The dollar's dominance looks unassailable on paper. It accounts for 56% of global foreign exchange reserves, 48% of SWIFT payments, and serves as the invoicing currency for nearly half of international trade.

Yet beneath this stability, a gradual shift is underway. BRICS nations (Brazil, Russia, India, China, South Africa, and their recent additions) are building payment systems, settling bilateral trade in local currencies, and establishing alternative financial infrastructure.

This is not the revolutionary overthrow of dollar hegemony that headlines suggest. It is financial hedging at scale.

Countries are reducing vulnerability to U.S. monetary policy, sanctions, and currency volatility.

The real question for investors is not whether the dollar will collapse, but whether these alternatives can move from bilateral experiments to systemic infrastructure.

Table of Contents

- The Dollar's Slow Erosion

- CIPS vs SWIFT

- BRICS Infrastructure:

- What This Means for Investors

- Limits of the Shift

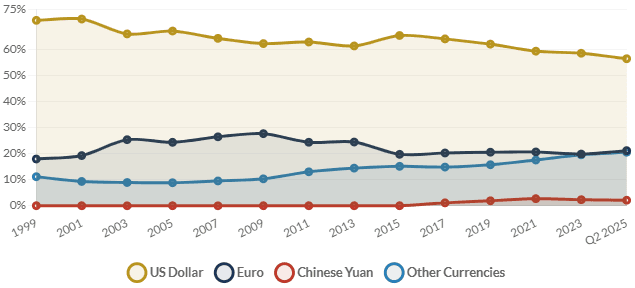

The Dollar's Slow Erosion

The dollar's share of global foreign exchange reserves has declined from 71% in 1999 to 56.3% in Q2 2025, a 15 percentage point drop over two decades.

This is not a crisis, but it is a trend. Central banks are diversifying into euros, yen, and smaller currencies like the Swiss franc, which quadrupled its reserve share to 0.8% in Q1 2025. Gold holdings have also surged, now comprising 23% of official reserve assets, up from under 10% in 2015.

The IMF's Currency Composition of Official Foreign Exchange Reserves data tells a nuanced story. When adjusted for exchange rate movements, the dollar's decline is less dramatic. Much of the Q2 2025 drop reflected euro appreciation rather than active selling.

But the structural trend persists.

Countries are moving away from concentration risk, particularly those exposed to U.S. sanctions or Fed tightening cycles. The weaponization of the dollar, including freezing Russian reserves after the Ukraine invasion and using SWIFT as a sanctions tool, accelerated this shift.

The question is not whether diversification will continue, but whether it will accelerate or plateau.

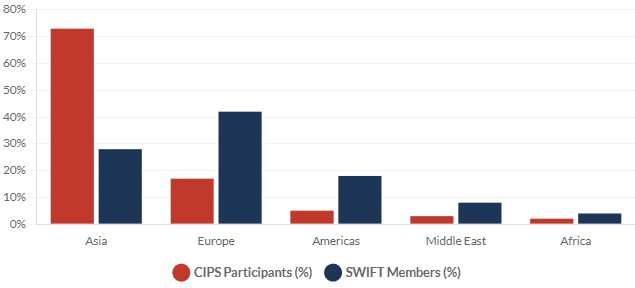

CIPS vs SWIFT: Scale Gap Persists

CIPS remains orders of magnitude smaller than SWIFT. While participant counts have grown (1,683 by May 2025), the system processed $24.5 trillion in 2024 compared to SWIFT's tens of trillions daily. CIPS transactions increased 24% to 8.2 million in 2024, but SWIFT handles over 40 million messages per day.

The infrastructure is building, but adoption lags. European institutions represent just 17% of CIPS indirect participants. Asia dominates at 73%. Until developed markets integrate CIPS into core operations, it remains a China-centric tool rather than a global alternative.

BRICS Infrastructure: Building in Parallel

The New Development Bank, launched in 2014, has approved $40 billion across 122 projects since inception. Under president Dilma Rousseff, the NDB raised $16.1 billion in 2024 alone, with local currency lending now at 25% of the portfolio (targeted to reach 30% by 2026).

Borrowing in renminbi or reais insulates recipients from dollar volatility and Fed rate cycles. BRICS Pay, the bloc's payment system, facilitates local currency settlements but remains limited in scope. The proposed BRICS Cross-Border Payment Initiative aims to create a multi-currency clearing infrastructure independent of SWIFT. The July 2025 Rio summit declaration made no mention of a common currency or coordinated de-dollarization strategy.

What This Means for Investors

De-dollarization is real, but it is gradual and regional rather than systemic. The dollar will not lose reserve status in the next decade, but its unchallenged dominance is eroding. Central banks are diversifying. Trade corridors are finding alternatives. Payment systems are proliferating.

For investors, the takeaway is diversification, not displacement. The dollar's dominance is eroding at the margins, creating opportunities in alternative payment systems, regional currencies, and infrastructure facilitating non-dollar trade. But the core of global finance (reserve holdings, capital markets, institutional trust) still anchors to the dollar. That will not change quickly, even as the world slowly builds parallel systems.

Limits of the Shift

History offers perspective. The British pound accounted for twice the dollar's reserve share in 1948. By 1969, the dollar had overtaken it tenfold. Currency dominance follows economic and geopolitical power. But transitions take decades and require alternatives with comparable depth, liquidity, and trust.

The euro was supposed to rival the dollar after its 1999 launch. It peaked at 28% of reserves in 2009 and has hovered around 20% since. Why? Fragmented bond markets, ECB policy inconsistencies, and recurring sovereign debt crises undermined confidence. The yuan faces steeper obstacles: capital controls, state intervention, and geopolitical tension.

BRICS de-dollarization is not theatre, but it is not revolution either. It is pragmatic hedging by countries seeking financial autonomy in a multipolar world. The infrastructure is real. The bilateral wins are tangible. But scaling from regional corridors to global systemic alternatives remains an open question, one more likely to unfold over decades than years.