If you are an Indian software professional working for a US company such as Microsoft, Google, or Amazon, a major part of your wealth is probably tied up in the form of RSUs.

You will eventually want to sell these RSUs either partially or fully for various reasons like diversification, funding a major purchase, etc.

But exactly how and when you sell your vested shares can have a significant impact on the total processes, or the net returns that you get.

This article provides a simple framework that you can follow to minimize your tax liabilities and get the most out of your RSU wealth.

Table of Contents

- How RSUs Are Taxed

- The RSU Selling Framework

- Why Employees Sell Their RSUs

- US Estate Tax Considerations for Indian Investors

- How Paasa Helps

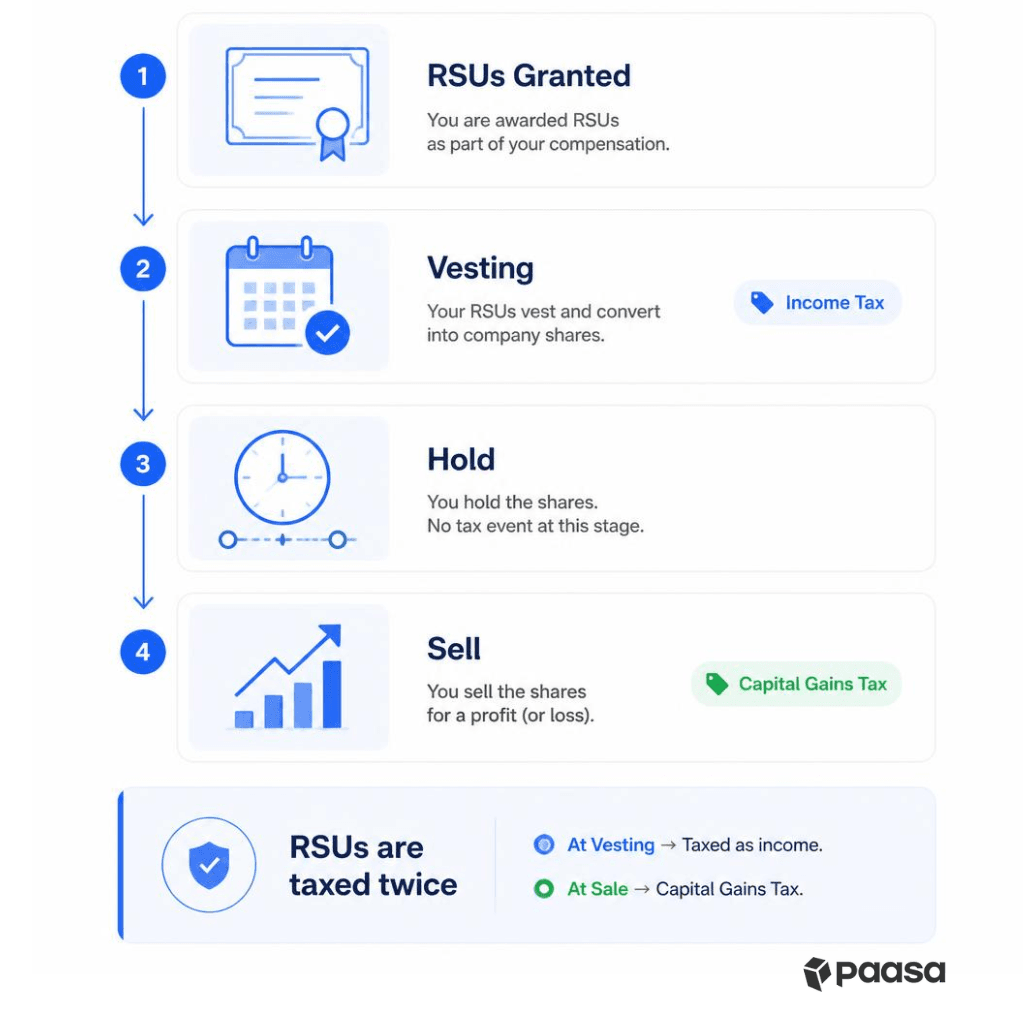

How RSUs Are Taxed

RSUs are taxed in two ways, once at vesting and once when you sell.

When RSUs vest, they are taxed as income. The fair market value is added to your income and is taxed at the applicable income tax rate.

Once your RSUs have vested, they are treated as normal foreign shares and taxed accordingly at sale. If they distribute dividends when you hold them, dividends are taxed as foreign dividends (according to the rules laid out in the US-India DTAA for US shares).

Tax at Vesting

When RSUs vest, the fair market value of the shares is treated as your employment income.

