NRIs living in the US, UK, or Singapore and planning to move back to India often find it difficult to navigate tax regulations and other investment related changes during the transition.

As a result, they often find themselves in situations where they have unknowingly violated Indian regulation or are stuck with a foreign broker who has frozen their investment account.

This is your consolidated guide to avoiding all those problems and actually taking advantage of the transition period to maximize your long term returns and financial security.

Table of contents

- RNOR status check

- Foreign investments

- Bank accounts

- Additional compliance requirements

- Returning from the USA

- Returning from the UK

- Returning from Singapore

- Returning from Australia

Moving back to India

Here are the things you need to keep in mind while moving back to India. You can use these to optimize your investments and structure them properly, and you can also treat this as a quick checklist to ensure you are not missing anything.

Check if you are eligible for "RNOR" Status

RNOR (Resident but Not Ordinarily Resident) is a transitional tax residency status for returning NRIs. It functions as a bridge between being a Non-Resident and becoming a full Ordinary Resident.

You qualify for this status if you meet one of the following criteria:

- You have been an NRI for 9 out of the last 10 financial years.

- You have lived in India for 729 days or less in the preceding 7 financial years.

- If you are an Indian Citizen or Person of Indian Origin (PIO) with Indian income exceeding ₹15 Lakhs, you become an RNOR if you stay in India for 120 to 181 days (instead of the usual 182).

- If you are an Indian Citizen with Indian income exceeding ₹15 Lakhs and you are not liable to tax in any other country, you are automatically treated as a "Deemed Resident" in India. Deemed Residents are always classified as RNORs.

This status grants you a 1 to 3-year window where your foreign income is NOT taxable in India, provided it is received outside India first. This allows you to manage your international assets without immediate tax liability in India.

- If you sell your overseas stocks and ETFs while you are RNOR, the capital gains are tax-free in India. You only pay applicable overseas taxes as a non-resident (often 0% on gains for non-residents). This allows you to reset your cost basis without paying any taxes.

Example

Suppose you are a software professional who has lived and worked in the US for the past 12 years. You recently moved back to India.

As you have been an NRI for the last 10 financial years, you qualify as Resident but Not Ordinarily Resident (RNOR).

You hold US stocks worth $700,000, and the total acquisition cost was $350,000.

Scenario 1: You did not sell (Old Cost Basis)

You held your original positions and became a Resident.

7 years later, your portfolio has grown to $1,500,000.

Since you are now a full Resident, the entire gain from your original purchase price is taxable in India.

| Amount | Note | |

|---|---|---|

| Sale Value (A) | $1,500,000 | Future value of the portfolio. |

| Original Cost Basis (B) | $350,000 | The price you originally paid in the US. |

| Total Capital Gain (A-B) | $1,150,000 | Profit liable for tax in India. |

| LTCG Tax @ 12.5% | $143,750 | Base tax on the gain. |

| Surcharge @ 15% | $21,563 | Calculated on the base tax amount. |

| Health & Cess @ 4% | $6,612 | Calculated on (Tax + Surcharge). |

| Total Tax Payable | $171,925 | Effective Rate: 14.95% |

Scenario 2: You sold while RNOR (New Cost Basis)

You executed a "Tax Reset" by selling your holdings while you were an RNOR and immediately repurchasing ETFs and stocks.

This resets your cost of acquisition to $750,000 from the original $350,000.

7 years later, when the portfolio reaches $1,500,000, your taxable gain starts from the higher "reset" price.

| Amount | Note | |

|---|---|---|

| Sale Value (A) | $1,500,000 | Future value of the portfolio. |

| New Cost Basis (B) | $700,000 | Reset value during your RNOR window. |

| Taxable Capital Gain (A-B) | $800,000 | Gain calculated only from the reset point. |

| LTCG Tax @ 12.5% | $100,000 | Base tax on the reduced gain. |

| Surcharge @ 15% | $15,000 | Calculated on the base tax amount. |

| Health & Cess @ 4% | $4,600 | Calculated on (Tax + Surcharge). |

| Total Tax Payable | $119,600 | Effective Rate: 14.95% |

By resetting your cost basis during the RNOR period, you pay $52,325 less in taxes when you eventually exit your positions.

What happens to my foreign investments?

You are legally allowed to indefinitely hold foreign assets (stocks, ETFs, property) that you acquired while you were an NRI. Under FEMA regulations, you do not have to sell them just because you moved back to India.

However, while Indian law allows you to keep them, your foreign broker might not.

Most brokerage firms in the US, UK, Europe, and Singapore are designed to serve residents of those specific countries. When you move back to India, your tax residency changes, and many platforms are not equipped to handle "Non-Resident" accounts compliant with Indian laws.

Here is how different platforms typically handle the move:

- Strict Restrictions (New Platforms): Popular fintech apps (like Robinhood/Webull in the US, or certain neobrokers in the UK/EU) often do not support non-residents. If they detect a foreign IP address or if you update your address to India, they may restrict your account access or force you to liquidate your positions immediately, triggering a tax bill.

