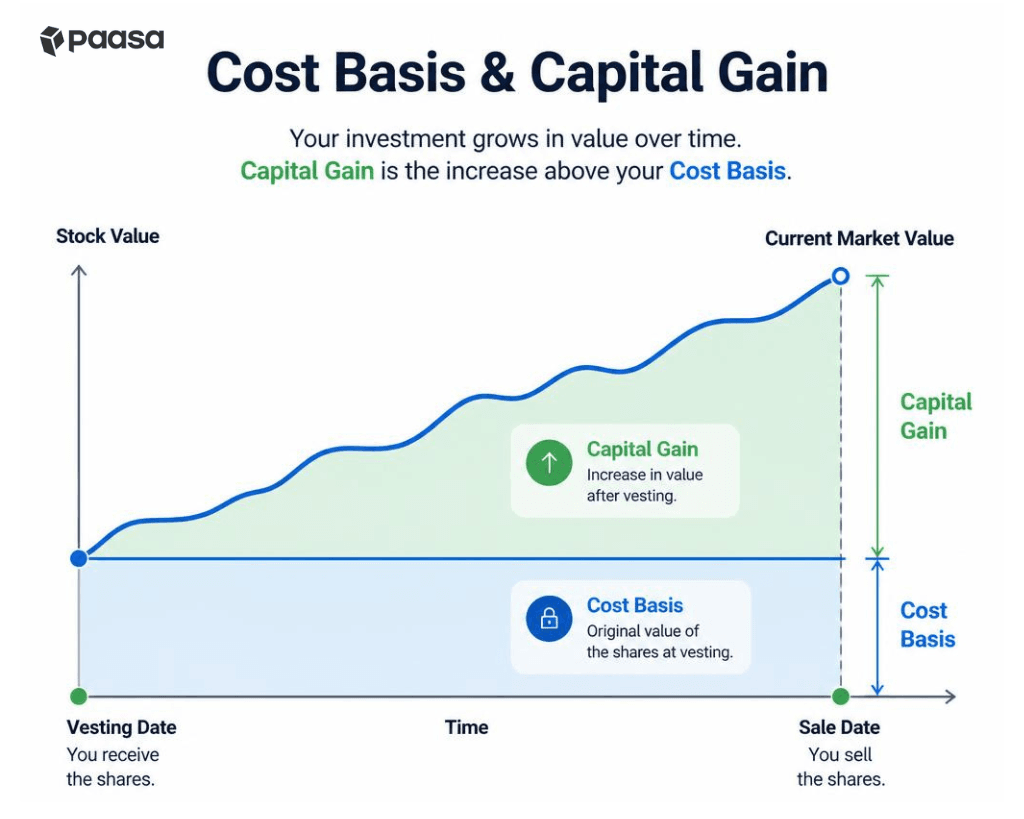

Selling your vested RSUs is the second taxable event. Unlike vesting (taxed as salary), any price change after vesting is treated as a capital gain or loss.

What is the Cost Basis (Cost of Acquisition)?

Your cost basis (also called the cost of acquisition) for RSU shares is the fair market value (FMV) of the shares on the vesting date, before any tax withholding is applied. This is because the entire value of the vested shares is treated as salary income at vesting, even if some shares are sold or withheld to pay taxes.

For example, suppose 100 RSUs vest at an FMV of $100 per share on 16 October 2025. The SBI TTBR on the vesting date is ₹88/USD.

The total fair market value (FMV) of your vested shares is ₹8,80,000.

Your employer may withhold or sell a portion of your vested shares to cover the tax liability. The number of shares withheld depends on your applicable income tax slab, along with any surcharge and cess. For example, if 30 out of 100 shares are withheld for taxes, you will receive the remaining 70 shares.

However, this does not reduce your cost of acquisition. Your cost of acquisition remains ₹8,80,000, based on the FMV of all 100 vested shares before tax withholding. The withheld shares are simply used to meet your tax liability.

When you later sell your RSU shares, you pay capital gains tax only on the change in value after the vesting date, since the FMV on the vesting date has already been taxed as salary income.

Capital Gain (or Loss) = Sale Price − Cost Basis (Cost of Acquisition)

- If you sell the shares for more than the FMV on the vesting date, the difference is a capital gain, which is taxable.

- If you sell the shares for less than the FMV on the vesting date, you incur a capital loss. In that case, no capital gains tax is payable on that sale, and the loss may generally be used to offset capital gains, subject to the applicable tax rules.

Foreign shares, including RSUs of overseas companies, are treated as unlisted equity shares/securities for Indian tax purposes. The rate of capital gains tax is based on the holding period:

| Holding period from vest date | Classification | Tax rate |

|---|---|---|

| Up to 24 months | Short-term capital gains (STCG) | At your income slab rate |

| More than 24 months | Long-term capital gains (LTCG) | 12.5%, without indexation |

Read our Capital Gains Tax on RSU Shares guide for a detailed explanation of calculating capital gains, holding periods, and tax rates.

What Happens If You Leave Before Vesting?

In most cases, if you leave your employer before your RSUs vest, any unvested RSUs are forfeited. Since the shares never become yours, you don't owe any tax on them.

If your RSUs have already vested before you leave, leaving your employer has no impact on their tax treatment. The shares are yours, and you can continue to hold or sell them like any other investment.

Some companies have special provisions that allow RSUs to vest after retirement or accelerate vesting following events such as an acquisition or change in control. In these cases, the shares are taxed when they vest.

How Paasa Helps

Paasa helps Indian investors manage global investments with confidence. Whether you're building wealth through RSUs or investing across international markets, Paasa brings your portfolio and tax reporting together in one place.

For RSU holders, Paasa offers:

- Diversify your RSU wealth across global markets while maintaining USD exposure

- End-of-year tax reports covering capital gains, dividends, and Schedule FA in INR

- Accurate reporting using the prescribed SBI TT Buying Rates

- Optional expert guidance on taxation, FEMA, LRS, and other compliance matters

If you have questions about managing your RSUs or global investments, our team is here to help.