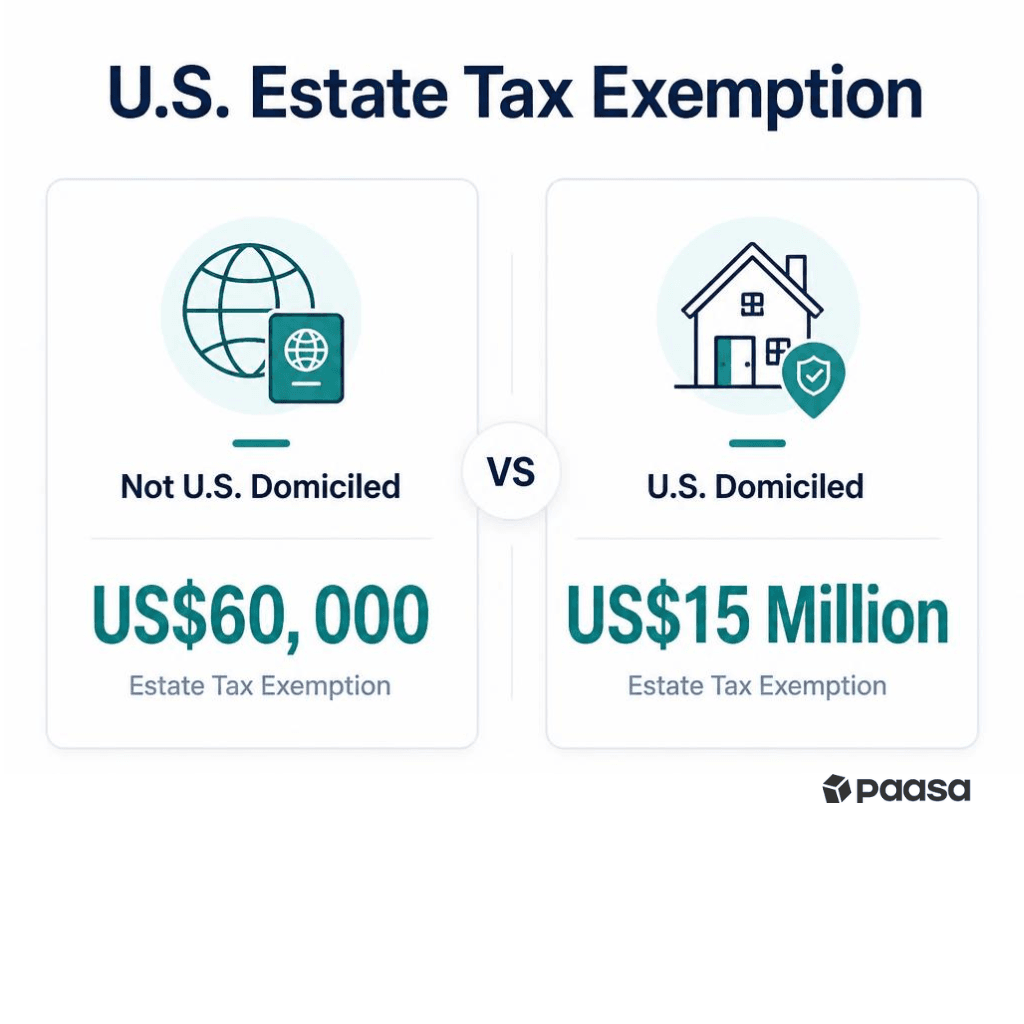

If you are a US tax resident but not a US citizen or green card holder, your US-situs assets are subject to the lower US$60,000 US estate tax exemption, rather than the US$15 million+ exemption available to individuals who are domiciled in the United States.

To reduce this estate tax exposure, many non-US investors choose to invest through non-US-domiciled funds, such as UCITS ETFs, which provide exposure to the US market without being treated as US-situs assets.

However, if you are a US tax resident, investing in UCITS ETFs creates a different tax challenge. Most UCITS ETFs are treated as Passive Foreign Investment Companies (PFICs) for US tax purposes and are therefore subject to the PFIC tax rules.

