NRIs who have returned from the US and now hold RNOR status in India are often confused about how capital gains and dividend income from their overseas investments are taxed during this transition period.

This guide breaks down exactly how your US capital gains and dividends are taxed during this transition period, the reporting requirements in India, and how to optimize your portfolio before your status expires.

Table of contents

- What is RNOR

- How capital gains are taxed

- How dividend income is taxed

- Reporting requirements

- Get the most out of RNOR status

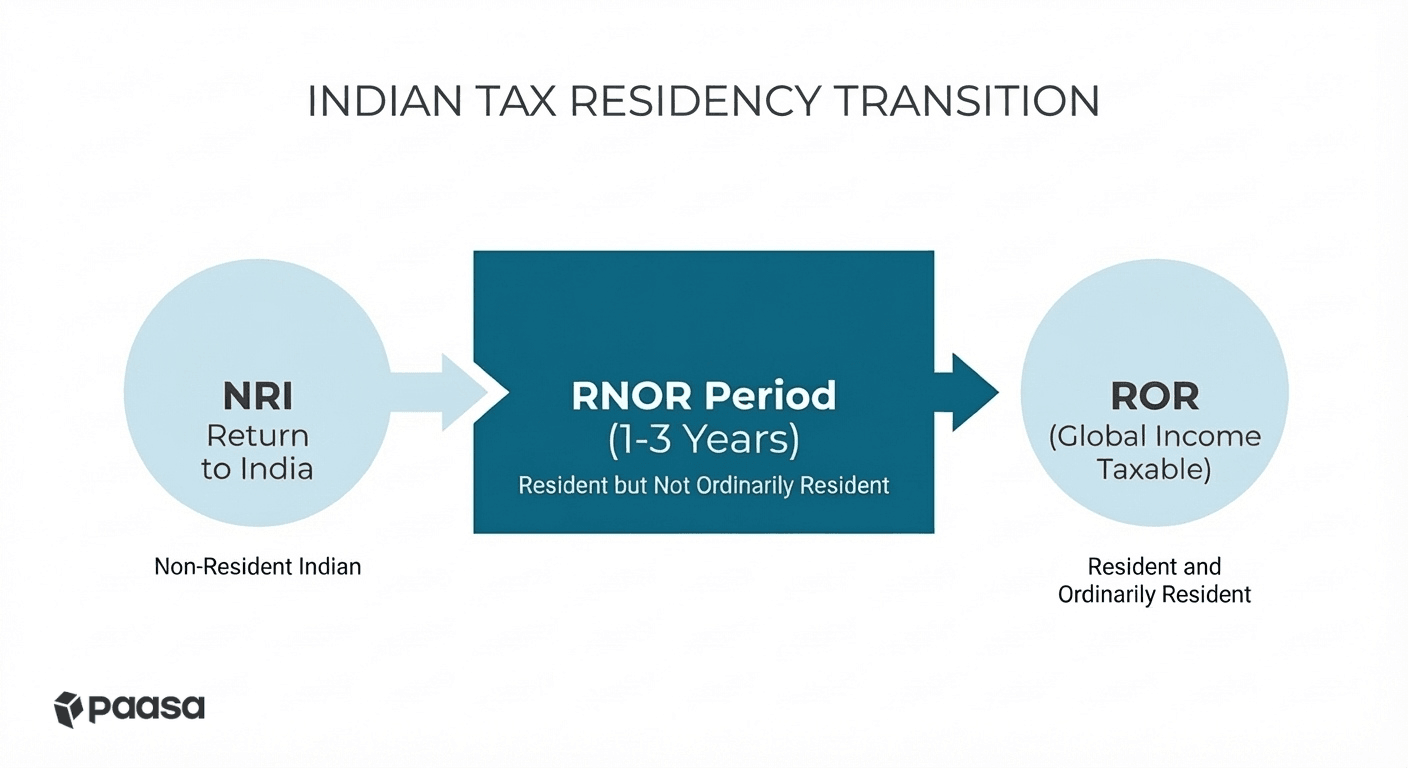

What is RNOR and who qualifies?

To qualify as an RNOR, you must first be considered a "Resident" of India for the current year (physically present for ≥182 days).

