For most of the last decade, Latin America was the part of an emerging market portfolio nobody wanted to talk about.

Brazilian equities traded at depressed multiples while domestic investors held the lowest allocation to local stocks in 25 years, Mexico's nearshoring story moved slower than promised, and Argentina was synonymous with currency crises rather than capital formation.

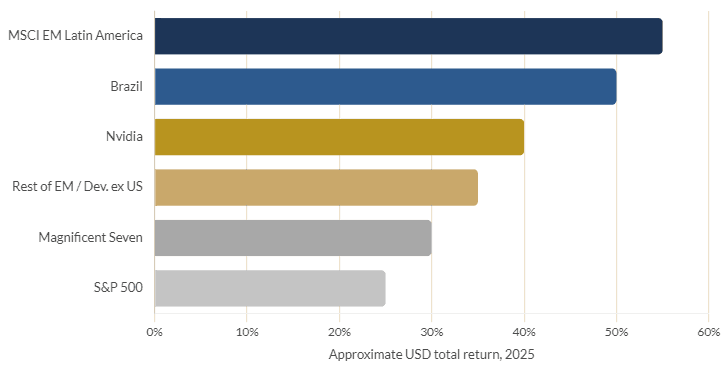

Then 2025 happened. The MSCI EM Latin America Index gained roughly 55% for the year, with Brazil, the region's largest and supposedly weakest performer, still up around 50%. That outcome was not just good relative to history.

It outpaced the broader emerging and developed ex US universe by roughly 20 percentage points, beat the Magnificent Seven cohort by about 25 points, topped the S&P 500 by close to 30 points, and even edged out Nvidia, the poster child of the AI trade, by around 15 points.

Table of contents

2025 Calendar Year Total Returns

The momentum has carried into 2026.

By late February, the MSCI EM Latin America Index had jumped over 20% year to date, reaching an eleven year high and marking its strongest start to a year since 1991.

The index capped a ninth consecutive week of gains in February, its longest winning streak since 2017, with Brazil, Colombia, and Mexico all drawing renewed overseas buying.

The catalysts were a mix of local and global: a US Supreme Court ruling that struck down a sweeping set of global tariffs gave risk assets a lift, while upcoming presidential elections in Brazil and Colombia raised hopes among investors for friendlier policy shifts and lower interest rates.

Whether this rally is the start of a structural rerating or a cyclical flash depends on two things: corporate earnings and policy follow through.

Consensus estimates currently call for around 15% earnings growth across the region in 2026, but that number assumes stable foreign exchange rates and commodity prices.

Given how many Latin American economies are commodity exporters, a sharp dollar rally or a slump in oil, copper, or soybean prices could quickly turn a tailwind into a headwind. The currencies to watch are the Brazilian real and the Chilean peso, both highly sensitive to global commodity cycles and a useful real time gauge of how the rest of

MSCI EM Latin America Index

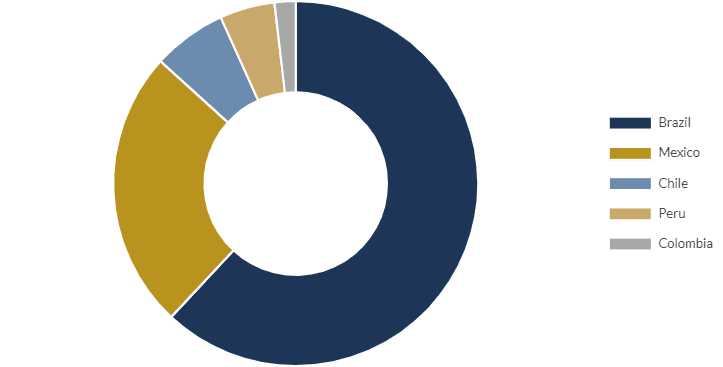

Brazil remains the anchor of the region, with the B3 exchange in São Paulo home to roughly a trillion dollars of market capitalisation and the Ibovespa hitting an all time high near 199,000 points in April 2026.

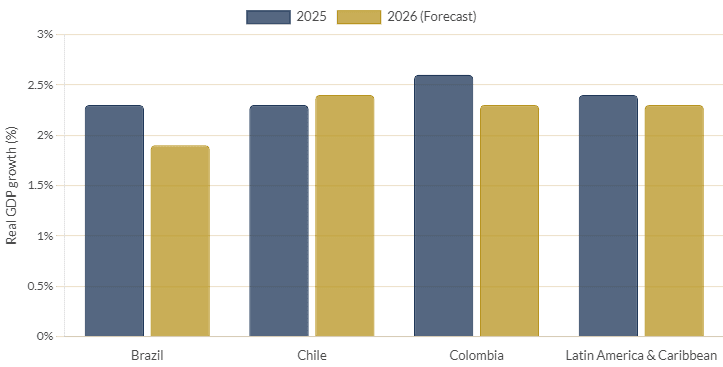

The country is benefiting from its position as a net energy exporter at a time of higher global energy prices, which the IMF cited as a key reason for upgrading Brazil's 2026 growth forecast.

