In early 2020, as the pandemic paralysed the global economy, a strange thing happened. The Indian rupee didn't just weaken. It collapsed, falling from ₹71 to nearly ₹77 against the dollar in a matter of weeks, even as the US economy itself was entering freefall.

Two years later, in 2022, it happened again: the rupee hit then-record lows as aggressive Federal Reserve rate hikes sent the dollar index to a 20-year high, triggering the largest FII outflow from Indian equities on record over ₹1.21 lakh crore for the year.

For the Indian investor watching their portfolio bleed, this pattern feels arbitrary. The US was weak. Why was the dollar strong? Or the US was tightening, but India's own economy was growing. Why were foreign investors leaving?

The answer, with uncommon elegance, is the Dollar Smile Theory. A framework developed in 2001 by Stephen Jen, then a currency strategist at Morgan Stanley, that explains a fundamental asymmetry baked into the dollar's role in global finance.

Mastering this framework won't make anyone a forex trader. But it will make you a far better allocator.

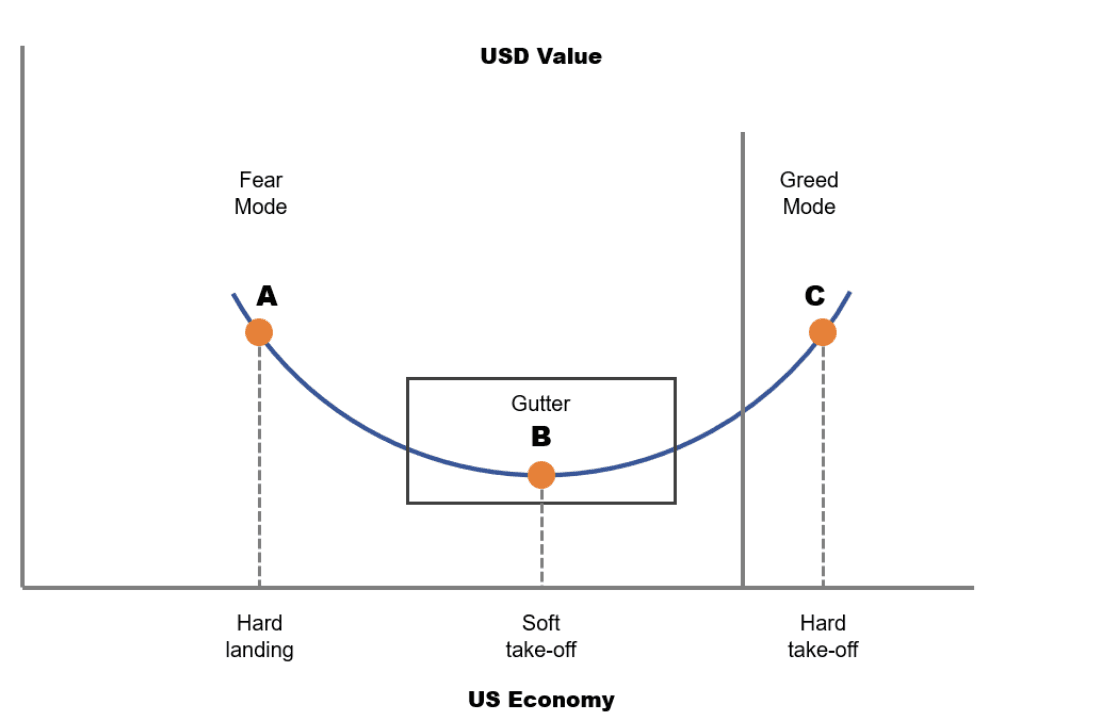

The Shape of the Theory

The Dollar Smile Theory rests on a deceptively simple observation: the US dollar tends to strengthen at both extremes of economic performance, and weaken in the middle. Plot dollar strength against the US business cycle, and you get something that looks like a smile.

Three distinct phases define it:

- Left side: The US or the global economy enters severe stress. Investors panic. Capital floods into dollar-denominated safe-haven assets: US Treasuries, cash. The dollar surges not because America is doing well, but because it is the world's lender of last resort. Fear is the engine.

- Bottom (trough): The crisis passes. The Fed cuts rates. The US economy muddles along; growing, but not impressively. Global growth is stable. With low US yields and improving conditions elsewhere, investors take risk. Capital flows outward toward higher-growth markets. The dollar weakens as money chases better returns.

- Right side: The US economy accelerates and clearly outpaces the rest of the world. The Fed tightens. Yield differentials favour US assets. Capital repatriates. The dollar climbs again, but this time driven by outperformance rather than fear.

What makes the framework powerful and counterintuitive is the left side.