Once you are a Resident, you fall into the special RNOR category if you meet ANY ONE of the following criteria:

- You were a Non-Resident (NRI) in at least 9 out of the 10 financial years immediately preceding the current year.

- You were physically present in India for 729 days or less in total during the 7 financial years immediately preceding the current year.

- If you are an Indian Citizen or Person of Indian Origin (PIO) with Indian income exceeding ₹15 Lakhs, you become an RNOR if you stay in India for 120 to 181 days (instead of the usual 182).

- If you are an Indian Citizen with Indian income exceeding ₹15 Lakhs and you are not liable to tax in any other country, you are automatically treated as a "Deemed Resident" in India. Deemed Residents are always classified as RNORs.

How long does it last?

The RNOR status can last from 1 to 3 years.

Most returning NRIs enjoy this status for 2 full financial years after the year they return. In some cases (depending on your arrival date), it can stretch to 3 years.

Once this period ends, you become an Ordinary Resident (ROR), and your global income becomes fully taxable in India.

How are capital gains from US stocks and ETFs taxed when you hold the RNOR status?

Capital gains from US stocks and ETFs are tax-free when you are an RNOR in India.

1. In the US

As a non-resident of the US, you are not subject to US Capital Gains Tax on the sale of standard stocks or ETFs.

2. In India

Under RNOR rules, income that "accrues or arises outside India" is not taxable in India, provided it is not derived from a business controlled in India. Since your personal stock portfolio is a passive investment, the gains are tax-exempt.

Note

To keep this income tax-free, you must ensure the sale proceeds are deposited into your US brokerage account first.

When you sell your global investments using Paasa, the proceeds are deposited into your Paasa brokerage account, and remain tax-free in India.

Example

Suppose you are an RNOR in India and you sell US stocks and ETFs worth $100,000.

Your acquisition cost for these stocks was $60,000, meaning you have a capital gain of $40,000.

- Step 1: You sell the stocks.

- Step 2: The $100,000 proceeds are credited to your Paasa/IBKR wallet (which is an overseas brokerage account).

- Step 3: You then remit this money to your Indian bank account.

Because you are an RNOR and you received the funds in an overseas account first:

- Tax in the US: $0 (Non-residents pay no capital gains tax).

- Tax in India: $0 (Foreign income received abroad is exempt for RNORs).

You pay zero tax on your profit of $40,000.