- Limited Access (Traditional Brokers): Large traditional brokers (like Schwab, Fidelity, or Interactive Brokers) are generally more flexible and may allow you to convert to an "International" account. However, you will likely face operational hurdles:

- You may lose access to specific local mutual funds or ETFs.

- Dividend Reinvestment Plans (DRIP) are often disabled.

- You are left to manage complex tax reporting (like Schedule FA) manually, as these brokers do not generate reports for the Indian financial year.

What is the best way to stay invested globally?

The most effective strategy is to consolidate your holdings by transferring your investments to a platform specifically built for global investing from India, like Paasa.

These platforms are designed to bridge the gap:

- Seamless Operation: They allow you to maintain your positions and trade as usual from India.

- Compliance Ready: They handle India-specific requirements, such as filing Form W-8BEN (to reduce tax on US dividends) and generating reports tailored for Schedule FA filings in India.

💡 Pro-Tip: Transfer, Don't Sell

Do not sell your stocks just to move them. Selling triggers a "taxable event," meaning you have to pay capital gains tax immediately.

Instead, use an "In-Kind" Transfer (such as ACATS for US stocks). This allows you to move your entire portfolio "as is" to an India-friendly platform like Paasa without selling a single share, preserving your wealth and avoiding unnecessary taxes.

To learn more about how you can do in-kind transfers from different platforms to Paasa, read:

- How to transfer from Robinhood?

- How to transfer from Morgan Stanley?

- How to transfer from Fidelity?

- How to transfer from E-Trade?

- How to transfer from EquatePlus?

What happens to my bank accounts?

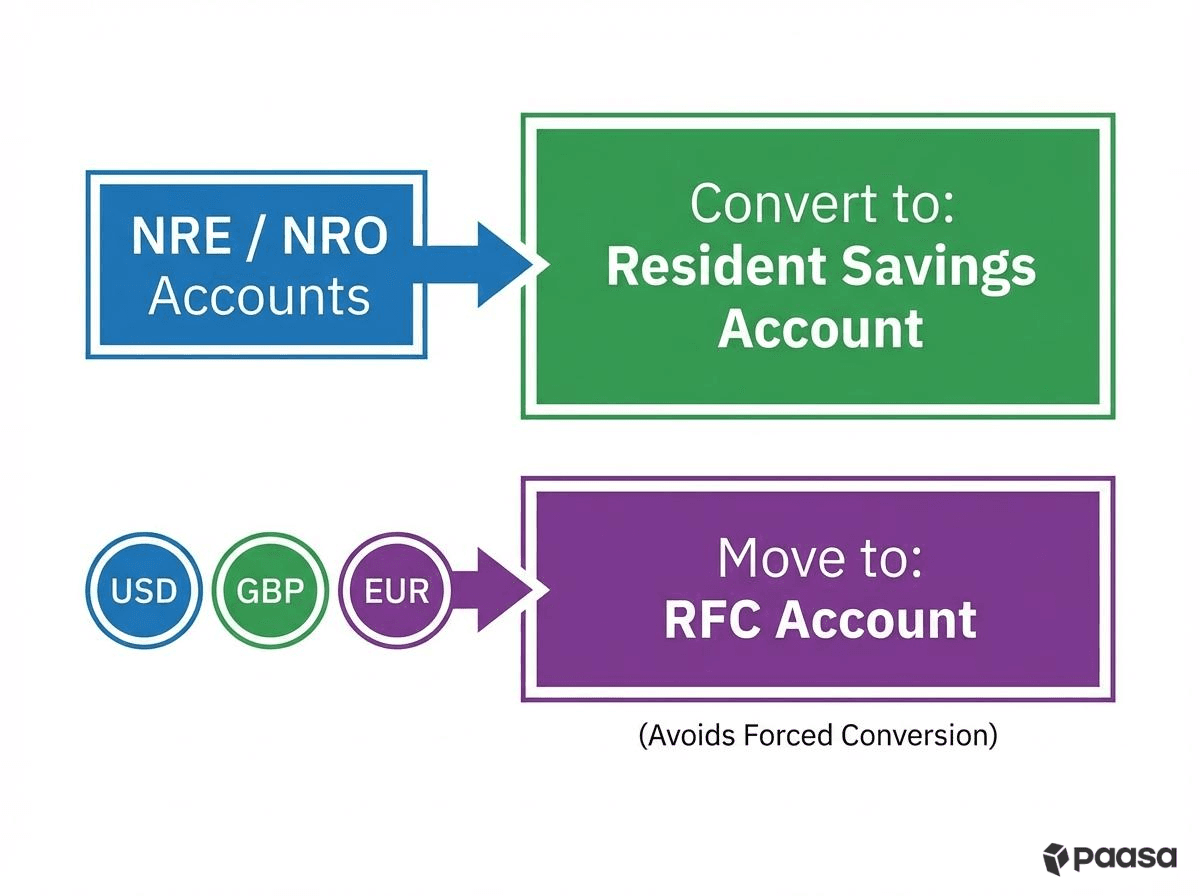

- You need to convert your NRE/NRO to Resident Savings Account You must notify your bank of your return. Your NRE and NRO accounts will be converted into a standard Resident Savings Account.