A US recession, under traditional economic logic, should weaken the dollar. Fewer rate hikes ahead, lower yields, weaker fundamentals. But the dollar is not just an economic indicator. It is the world's reserve currency and its primary safe-haven asset. When fear overwhelms reason, the dollar rises regardless of US fundamentals.

India at the Crossroads of Each Phase

In the left phase — Global crisis, dollar surges.

India faces a dual blow. FIIs liquidate emerging market positions and repatriate to dollars, compressing Indian equity multiples. The rupee weakens sharply as dollar demand spikes. And because India imports roughly 85% of its crude oil in dollars, a surging dollar simultaneously raises import costs, widens the current account deficit, and fans domestic inflation. The 2008 GFC and the March 2020 COVID panic are textbook examples. Both triggered sharp rupee slides and FII exits that bore no relationship to India's own economic trajectory.

In the middle phase — Dollar weak, global risk appetite open.

India tends to be a primary beneficiary. Foreign capital flows freely into high-growth emerging markets. Indian equities see sustained inflows. The rupee stabilises or appreciates, reducing import costs and easing inflationary pressure. The 2004–2008 and 2020–2021 periods illustrate this well: dollar weakness, rising global growth, and a bull market in Indian equities moved largely in tandem.

In the right phase — US outperformance, Fed tightening.

India faces a structural headwind even if its own growth remains solid. Higher US yields make dollar assets more attractive on a risk-adjusted basis. The yield differential between US Treasuries and Indian government bonds, which has historically underpinned FII bond flows, compresses or inverts. FIIs don't need to be bearish on India to sell Indian assets. They just need to be bullish on America. 2022's record outflows are the clearest modern example: India's GDP was growing at a healthy 7%, yet FIIs withdrew at a historic pace.

The Rupee's Structural Asymmetry

The rupee is not a passive victim of the dollar cycle. Its relationship with the DXY (the dollar index against major developed-market currencies) is real but imperfect, a correlation of roughly −0.44 on monthly averages, according to analysis from Canara Bank. What this means in practice: a rising DXY reliably pressures the rupee, but the rupee can also weaken for India-specific reasons.

The structural backdrop matters. The rupee has depreciated from roughly ₹43 to the dollar in 2000 to around ₹84–86 today. That's a long-run weakening driven primarily by India's higher inflation rate relative to the US & the purchasing power parity (PPP) math playing out over decades. The dollar smile doesn't cause this secular depreciation. But it accelerates it at the worst possible moments.

What has changed is the Reserve Bank of India's growing capacity to intervene.

During the 2022 dollar spike, the RBI spent over $40 billion in forex reserves to defend the rupee by selling dollars in the spot market and taking positions in the futures market. This intervention doesn't reverse the trend; it smooths it.

Indian investors in 2025 face a rupee that is managed volatility, not free float, an important distinction when thinking about the actual impact of dollar cycles on real portfolio returns.

The Limits of the Smile

The Dollar Smile is a framework, not a formula. Several structural shifts since the Global Financial Crisis have complicated its predictive reliability. Central banks worldwide including China and Russia have meaningfully reduced their US Treasury holdings, gradually eroding the structural safe-haven bid. The dollar still accounts for roughly 58% of global reserves, but that's down from historical highs and trending lower.

The most significant complication in 2025 was that the dollar declined even during moments of global risk aversion as the left side of the smile appeared to be flattening.

Goldman Sachs described this as "uncharacteristic weakness during episodes of global risk aversion," suggesting that structural confidence in dollar hegemony is becoming less automatic.

For Indian investors, this is a nuanced shift: it means the dollar's safe-haven premium may offer less refuge during future crises than it did in 2008 or 2020.

Additionally, RBI intervention has created a managed float that decouples short-term USD/INR moves from the pure DXY relationship. India's growing domestic institutional investor base absorbed over ₹1 lakh crore of FII selling in October 2024 alone.

This means Indian markets are more insulated from foreign flow volatility than they were a decade ago. The smile still matters. Its edges are just harder to call precisely.

The Takeaway

The Dollar Smile Theory offers Indian investors something rare: a mental model that explains apparent contradictions.

Why does the dollar strengthen when America is in recession? Because fear is a dollar buyer. Why do Indian markets fall when India's growth is solid? Because the dollar is rising, and FIIs are leaving regardless. Why might the next multi-year bull market in Indian equities be partly a dollar story? Because a weakening dollar is, historically, the most reliable fuel for emerging market outperformance.

The dollar is the gravity of global finance. The smile describes how that gravity shifts across economic cycles. Indian investors who understand the phase they are in rather than reacting to each headline in isolation will allocate more deliberately, panic less, and position better for what tends to follow.