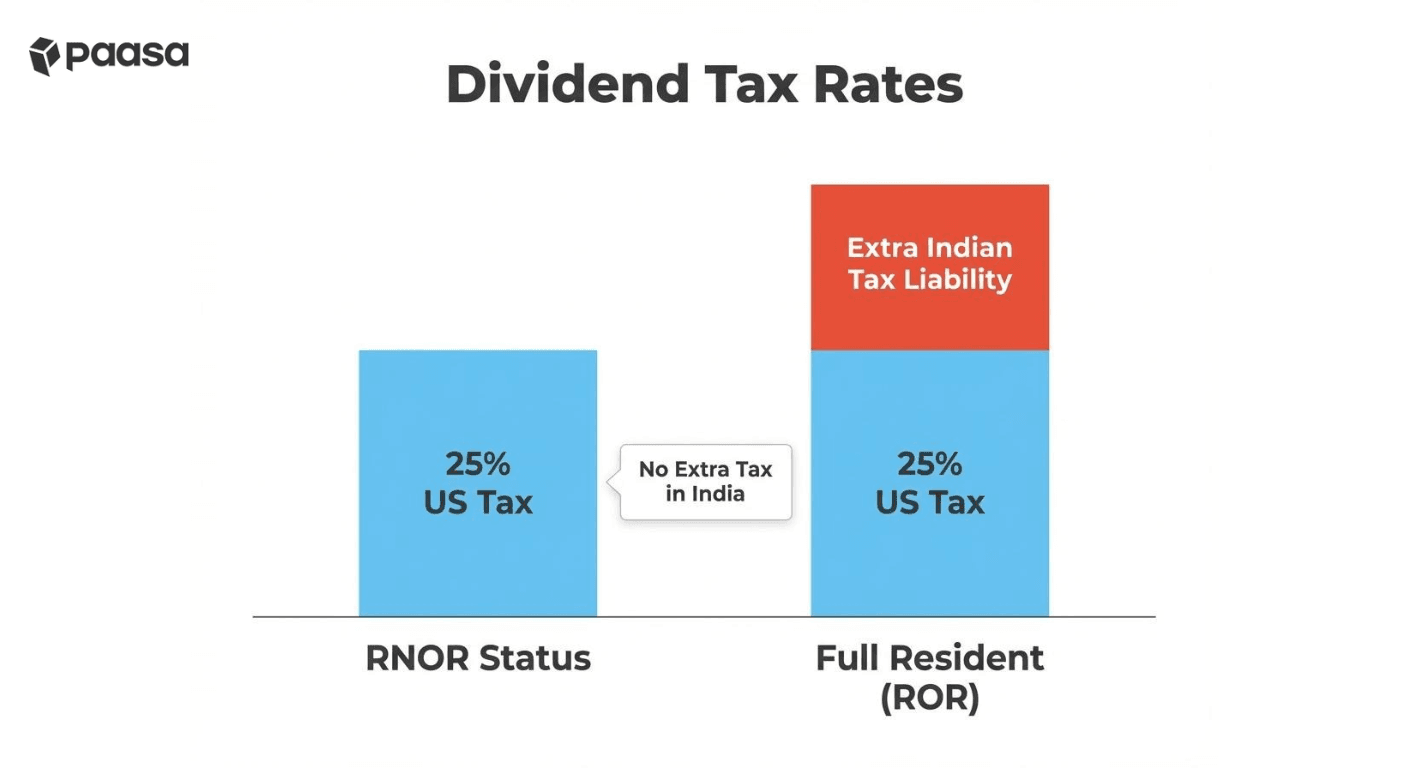

How is dividend income from US stocks and ETFs taxed when you hold the RNOR status?

When you receive dividends from US stocks, the US government deducts tax at the source before the money hits your account.

1. In the US (Withholding Tax)

For non-residents, the US applies a flat withholding tax on dividends.

Under the India-US Double Taxation Avoidance Agreement (DTAA), this rate is reduced to 25% (after filing Form W-8BEN).

Your US broker will automatically deduct this 25% tax and credit the remaining amount to your account.

2. In India (Tax-Free)

As an RNOR, this foreign dividend income is exempt from tax in India, provided it is credited to your overseas account first.

Because India does not tax this income, you cannot claim a Foreign Tax Credit (FTC) for the 25% tax you already paid to the US.

The tax paid in the US is effectively a cost you cannot recover.

Why this is actually an advantage

While losing 25% to taxes might seem high, it is usually better than being a full Ordinary Resident (ROR).

- As an RNOR: You pay a flat 25% (to the US) and 0% to India. Total tax = 25%.

- As a Full Resident (ROR): You would pay tax at your income slab rate in India. When you are in the 30% bracket (plus surcharge and cess), your effective rate will be higher than the US withholding tax. Even after claiming a credit for the US tax, you would still owe the difference to the Indian government.

Example

Suppose you received $10,000 in dividends from your US stocks this year. You fall into the highest tax bracket in India.

Here is how your tax liability compares as an RNOR vs. a full Ordinary Resident (ROR).

Scenario A: You are an RNOR

Since you are an RNOR, you only pay the US withholding tax. You do not owe any tax in India on this income.

| Amount | Note | |

|---|---|---|

| Gross Dividend Income (A) | $10,000 | Income received from US stocks. |

| US Tax Withheld (B) | $2,500 | 25% DTAA rate deducted at source. |

| Net Income Received (A-B) | $7,500 | Amount credited to your account. |

| Indian Tax Liability | $0 | Exempt foreign income for RNOR. |

| Total Tax Paid | $2,500 | Effective Rate: 25% |

Scenario B: You are a Full Resident (ROR)

If you were a full resident, this $10,000 is added to your total Indian income and taxed at your slab rate.

| Amount | Note | |

|---|---|---|

| Gross Dividend Income (A) | $10,000 | Added to your total taxable income. |

| Tax @ Slab Rate 30% (B) | $3,000 | Highest slab rate. |

| Surcharge @ 15% (C) | $450 | Capped at 15% for dividends. |

| Health & Cess @ 4% (D) | $138 | Calculated on (Tax + Surcharge). |

| Total Indian Tax Liability (E) | $3,588 | (B + C + D). Effective rate ~36%. |

| Foreign Tax Credit (F) | $2,500 | Credit for tax already paid in US. |

| Net Tax Payable to India (E-F) | $1,088 | Extra tax you owe to India. |

| Final Net Income (A-E) | $6,412 | Total Tax Paid: $3,588 |

By holding RNOR status, you save $1,088 in taxes and effectively pay the lower US rate (25%) instead of the higher Indian rate (~36%).

