If you are an NRI, the fact that you are the citizen of one country and tax resident of another creates no problem when making investments, even in multiple countries.

But complex cross-border tax laws often create situations where simply holding certain assets or continuing your usual investments results in punitive taxes and heavy penalties since you are subject to regulations of multiple countries.

This also creates a new set of problems if you want to move back to India at any point.

We have covered the most common global investing oversights NRIs in countries like the US, UK, and Germany are making, and how you can avoid these mistakes, both while living abroad and while planning a move back to India.

Table of content

- Common investing mistakes NRIs make when living abroad

- Common mistakes NRIs make when returning to India

- How Paasa can help

Common global investing mistakes NRIs make when living abroad

1. Not accounting for the US Estate Tax

Most people assume that if they pass away, their US assets (stocks, ETFs, house) will simply pass to their spouse or children tax-free.

However, the US has an up to 40% Estate Tax that your heirs will need to pay before they can inherit your US assets.

The US Estate Tax is a federal tax imposed on the transfer of a deceased person's assets to their heirs, essentially acting as a tax on the right to transfer property upon death.

This is generally not a concern for US citizens and Green Card holders, because they get an estate tax exemption for assets up to $15 million, and the Estate Tax is only levied if the value of their estate exceeds this threshold.

However, for Non-Resident Aliens (NRIs), this exemption drops to just $60,000.

If you pass away while holding US assets (like US stocks, real estate, or a 401k) worth more than $60,000, the US government can tax the excess amount at up to 40% before your heirs receive anything.

Therefore, if you are a US tax resident NRI, you have to take the estate tax into account while financial planning.

Note: You cannot bypass the US estate tax while you are a US tax resident by buying non-US funds (like Indian Mutual Funds or Ireland-domiciled ETFs) to avoid holding US-situs assets. The US applies a punitive tax on "Passive Foreign Investment Companies" (PFIC). These holdings come with complex, strict reporting requirements and tax rates that can exceed 50%. This makes investing in non-US situs pooled assets like Indian Mutual Funds and UCITS ETFs extremely difficult while you are a US tax resident. Unlike funds, direct holdings of non-US situs stocks (individual companies) do not trigger PFIC rules. However, cross-border tax laws are complex; please consult a tax professional before proceeding with any restructuring. If you are not a US tax resident, buying non-US situs assets like UCITS ETFs is the best way to eliminate the US Estate Tax Risk while staying invested in US markets.