This article explains how PFIC rules apply to UCITS ETFs, the three PFIC tax regimes, and the key tax considerations if you are living and working in the US on a temporary work visa.

Table of content

- Understanding the US Estate Tax Problem

- Understanding the PFIC Rules for UCITS ETFs

- How PFICs Are Taxed in the US

- Practical Approach for NRIs

- About Paasa

Understanding the US Estate Tax Problem

Being a US taxpayer does not automatically entitle you to the full US estate tax exemption.

Tax residency determines whether you are treated as a US taxpayer for income tax purposes, while domicile determines how your estate is taxed.

As a result, many Indians living and working in the US become US taxpayers for income tax purposes but continue to be treated as non-US domiciled for estate tax purposes.

If you are not US domiciled, you qualify for only the US$60,000 estate tax exemption on US-situs assets. This is significantly lower than the exemption available to US-domiciled individuals, which is $15 million.

If you hold more than US$60,000 of US-situs assets, such as US-listed shares or US-domiciled ETFs, the value above this exemption is subject to US estate tax, with the highest marginal rate reaching 40%.

Example

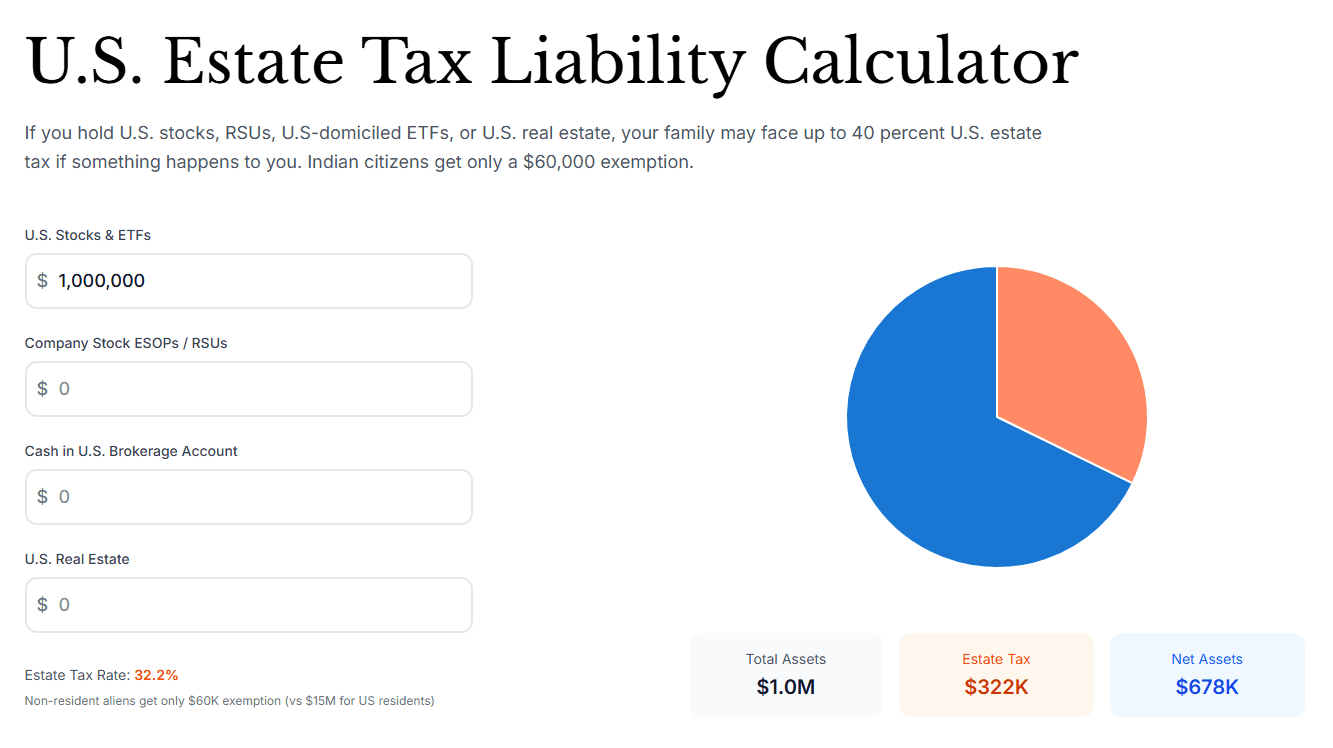

Suppose your total US assets, including stock market investments and other US-situs property, amount to US$1,000,000.