Employers typically withhold taxes before the shares are delivered, which is why the number of shares received is often lower than the number that vested.

Importantly, this tax applies even if they do not sell the shares.

Capital Gains Tax After Vesting

Once your RSUs vest and the shares land in your brokerage account, they are treated exactly like any other foreign-listed stock for capital gains purposes.

The capital gain or loss is calculated as: Sale Price - Fair Market Value at Vesting

If the stock appreciates after vesting, you owe capital gains tax when you sell.

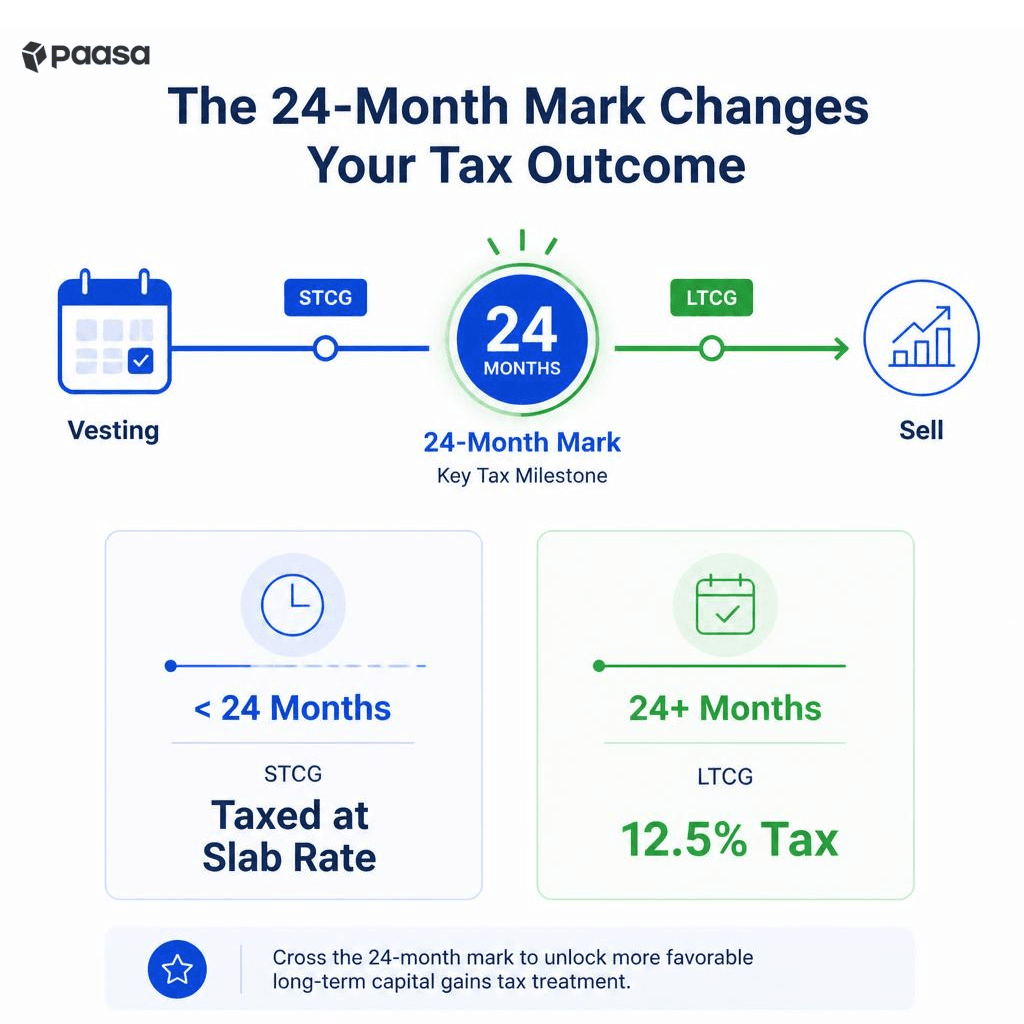

The rate of tax is decided based on your holding period.

| Holding period from vest date | Classification | Tax rate |

|---|---|---|

| Up to 24 months | Short-term capital gains (STCG) | At your income slab rate |

| More than 24 months | Long-term capital gains (LTCG) | 12.5%, without indexation |

For RSU shares, the date of acquisition is the vest date.

To learn more, read our detailed guide on Capital Gains Tax on RSU Shares.

The RSU Selling Framework

The right approach depends on factors such as concentration risk, tax considerations, liquidity needs, and conviction in the company.

The following approaches illustrate some of the most common ways to manage vested RSUs, along with the risks associated with each.

1. Same-Day Sale

If a large part of your wealth is tied up in RSUs and you have decided to diversify, selling right after the shares vest is the most effective way.