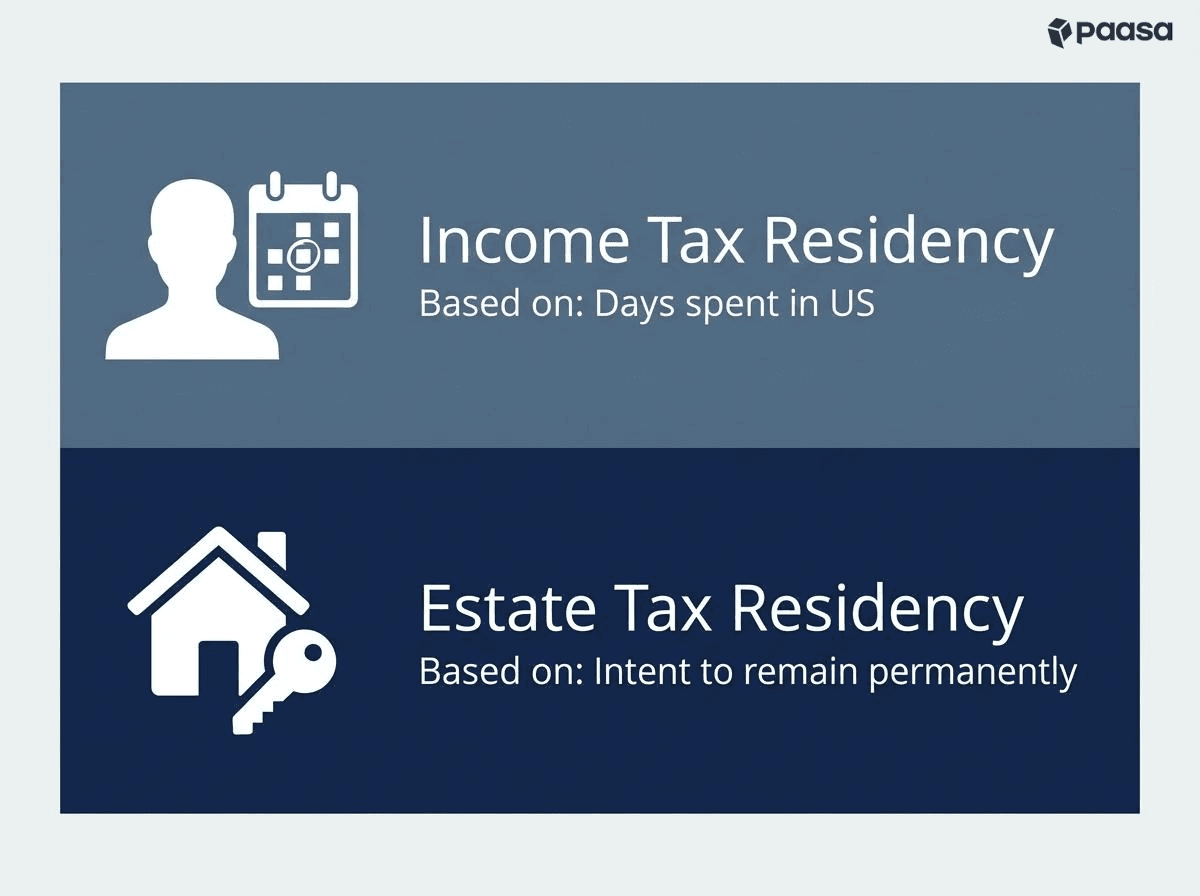

2. Assuming US tax residency equals residency for Estate Tax purposes

You might be a "Resident" for Income Tax purposes because you live in the US, but that does not automatically make you a "Resident" for Estate Tax purposes.

Estate Tax residency is based on "Domicile" and your intent to remain in the US indefinitely.

If you are on a work visa, it is assumed that you never intended to stay in the US permanently. This classifies you as a "Non-Resident" for Estate Tax, triggering the 40% tax liability on your total US assets above the $60,000 exemption.

3. Investing in Indian mutual funds while you are a US resident

Many NRIs continue investing in Indian mutual funds while living in the US, unaware that the IRS classifies these as Passive Foreign Investment Companies (PFIC). This triggers a punitive tax designed to discourage offshore investing.

Instead of paying the standard capital gains tax rate , your profits are taxed at the highest ordinary income rate (currently 37%), regardless of your actual tax bracket. On top of that, the IRS charges interest on these "deferred" taxes for every year you held the fund.

This interest is compounded daily, which can wipe out a significant portion of your total returns over time.

To avoid this, it is smarter to sell or gift your Indian mutual funds before moving to the US. You can then invest in India-focused ETFs listed on US exchanges (like INDA), which give you similar exposure but are taxed as regular US stocks.

4. Continuing with your regular Indian bank account

Continuing to use your regular resident savings account in India after moving abroad is a violation of the Foreign Exchange Management Act (FEMA).

Once you have been outside India for more than 182 days, your status changes to "Non-Resident," and you are legally prohibited from holding a standard savings account.

The penalties for this oversight can be severe, potentially reaching up to 300% of the funds involved.

To stay compliant, you must notify your bank to convert your existing account into an NRO (Non-Resident Ordinary) account to manage Indian income. You should also open an NRE (Non-Resident External) account, which allows you to repatriate foreign earnings tax-free.