Here's what your estate tax calculation would look like:

Gross US Estate: US$1,000,000

Less Exemption: (US$60,000)

Taxable Estate: US$940,000

The estate tax is calculated progressively on the US$940,000 taxable estate, resulting in an estimated $322,000 of US estate tax.

In this scenario, out of your US$1 million portfolio, the IRS would collect $322,000, leaving around US$678,000 to your beneficiaries.

Use our US Estate Tax Calculator to estimate the potential estate tax on your own US-situs assets.

For investors who are not US taxpayers, one common way to avoid this exposure is to invest through UCITS ETFs. Since UCITS ETFs are not treated as US-situs assets, they fall outside the scope of US estate tax.

You can learn more about how they work in our UCITS ETF guide.

However, that solution is not available if you are a US taxpayer. Most UCITS ETFs are classified as Passive Foreign Investment Companies (PFICs) under US tax law, making them subject to a separate set of tax and reporting rules.

The PFIC Implications of Investing in UCITS ETFs

For US taxpayers, most UCITS ETFs are classified as Passive Foreign Investment Companies (PFICs) and are subject to separate US tax rules.

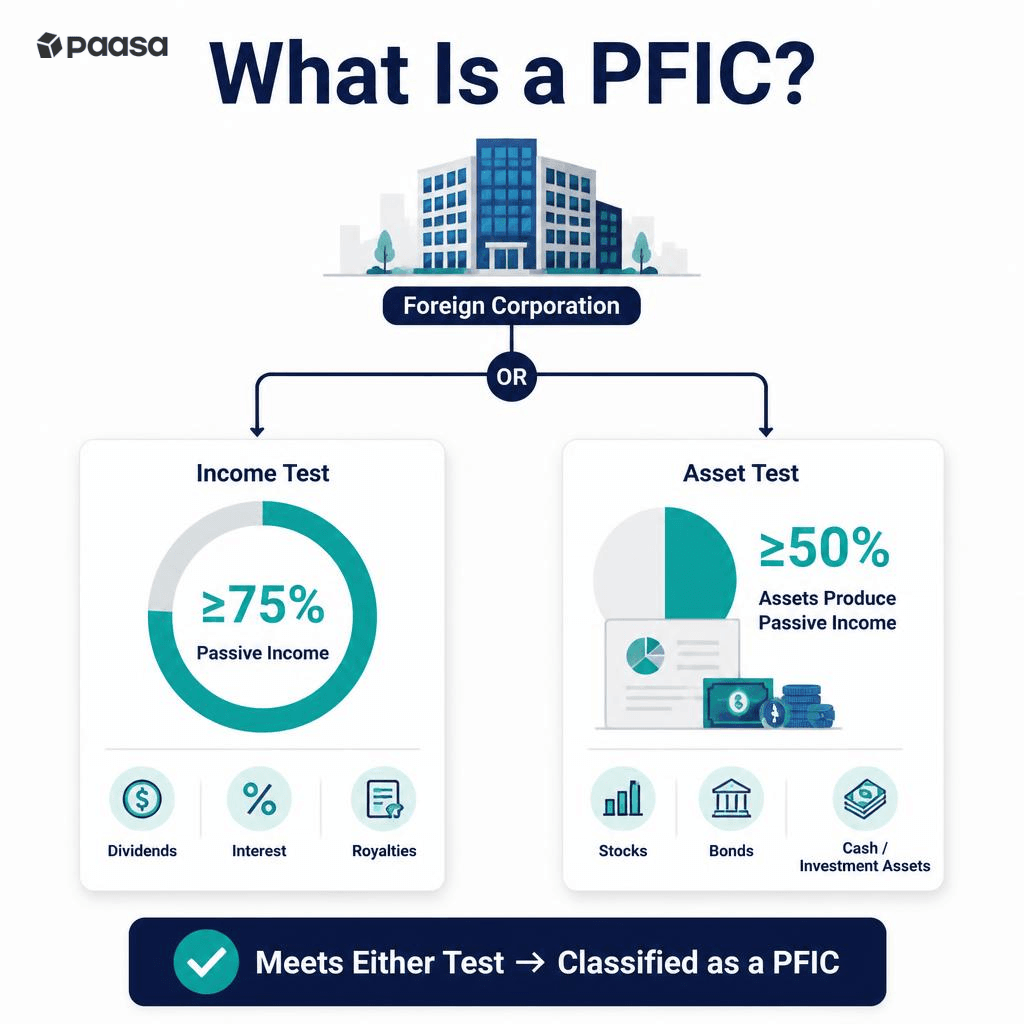

What Is a PFIC?

A foreign company is classified as a PFIC if it meets either of the following conditions:

- At least 75% of its gross income is passive income.

- At least 50% of its assets produce, or are held to produce, passive income.

Passive income includes dividends, interest, capital gains or royalties. For example, an Ireland-domiciled ETF that earns 98% of its income from dividends would satisfy the income test and be classified as a PFIC.

What Investments Can Be Classified as PFICs?

Many foreign pooled investment vehicles can be classified as PFICs. This includes many foreign mutual funds, investment trusts and exchange-traded funds (ETFs) that are established outside the United States.

Whether an investment is a PFIC depends on how the underlying entity is structured and whether it satisfies the PFIC tests under US tax law.

Are UCITS ETFs PFICs?

In most cases, yes.

UCITS ETFs are domiciled in jurisdictions such as Ireland or Luxembourg. Since they are foreign investment funds that primarily hold investment assets and earn passive income, they satisfy the PFIC tests.

As a result, a US taxpayer who invests in most UCITS ETFs is treated as owning a PFIC.

How PFICs Are Taxed in the US