Since you have not made any capital gains yet, you will not have to pay any capital gains tax on the sale proceeds.

Once you sell them, you are free to invest the money elsewhere.

Risk: You will still have to report a miniscule capital gain when you file your tax returns as the selling price will be slightly higher or lower than your acquisition cost due to normal price movements.

2. Hold for Long-Term Capital Gains

If you have decided to hold your company shares for now, holding them till they qualify for long term capital gains (LTCG) classification is the best approach.

In India, foreign shares held for more than 24 months qualify for the 12.5% long-term capital gains tax rate. If you sell them before 24 months, your gains will be classified as short term capital gains (STCG) and taxed at your income tax slab rate.

Example

Here's how much difference the short term and long term classification can make in your net returns.

Suppose 100 Microsoft shares vest on April 1, 2024, at $400 per share.

The SBI TTBR on the last day of the preceding month was ₹83.00 and therefore your total acquisition cost was 100x400x83 = ₹33,20,000

We are assuming that the selling price and applicable SBI TTBR rate was the same at both dates for ease of calculation.

Suppose the stock price was $480 on both selling dates and the SBI TTR was ₹90.00.

Therefore your total sale proceeds and resulting capital gains was:

| Amount | Note | |

|---|---|---|

| Cost of acquisition (A) | ₹33,20,000 | 100 shares × $400 × ₹83.00, vest-day FMV already taxed as salary |

| Total sale proceeds | $48,000 | 100 shares × $480 |

| SBI TTBR | ₹90.0 per dollar | |

| Sale proceeds in INR (B) | ₹43,20,000 | $48,000 × ₹90.0 |

| Capital gain (B - A) | ₹10,00,000 | ₹43,20,000 − ₹33,20,000 |

Here's how your tax liability will look if you sell at 23 months and at 25 months:

Selling at 23 months

| Holding period | 23 months | April 1, 2024 to March 1, 2026 |

| Classification | STCG | Under 24 months |

| Tax at 30% | ₹3,00,000 | Applicable slab rate |

| Surcharge at 10% | ₹30,000 | Applicable if total income is ₹50L–₹1Cr |

| Health and education cess at 4% | ₹13,200 | On tax + surcharge |

| Total tax | ₹3,43,200 |

Selling at 25 months

| Holding period | 25 months | April 1, 2024 to May 1, 2026 |

| Classification | LTCG | Over 24 months |

| Tax at 12.5% rate | ₹1,25,000 | Applicable LTCG rate |

| Surcharge at 10% | ₹12,500 | Applicable if total income is ₹50L–₹1Cr |

| Health and education cess at 4% | ₹5,500 | On tax + surcharge |

| Total tax | ₹1,43,000 |

Holding the shares for more than 24 months reduced the tax liability from ₹3,43,200 (STCG) to ₹1,43,000 (LTCG), resulting in a tax saving of ₹2,00,200.

A longer holding period can substantially improve after-tax returns on vested RSUs.

3. Tax-Loss Harvesting

If your shares are trading below their vesting value, selling them generates a capital loss that can offset other capital gains, subject to applicable tax rules.

You can use this approach as part of a broader tax-planning strategy to lower your overall tax liability and offset some of the loss.

Risk: The loss becomes permanent once realized, and you will not benefit from any upside in the stock price. Decide based on your conviction and future outlook for the stock.

Why Employees Sell Their RSUs

For many Indian professionals working at companies like Apple, Microsoft, Amazon, Google, and Nvidia, RSUs make up a significant portion of their total compensation. Over the years, as more RSUs vest and the stock appreciates, a large part of your wealth can become concentrated in your employer's stock.

This creates concentration risk, where a single company or sector can heavily influence your portfolio. Even if you hold RSUs from multiple tech companies, you're still exposed to the same sector risk.

A diversified portfolio reduces this risk by spreading your investments across many companies, so the impact of any single stock on your overall returns is limited.