Global investing mistakes NRIs make when returning to India

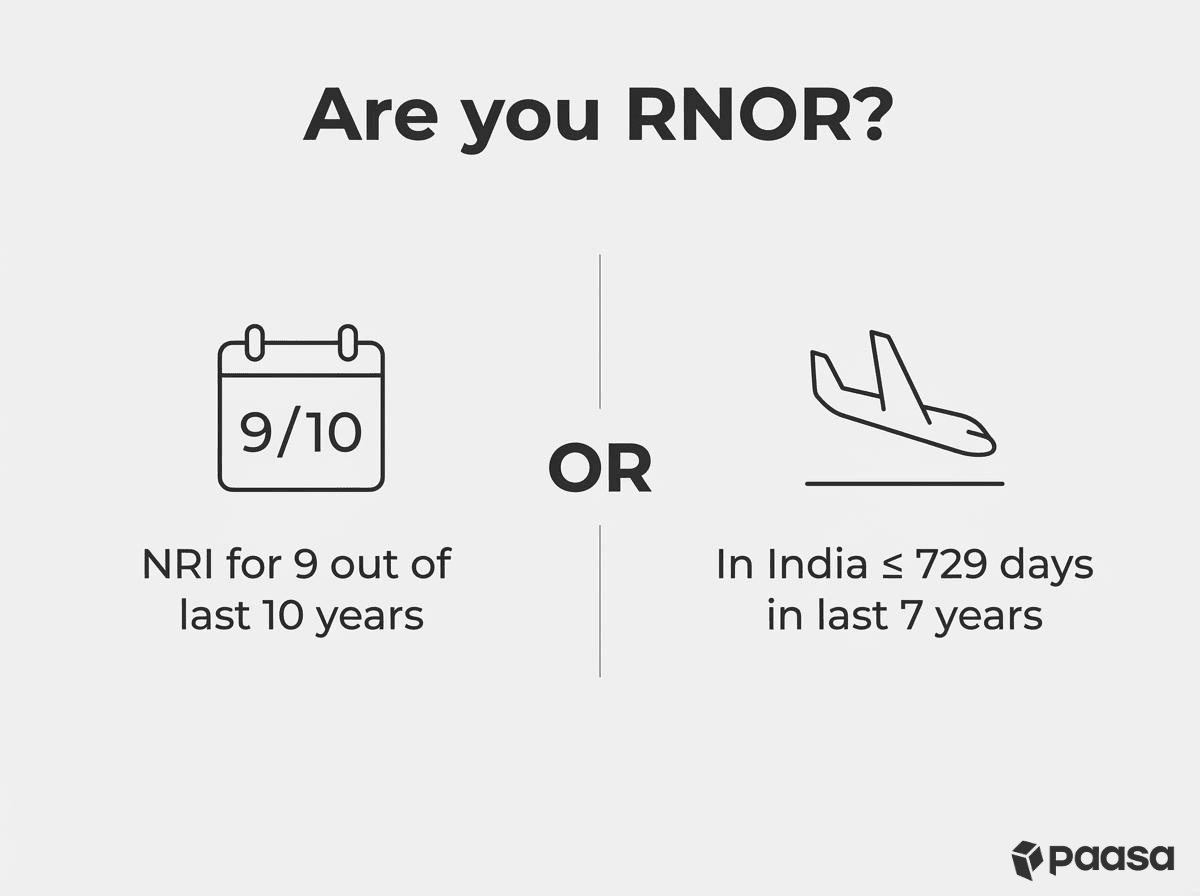

1. Not taking advantage of RNOR status while moving back

RNOR (Resident but Not Ordinarily Resident) is a transitional tax residency status for returning NRIs. It functions as a bridge between being a Non-Resident and becoming a full Ordinary Resident.

You typically qualify for this status if you meet one of the following criteria:

- You have been an NRI for 9 out of the last 10 financial years.

- You have lived in India for 729 days or less in the preceding 7 financial years.

- If you are an Indian Citizen or Person of Indian Origin (PIO) with Indian income exceeding ₹15 Lakhs, you become an RNOR if you stay in India for 120 to 181 days (instead of the usual 182).

- If you are an Indian Citizen with Indian income exceeding ₹15 Lakhs and you are not liable to tax in any other country, you are automatically treated as a "Deemed Resident" in India. Deemed Residents are always classified as RNORs.

This status grants you a 1 to 3-year window where your global income is treated differently from that of a standard Indian resident.

As long as you hold RNOR status, your foreign income is NOT taxable in India, provided it is received outside India first. This allows you to manage your US assets without immediate tax liability in India.

The mistake most people make is simply holding their US stocks through this period.

The smarter move is to "reset" your cost basis. While you are RNOR, you can sell that stock and immediately buy it back.

Because you are RNOR, the capital gain on the sale is not taxed in India. It is also usually not taxed in the country where you hold the stock since you have moved back to India and are now considered a non-resident. For example, the US has a 0% capital gains tax for non-residents.

This effectively updates your purchase price to the current market value. When you eventually sell the stock later as a full resident, you will only be taxed on the gains made after this reset, saving you a significant amount in future taxes.

Example

Suppose you are a software professional who has lived and worked in the US for the past 12 years. You recently moved back to India.

Having stayed only 300 days in India during the last 7 years, you qualify as Resident but Not Ordinarily Resident (RNOR).

You hold US stocks worth $700,000, and the total acquisition cost was $350,000.

Scenario 1: You did not sell (Old Cost Basis)

You held your original positions and became a Resident.

7 years later, your portfolio has grown to $1,500,000.