The benchmark Selic rate sits at a punishing 15%, a legacy of past inflation fighting, with markets pricing in a gradual easing cycle that would lower the cost of capital for Brazilian businesses.

The flip side is a federal debt load near 92% of GDP on IMF methodology, a new 10% withholding tax on dividends paid abroad that took effect on January 1, 2026, and US tariffs of 50% on most Brazilian exports, with carve outs for aircraft, certain energy products, and select agricultural goods. Brazil has responded by deepening trade ties with China, a dynamic worth watching for anyone mapping global supply chain realignment.

Mexico is the conservative, nearshoring focused choice.

Bilateral trade with the United States exceeds 800 billion dollars annually, and the country's proximity, existing infrastructure, and competitive labour costs make it the most obvious beneficiary of companies shifting manufacturing away from China.

The July 2026 joint review of the USMCA trade agreement is the single most consequential policy event on the region's calendar this year. Mexico still holds an investment grade credit rating, though Moody's cut it to Baa3, the lowest investment grade rung, citing fiscal pressures and the heavy debt load at state oil company Pemex.

Notably, even with the nearshoring tailwind, Mexico's economy is projected to shrink in dollar terms in 2026, a reminder that peso strength and dollar denominated GDP do not always move in the same direction as equity sentiment.

Chile is the region's stable resource play.

The country supplies roughly a quarter of the world's copper and, together with Argentina and Bolivia, sits atop the so-called Lithium Triangle, which holds more than half of the world's known lithium reserves. Chile's IPSA index is smaller and less liquid than Brazil's or Mexico's markets, but inflation has returned to target and business investment tied to copper and lithium exports is expected to support growth of around 2.4% in 2026, according to the IMF.

Argentina is the region's highest conviction, highest volatility bet.

President Milei's reform agenda has cooled inflation and stabilised the peso, and the Merval index jumped roughly 10% in dollar terms in May 2026 to reach post election highs.

MSCI is weighing whether to restore Argentina to emerging market status, a move JPMorgan estimates could draw close to a billion dollars of near automatic index buying, though most analysts expect a watch list step in 2026 rather than a full upgrade. The country's RIGI incentive regime, which offers 30 years of tax and legal stability for investments above 200 million dollars, is already backing around 8 billion dollars of approved mining projects but is set to expire at the end of 2026.

On the commodities side, Argentina's lithium carbonate production reached approximately 34,100 tonnes in 2025, with major operators guiding to 35,000 to 40,000 tonnes in 2026.

Colombia offers some of the cheapest valuations and highest dividend yields in the region, but a 2026 presidential election introduces real political risk, and the central bank has been raising rates to tame inflation that remains well above target.

Peru, the smallest of the five MSCI constituent markets, is firmly in the copper camp alongside Chile, with growth expected to hold up even as political uncertainty continues to curb new investment.

The Sectoral Story: Minerals & Manufacturing

The energy transition has turned Latin America into one of the world's most strategically important regions for critical minerals.

Chile, Argentina, and Bolivia, the so-called Lithium Triangle, together hold more than half of the world's known lithium reserves, and Chile and Argentina already rank among the top global producers.

Argentina's 2026 production guidance of 35,000 to 40,000 tonnes of lithium carbonate, up from roughly 34,100 tonnes in 2025, illustrates how quickly this supply base is scaling.

On the copper side, Chile alone produces close to a quarter of the world's supply, and Chile together with Peru accounts for nearly 40% of global copper production.

The distinction matters for investors: copper has a structural demand floor tied to electric vehicles, grid infrastructure, and data centre buildout that legacy commodities like iron ore simply do not have, while lithium has become as much a geopolitical asset as an industrial input, with the US, the EU, and China all competing for secure access.

Mexico's nearshoring story is less a single sector than a basket of related ones.

Morgan Stanley identifies construction and cement as direct beneficiaries through industrial parks and logistics hubs along the northern border, alongside energy and utilities, where higher capital expenditure and deregulation are expanding power generation capacity to support new factories.

The scale of the underlying trade relationship, more than 800 billion dollars annually between Mexico and the United States, means even incremental gains in manufacturing relocation translate into meaningful demand for ports, transport corridors, and industrial real estate across the region, not just in Mexico itself.

Growth Outlook: A Region Growing Slower but Steadier

The takeaway is that Latin America's 2025 and 2026 equity rally has run well ahead of the underlying growth numbers.

That is not unusual for emerging markets coming off a low valuation base, but it does mean the sustainability of the rally depends more on multiple expansion, capital inflows, and policy credibility than on a surge in GDP growth itself.

The 15% consensus earnings growth estimate for 2026 is therefore the figure to track most closely, since it is the bridge between today's modest growth numbers and the much larger rerating that bulls like Morgan Stanley are pricing in toward the end of the decade.