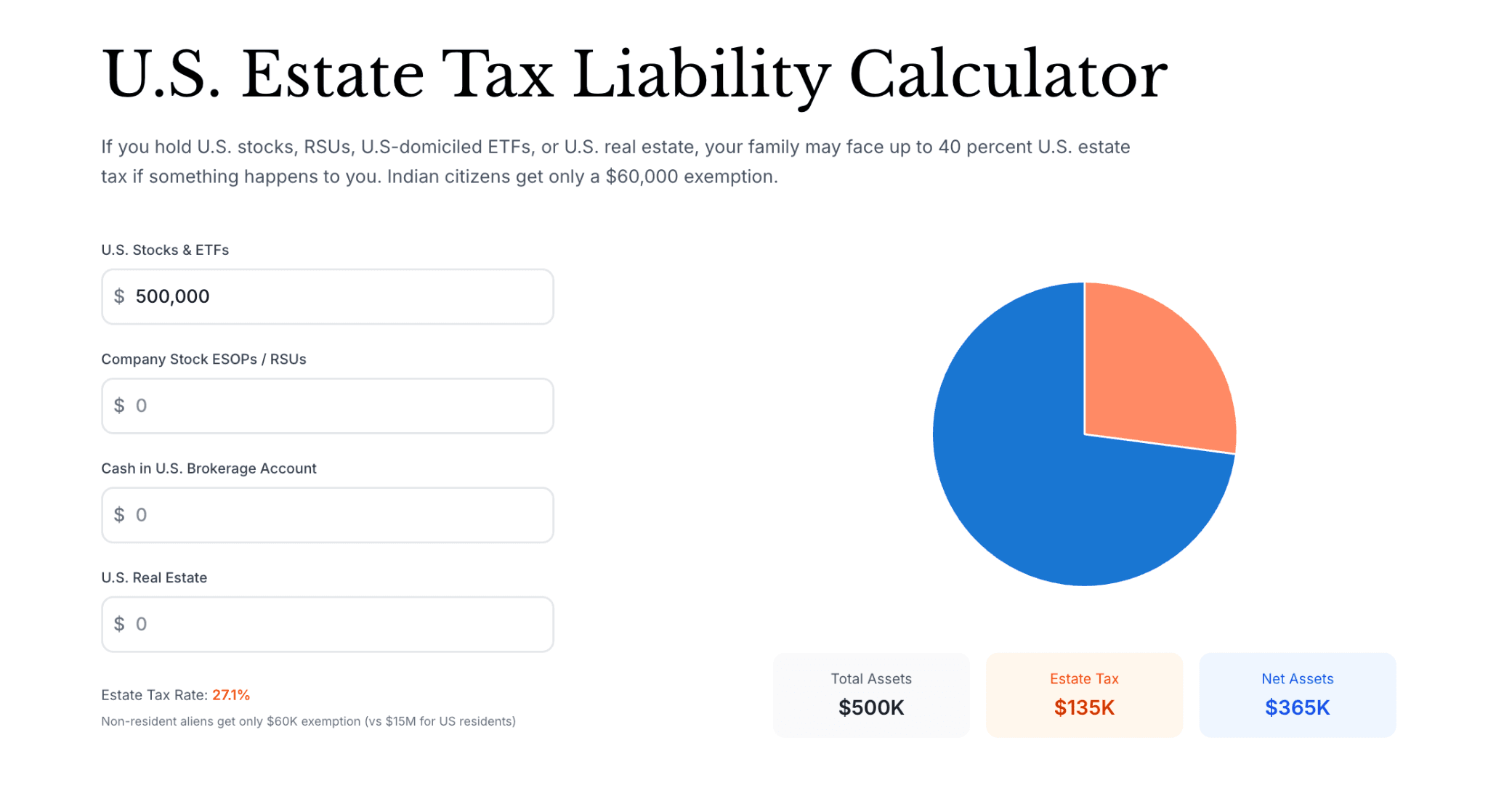

Another major reason Indian professionals sell their RSUs is the US Estate Tax.

US Estate Tax Considerations for Indian Investors

If you choose to hold vested RSUs for the long term, US estate tax is another factor to consider. Unlike capital gains tax, which applies when shares are sold, US estate tax applies to US-listed shares held at the time of death.

For Indian residents, US-listed shares are subject to US estate tax. Non-US residents receive an exemption of only $60,000, and amounts above this threshold are taxed at rates of up to 40%.

As a result, investors with significant holdings in US-listed shares should factor estate tax exposure into their long-term financial and succession planning.

For example, if you are an Indian resident who holds US-listed shares worth $500,000 at the time of death, the total Estate Tax liability upon your death will be $135K.

Use our Estate Tax Calculator to find your exact liability.

To learn about the US Estate Tax and how to protect your wealth from it, read our detailed guide on US Estate Tax for Indians.

How Paasa Helps

Paasa helps Indian investors and RSU holders access global markets with ease, enabling investments across the US, Europe, China, Japan, and other major economies.

Trusted by HNIs, family offices, and institutions, Paasa combines international investing opportunities with India-focused support and compliance.

Paasa helps you hold and protect your RSU wealth with:

- In-kind transfer from your existing brokerage account

- Access to US, Europe, China, Japan, and other major economies

- Access to UCITS ETFs that protect against the US estate tax risk

- Comprehensive tax reporting tailored for Indian investors, including capital gains, dividend taxation, and TCS tracking.