Since you are now a full Resident, the entire gain from your original purchase price is taxable in India.

| Amount | Note | |

|---|---|---|

| Sale Value (A) | $1,500,000 | Future value of the portfolio. |

| Original Cost Basis (B) | $350,000 | The price you originally paid in the US. |

| Total Capital Gain (A-B) | $1,150,000 | Profit liable for tax in India. |

| LTCG Tax @ 12.5% | $143,750 | Base tax on the gain. |

| Surcharge @ 15% | $21,563 | Calculated on the base tax amount. |

| Health & Cess @ 4% | $6,612 | Calculated on (Tax + Surcharge). |

| Total Tax Payable | $171,925 | Effective Rate: 14.95% |

Scenario 2: You sold while RNOR (New Cost Basis)

You executed a "Tax Reset" by selling your holdings while you were an RNOR and immediately repurchasing UCITS ETFs and US stocks.

This resets your cost of acquisition to $750,000 from the original $350,000.

7 years later, when the portfolio reaches $1,500,000, your taxable gain starts from the higher "reset" price.

| Amount | Note | |

|---|---|---|

| Sale Value (A) | $1,500,000 | Future value of the portfolio. |

| New Cost Basis (B) | $700,000 | Reset value during your RNOR window. |

| Taxable Capital Gain (A-B) | $800,000 | Gain calculated only from the reset point. |

| LTCG Tax @ 12.5% | $100,000 | Base tax on the reduced gain. |

| Surcharge @ 15% | $15,000 | Calculated on the base tax amount. |

| Health & Cess @ 4% | $4,600 | Calculated on (Tax + Surcharge). |

| Total Tax Payable | $119,600 | Effective Rate: 14.95% |

The Result

By resetting your cost basis during the RNOR period, you pay $52,325 less in taxes when you eventually exit your positions.

2. Not accounting for US exit tax (Green Card Holders)

If you have held a Green Card for 8 of the last 15 years, you are classified as a "Long-Term Resident." If you decide to surrender your Green Card and move back to India, you could be subject to the US Expatriation Tax (Exit Tax).

This tax generally triggers if your net worth exceeds $2 million or if your average annual income tax liability over the last five years was very high. If you qualify, the IRS treats you as if you sold all your assets on the day before you left. You are then forced to pay tax on the unrealized gains (paper profits) of your entire global portfolio, even though you haven't actually sold anything.

To avoid this, you should carefully plan your exit before hitting the 8-year mark. Alternatively, you can explore strategies like gifting assets to a spouse to bring your personal net worth below the $2 million threshold before you surrender your status.

3. Ignoring Germany’s exit tax (Wegzugsbesteuerung)

For years, Germany’s "Exit Tax" primarily targeted business owners holding shares in private companies. However, effective January 1, 2025, the rules also apply to private investors with significant portfolio holdings.

According to the new rule, if you have been a tax resident in Germany for at least 7 of the last 12 years and you decide to move away (e.g., return to India), you could trigger an immediate tax bill on your unrealized gains.

The tax applies if:

- You hold at least 1% of a fund's shares (rare for retail investors), OR

- You have invested more than €500,000 (acquisition cost) in a single fund or ETF.

If you cross these thresholds, the German tax office treats your departure as a "deemed sale." They act as if you sold your entire portfolio on the day you left and demand tax on the "paper profits" immediately, even though you haven't actually received any cash.

How to Avoid It

- Watch the Clock: If you plan to move to another country, plan your exit before you hit the 7-year residency mark.

- Structure Smartly: The €500,000 threshold often applies per fund. Diversifying your investments across multiple different ETFs (rather than putting €1M into a single stock) may help you stay below the limit for each specific asset.

4. Believing UK ISAs remain tax-free after returning to India.

Many returning professionals assume that because their Individual Savings Account (ISA) is tax-free in the UK, it remains tax-free in India. This is a costly misconception. The tax-free status is a UK-specific benefit that vanishes once you become a resident in India.

Once your status changes to "Resident and Ordinarily Resident" (ROR), India treats your ISA like any other foreign investment account. Dividends and interest become fully taxable at your income tax slab rate, and you will be liable for capital gains tax when you eventually sell.

To avoid paying unnecessary taxes, you should act while you are still an RNOR. By selling your ISA holdings and immediately repurchasing them (resetting the cost basis) before you become a full resident, you ensure that the gains you made while living in the UK are never taxed in India.

About Paasa

Paasa is a global investing platform built specifically for Indian residents and NRIs.

Paasa helps you invest globally and provides the compliance support advice you need to navigate global tax laws.

Paasa’s investment advisory can help you identify global investing mistakes before you make them, and help you find solutions tailored to your future plans and investment goals.

Disclaimer

This article is intended solely for information and does not constitute investment, tax, or legal advice. Global investments carry risks, including currency risk, political risk, and market volatility. Please seek advice from qualified financial, tax, and legal professionals before acting.