PFICs are taxed under one of three U.S. tax regimes, depending on the elections available and made by the investor:

- Excess Distribution Regime (Default Rule)

- Qualified Electing Fund (QEF) Election

- Mark-to-Market (MTM) Election

1. Excess Distribution Regime

If you do not make a Qualified Electing Fund (QEF) election or a Mark-to-Market (MTM) election, your PFIC investment is automatically taxed under the IRC Section 1291 rules, commonly referred to as the Excess Distribution Regime.

This is the default PFIC tax regime and is considered the least favourable.

Under this regime, the IRS distinguishes between normal distributions and excess distributions.

A distribution is considered an excess distribution if it exceeds 125% of the average distributions you received from the PFIC during the previous three tax years (or your holding period, if shorter).

Example

Suppose you receive the following dividends from your UCITS ETF:

- Year 1: $100

- Year 2: $120

- Year 3: $140

The average distribution over the three years is $120. The IRS allows for an increase of up to 125% of this average, which is $150.

Now assume you receive a dividend of $230 in Year 4.

The first $150 is treated as a normal distribution. The remaining $80 is treated as an excess distribution.

The IRS assumes this $80 did not arise entirely in Year 4. Instead, it assumes the income accumulated evenly over the period you owned the PFIC.

If you have held the UCITS ETF for four years, the excess distribution is allocated as follows:

| Holding Period | Excess Distribution Allocated |

|---|---|

| Year 1 | $20 |

| Year 2 | $20 |

| Year 3 | $20 |

| Year 4 | $20 |

The $20 allocated to the current year is taxed under the normal tax rules.

The $20 allocated to each prior year is taxed at the highest ordinary income tax rate applicable for that year, regardless of your actual tax bracket.

In addition, the IRS charges interest because it treats those taxes as having been paid late.

The same principle applies when you sell your PFIC investment and realize a capital gain.

2.Qualified Electing Fund (QEF) Election

A Qualified Electing Fund (QEF) election is an alternative to the default Excess Distribution Regime. Many investors choose this method to avoid the punitive tax and interest rules that apply under the default PFIC regime.

Instead of waiting until you receive a large distribution or sell your PFIC investment, a QEF election requires you to report your share of the PFIC's income every year, even if the fund does not distribute any cash.