Do I need to report capital gains and dividend income from overseas investments while I hold the RNOR status in India?

You are not legally required to report your foreign assets and income in Schedule FA.

You generally do not need to fill Schedule FSI. You only need to fill it if you have any foreign income that is taxable in India while you are a RNOR.

How to get the most out of your RNOR status by resetting your cost basis

If you hold US stocks that have appreciated in value, you are sitting on unrealized gains. If you hold these stocks until you become a full resident, India will eventually tax you on the entire gain (from your original purchase price).

While you are still an RNOR, you can sell your US stocks and buy them back.

- Step 1: Sell your overseas stocks and ETFs Triggers a capital gain. Since you are an RNOR, this gain is tax-free in India (and tax-free in the US for non-residents).

- Step 2: Invest the money again in stocks and ETFs of your choice This establishes a new, higher "acquisition cost" for your investments, and also gives you an opportunity to restructure your portfolio if needed.

- When you eventually sell these stocks years later as a full resident, your tax will be calculated based on this new, higher price, effectively wiping out the tax liability on all your past growth.

Example

Suppose you bought Amazon stock years ago for $200,000. It is now worth $500,000. You expect it to grow to $1 Million in the future, at which point you will sell it as a full resident (ROR).

Here is the difference between holding vs. resetting your cost basis.

Scenario A: You Hold (Don't Sell)

You keep the stock. When you eventually sell at $1 Million, you are taxed on the entire profit from the very beginning.

| Amount | Note | |

|---|---|---|

| Future Sale Value (A) | $1,000,000 | Price when you sell as a resident. |

| Original Cost Basis (B) | $200,000 | The price you originally paid. |

| Taxable Capital Gain (A-B) | $800,000 | You are taxed on the full growth. |

| LTCG Tax @ 12.5% | $100,000 | Base tax on the gain. |

| Surcharge @ 15% | $15,000 | Calculated on the base tax amount. |

| Health & Cess @ 4% | $4,600 | Calculated on (Tax + Surcharge). |

| Total Tax Payable | $119,600 | Effective Rate: 14.95% |

Scenario B: You Reset (Sell & Buy Back Now)

You sell now at $500,000 (tax-free) and buy back immediately. Your new cost basis is $500,000.

| Amount | Note | |

|---|---|---|

| Future Sale Value (A) | $1,000,000 | Price when you sell as a resident. |

| New Cost Basis (B) | $500,000 | Reset Price (Higher cost basis). |

| Taxable Capital Gain (A-B) | $500,000 | You are taxed only on the new growth. |

| LTCG Tax @ 12.5% | $62,500 | Base tax on the gain. |

| Surcharge @ 15% | $9,375 | Calculated on the base tax amount. |

| Health & Cess @ 4% | $2,875 | Calculated on (Tax + Surcharge). |

| Total Tax Payable | $74,750 | Significantly Lower Tax Bill |

By selling and rebuying during your RNOR period, you will save $44,850 in future taxes ($119,600 - $74,750).

About Paasa

Paasa is a global investing platform built specifically for Indian residents and returning NRIs. We provide direct access to over 10 global exchanges, including the United States, United Kingdom, Switzerland, Hong Kong, Germany, France, Canada, Netherlands, Japan, and Singapore and support 9 global currencies.

- Seamless "In-Kind" Transfers (ACATS): You can move your entire US stock portfolio (from brokers like Robinhood, Schwab, Fidelity, E*TRADE, and more) directly to Paasa. This allows you to consolidate your assets in one place without triggering a tax event.

- The Compliance Advantage: Paasa provides the exact reports you need for your Indian tax returns and foreign asset disclosures, eliminating the need for manual calculations.

- Estate Tax Protection: Paasa offers access to Ireland-domiciled (UCITS) ETFs, allowing you to legally shield your long-term investments from the 40% US Estate Tax that applies to non-residents.