- You should open a RFC Account: If you bring your USD/GBP back to a normal savings account, it gets forcibly converted to Rupees. If the Rupee strengthens or you need to move abroad again, you lose money on conversion fees. An RFC account lets you hold your balance in foreign currency (USD, GBP, EUR) even while living in India. It protects you from currency risk and is fully repatriable.

What additional compliance requirement am I subject to?

Once you become a full resident (ROR), you must declare all foreign assets (bank accounts, RSUs, stocks) in the Schedule FA (Foreign Assets) section of your Indian Income Tax Return. Failure to report even if you earned zero income from the asset carries the risk of further scrutiny, penalties, and prosecution.

To learn more about how your global income is taxed in India and the reporting requirements, read:

- How global stocks and ETFs are taxed?

- How repatriate foreign income is taxed?

- What are the foreign asset disclosure requirements?

Important things you need to remember when Returning from the USA

401(k) / IRA

You can either withdraw your 401k (and pay a 10% penalty plus taxes) or keep it as is when moving back to India. If you continue to hold your 401k or IRA, manage the investments within it, and eventually withdraw from it in retirement, even if you never return to the US. However, once you leave your job, you generally cannot make new contributions to that specific plan. Your account essentially goes into "maintenance mode" the funds stay invested and continue to grow tax-deferred.

Tax Filing

In the year you move, you may need to file a "Dual-Status" tax return, which is more complex than a standard 1040.

Please consult your tax advisory for professional guidance on whether you need to file a dual status return and how to do it.

Important things you need to remember when Returning from the UK

ISA (Individual Savings Account)

ISAs are tax-free only for UK residents. The moment you become an Indian resident, the tax shield vanishes. All dividends and gains inside your ISA become fully taxable in India. You can liquidate your ISA or reset the cost basis (sell and rebuy) while you are still an RNOR to save on future capital gains tax.

- Pension (SIPP/Workplace)

- Transferring this to India (QROPS) is often difficult and triggers a high tax charge (up to 25%). It is usually financially better to leave the pension in the UK and draw from it in retirement.

Important things you need to remember when Returning from Singapore

SRS / CPF

CPF withdrawals are tax-free in Singapore. However, if you receive the lump sum after you become a tax resident of India, the entire amount could be taxed as "salary" or "income" in India. Time your exit carefully. Ensure you withdraw your CPF/SRS balance and receive the funds while you are still a non-resident of India (or during your RNOR period) to ensure the withdrawal remains tax-free.

Important things you need to remember when Returning from Australia

Superannuation

You cannot withdraw your Superannuation just because you are leaving, unless you were on a temporary visa. If you are a Permanent Resident or Citizen, your money stays locked in Australia until you reach retirement age (usually 60). Your Super fund continues to be taxed in Australia (15% on earnings). Once you are an Indian resident, you must also report this fund in India. To avoid paying tax twice on the same income, you will need to claim a Foreign Tax Credit in your Indian tax return.

Capital Gains Exit Tax

When you stop being an Australian tax resident, the ATO assumes you sold all your stocks and ETFs on the day you left. This is called "Deemed Disposal." You have two options here:

- Pay Now (reccommended): Pay tax on your "paper profits" in your final Australian tax return. This creates a "clean break." Future growth is not taxed by Australia.

- Defer: You can choose not to pay now. However, this keeps your assets "connected" to Australia. When you finally sell them years later, Australia will tax the entire gain (including growth that happened while you lived in India), and you usually lose the 50% Capital Gains Tax discount.

About Paasa

Paasa is a global investing platform built specifically for Indian residents and returning NRIs. We provide direct access to over 10 global exchanges, including the United States, United Kingdom, Switzerland, Hong Kong, Germany, France, Canada, Netherlands, Japan, and Singapore and support 9 global currencies.

- Seamless "In-Kind" Transfers (ACATS): You can move your entire US stock portfolio (from brokers like Robinhood, Schwab, Fidelity, E*TRADE, and more) directly to Paasa. This allows you to consolidate your assets in one place without triggering a tax event.

- The Compliance Advantage: Paasa provides the exact reports you need for your Indian tax returns and foreign asset disclosures, eliminating the need for manual calculations.

- Estate Tax Protection: Paasa offers access to Ireland-domiciled (UCITS) ETFs, allowing you to legally shield your long-term investments from the 40% US Estate Tax that applies to non-residents.

Disclaimer

This article is intended solely for information and does not constitute investment, tax, or legal advice. Global investments carry risks, including currency risk, political risk, and market volatility. Please seek advice from qualified financial, tax, and legal professionals before acting.