This means you pay US tax annually on your share of the fund's ordinary earnings and net capital gains as they are earned, rather than when they are distributed.

Example

Suppose you own an accumulating UCITS ETF, which reinvests all of its income instead of paying dividends.

During the year, your share of the fund's earnings is US$1,000.

Even though you do not receive any cash, you must report the US$1,000 as income on your US tax return and complete IRS Form 8621 to report your PFIC investment and QEF election.

Since you have already paid tax on these earnings annually, they are not taxed again when you eventually sell the investment.

This avoids the excess distribution calculations, the highest ordinary income tax rates, and the interest charges that apply under the default PFIC regime.

3.PFIC Annual Information Statement

You can make a QEF election only if the PFIC provides a PFIC Annual Information Statement.

This statement tells you how much of the fund's annual ordinary earnings and net capital gain is allocated to your investment for the year. You use these figures to calculate the income that must be reported on your US tax return.

Without a PFIC Annual Information Statement, you cannot make a valid QEF election.

Is a QEF Election Available for UCITS ETFs?

In practice, this is one of the biggest limitations of the QEF regime.

Most UCITS ETFs do not provide a PFIC Annual Information Statement. As a result, although the QEF election is often the most tax-efficient PFIC regime, it is not available for most UCITS ETF investors.

Mark-to-Market (MTM) Election

A Mark-to-Market (MTM) election is another alternative to the default Excess Distribution Regime.

Under this method, the IRS treats your PFIC as if you sold it at its fair market value (FMV) on the last day of each tax year and immediately bought it back at the same price.

This means you recognize gains or losses every year, even if you never actually sell the investment. Annual gains and losses are reported on IRS Form 8621.

If the value of your PFIC increases during the year, you must report the gain on your US tax return. If the value falls, you may be able to claim a loss, subject to certain limitations.

How Are Gains and Losses Taxed?

Under the MTM election, annual gains are taxed as ordinary income, not as capital gains.

Similarly, annual losses are treated as ordinary losses. However, you can deduct these losses only to the extent of the MTM gains that you have previously recognized.

For example, suppose you reported MTM gains of US$20 in each of the first three years, for a total of US$60.

In Year 4, the value of your PFIC falls by US$100.

Although your economic loss is US$100, you can deduct only US$60, because that is the total amount of MTM gains you previously recognized and paid tax on. The remaining US$40 cannot be deducted.

Who Can Make an MTM Election?

Not every PFIC qualifies for the MTM election.

You can make an MTM election only if the PFIC shares qualify as marketable stock under the IRS rules. This means the shares are regularly traded on a qualified stock exchange or another qualifying market.

Private foreign investment funds and many closely held foreign companies do not qualify.

Practical Approach for NRIs

If you are a US tax resident living in the US on a temporary work visa, the most practical approach is to avoid PFIC investments, such as UCITS ETFs, foreign mutual funds etc as the PFIC tax rules can significantly reduce your after-tax returns.

Instead, investing directly in US-listed stocks and US-domiciled ETFs is the more tax-efficient option, even though these investments remain subject to US estate tax.

For non-US domiciled individuals, the US$60,000 estate tax exemption is an unavoidable limitation.

However, if you become permanently domiciled in the US, the estate tax concern is largely eliminated because you become eligible for the much higher estate tax exemption of $15 million dollars.

If you later return to India, your tax position changes entirely, and your investment strategy should be reassessed accordingly.

About Paasa

Paasa is an Indian investor's gateway to global investing, trusted by HNIs, family offices, and institutions to diversify into markets across the US, Europe, China, Japan, and beyond.

What sets Paasa apart is its India-facing compliance layer:

- FEMA and LRS compliance embedded into every transaction.

- Tax reporting and analytics built for Indian investors (LTCG, STCG, dividend tax, TCS tracking).

- End-to-end support for remittance structuring, reconciliation, and compliance queries.

Whether it's equities, ETFs, UCITS funds, managed strategies, or even helping you protect your RSUs from estate tax, Paasa provides a single transparent platform for global portfolios with the confidence that India-specific compliance is taken care of.