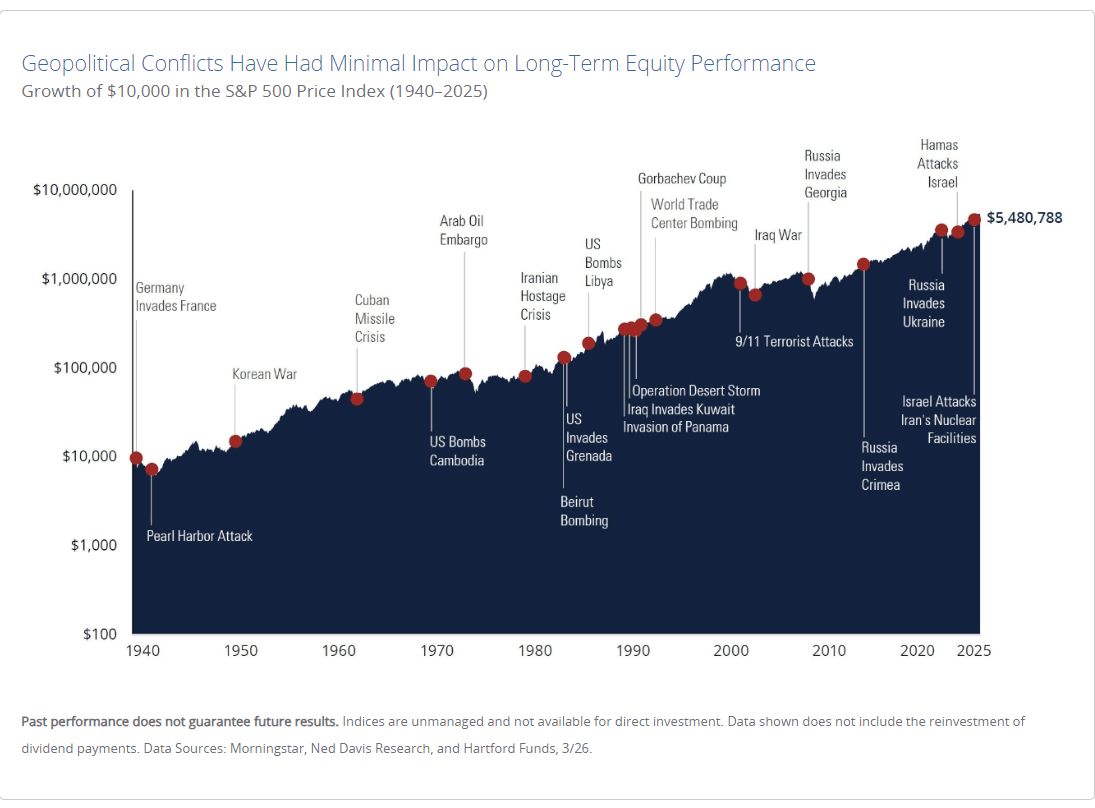

Every time a conflict breaks out, financial headlines run the same playbook: plunging futures, screaming volatility indices, breathless warnings of systemic risk. And every time, the long-term record tells a quieter, different story. Markets have absorbed World War II, Korea, Vietnam, the Gulf War, 9/11, Iraq, Ukraine and across nearly all of them, investors who held their positions came out ahead of those who fled to cash.

This note draws on a century of data to examine why war tends to produce market bottoms rather than prolonged collapses, which asset classes benefit most, and what the mechanism actually is behind a counterintuitive truth that has repeated itself across every generation of investors.

Table of content

What Does Geopolitical Conflict Mean for the Market?

History offers a helpful perspective. While geopolitical shocks create short-term uncertainty, the long-term behavior of markets has been remarkably consistent. Markets react quickly to uncertainty (markets hate uncertainty), but they also tend to recover faster than many expect. Looking at the data across decades of conflict reveals an important lesson for investors. Economic fundamentals influence the markets far more than geopolitical headlines.

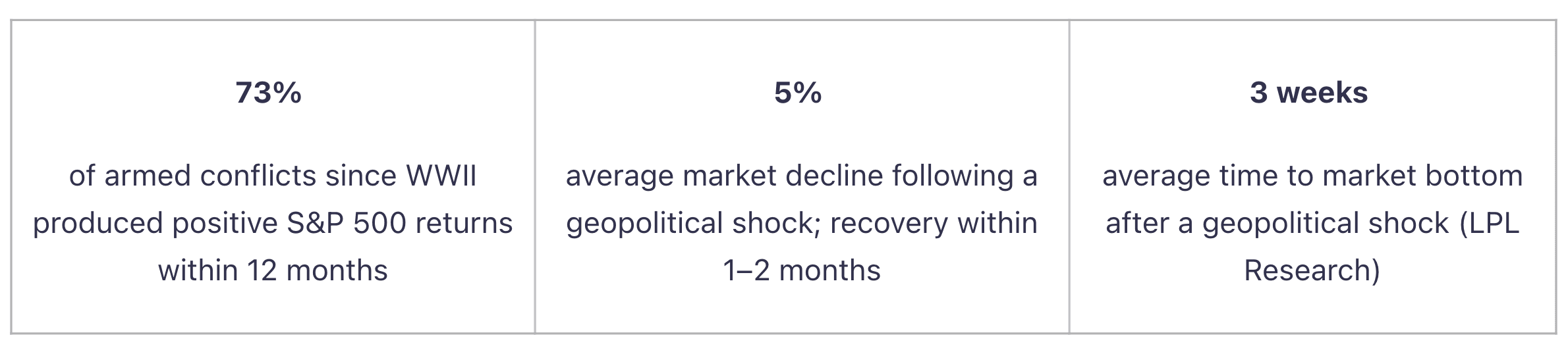

Markets are often higher one year after geopolitical shocks. According to research published by Hartford Funds examining armed conflicts since World War II, the S&P 500 was higher one year after the onset of conflict roughly 70 percent of the time. The average one-year return has historically been in high single digits.

At first glance, it may seem counterintuitive. Major global conflicts dominate headlines and create uncertainty, yet markets often recover quickly or continue moving higher.

The Data War-by-War

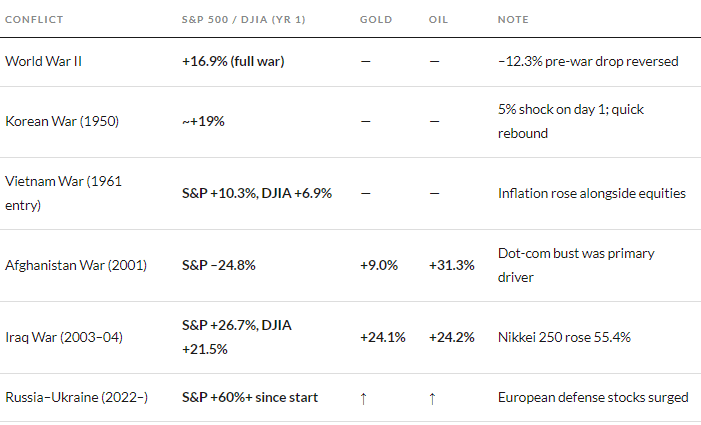

The record is most legible when examined conflict by conflict. The table below covers six major U.S.-involved conflicts and their first-year market outcomes across equities and select commodities. The one notable exception, Afghanistan in 2001, is explained by the dot-com bubble collapse that was already underway, not the conflict itself. Strip out that confounding factor and the pattern is remarkably consistent.

Why Asset Prices Rise

Three structural forces explain why war has historically been additive to asset prices rather than destructive over any meaningful time horizon.

- Fiscal stimulus at scale. Wars force governments to spend. Defense contracts flow to manufacturers; infrastructure investment expands; employment in armaments and logistics rises. This is a Keynesian stimulus compressed into months. Post-9/11, the wars in Iraq and Afghanistan alone channeled an estimated $2–4 trillion to contractors, with one-third to one-half of total Pentagon spending flowing to private firms.

- Lower stock volatility. Counter-intuitively, NBER research covering 100 years of U.S. military spending documented that stock volatility is approximately 25% lower during conflict periods than during peacetime. The reason is that wartime government procurement gives corporations predictable revenue; defense budgets are set years in advance, which narrows earnings-per-share dispersion and makes analyst forecasting more accurate. Uncertainty about profits falls even as geopolitical uncertainty rises.

- Innovation spillover. Wars accelerate R&D in ways that generate civilian returns for decades. GPS, the internet (ARPANET), jet propulsion, radar, and semiconductor miniaturization all trace lineage to military investment. Each dollar of defense R&D historically creates 1.5–2 jobs, many in sectors that eventually become peacetime growth drivers.

Defense & Commodity Sectors: Where the Alpha Lives

While broad equity markets tend to recover and rise, two specific sectors show the most consistent wartime outperformance: defense industrials and commodities (energy and gold).

From the Iraq War's commencement in March 2003, the S&P Aerospace and Defense index nearly tripled over the next four years, easily outstripping the S&P 500's gains. Defense stocks outperformed the S&P 500 for three consecutive years, from 2000, 2001, and 2002, as spending surged following the September 11 attacks.

A peer-reviewed study of 75 global defense companies from 2014 to 2023 found that the Russia–Ukraine war impacted stocks of 81.4% of companies in the sample, with the majority recording significant positive returns. The Crimean annexation in 2014 alone triggered immediate price reactions at 50.6% of tracked defense firms.

Gold and oil tell a complementary story. During the Iraq War's first year, gold rose 24.1% and WTI crude gained 24.2%. These are not coincidental: war disrupts supply chains and elevates geopolitical risk premia, both of which flow directly into commodity prices.

Investor's Takeaway

The evidence across a century points to a straightforward conclusion: selling during war is almost always the wrong decision.

The investors who fled to cash after Pearl Harbor, after 9/11, after the Iraq invasion, after the Ukraine invasion; each time they locked in losses that the market subsequently recovered. Some of the best single trading days in market history have occurred inside bear markets triggered by geopolitical events.

The average one-week decline after an initial geopolitical shock is a mere 1.09%, per Stock Trader's Almanac data covering 17 crises since 1939. Within twelve months, the S&P has historically posted an average gain of 2.92% above that baseline, with the distribution skewed heavily positive when conflicts do not coincide with major macroeconomic contractions.

What this means practically: if war breaks out and your instinct is to sell, history says that instinct is expensive. The better-documented strategy is to hold, consider adding exposure to defense and commodity sectors in the early months of a conflict, and let the market's inherent forward-looking mechanism do its work.